Tags

agricultural commodities, alternate energy, Austrian school, banking crisis, banks, bear market, bear stearns, bull market, capitalism, central banks, China, Comex, commodities, communism, Copper, deflation, depression, diamonds, dollar denominated, dollar denominated investments, economic, economic trends, economy, financial, futures, futures markets, gold, gold miners, hard assets, heating oil, India, inflation, investments, market crash, Markets, mining companies, natural gas, oil, palladium, physical gold, platinum, platinum miners, precious metals, price, price manipulation, prices, producers, production, protection, rare earth metals, recession, risk, run on banks, safety, silver, silver miners, socialism, sovereign, spot, spot price, stagflation, timber, U.S. Dollar, volatility, Water

Gold Bugs Beware – Seeking Alpha

I hope that all the gold bugs are preparing for the next leg down. Although risk does exist on both sides, the path of least resistance is down.

Then and Now

When researching gold prices, it is common practice to use historical quotes to give some indication of where prices may go. In my opinion that is a very bad strategy. ‘Inflation adjusted highs’ is simply a fancy way of saying that the price was here, we multiplied by some factor and so the inflation adjusted high is X. Therefore with more inflation the price MUST take out that previous high. That’s like saying that Yahoo shares traded for $100 in the past and since earnings have expanded since then, we must ultimately breach that price – ignoring the P/E ratio buyers are willing to pay and by that I mean demand.

You see, just how a lack of viable (good companies) alternatives led to Yahoo’s high price due to the price multiple, it was a similar case with gold in the 70s. A lack of alternatives and poor inter-connectivity in global markets made gold the only truly acceptable global inflation hedge and safe haven. Now things are different both fundamentally and structurally. One structural example is the increased use of derivatives and the use of treasuries to act as margin for these contracts. This has led to treasuries significantly outperforming gold as margin calls and safe haven buying have led to escalating purchases of treasuries.

Another problem with using a historical reference is that we have never experienced such a high level of de-leveraging – due to the excessively high credit buildup, that up until earlier this year fueled gold’s rise. Essentially the market is correcting the imbalances, exactly what the bugs were calling for, except it’s working against them. The size of the de-leveraging is dwarfing the capital that has been injected into the economy.

Gold ETFs

I read a great article on gold ETFs the other day and apologize to the author for not referencing it here as I cannot find it. Please post it as a comment if anyone knows what I am referring to.

The author was arguing that the landscape is very difference in the gold market because of the existence of the streetTracks Gold ETF (GLD) and the prices at which retail investors originally bought in at. The author argued that a lot of the purchases were made at prices above $600, and those investors may be tempted to sell if the price reaches their entry level. We may see a squeeze of sorts on the gold market, should that ETF be forced to liquidate sizable holdings at a fast pace to meet redemptions. Should that occur at the same time as the IMF or a central bank selling gold to meet short term expenses, there could be a structural crash in the price of gold.

The IMF and Central Banks

Institutions setup to pump liquidity into the system at crucial times can come under strain when their balance sheets are stretched and they are forced to raise capital. This is definitely not the largest risk to gold, but it does exist. The reason that the risk is minimal is that gold represents a relatively small percentage of the IMF and most countries’ reserves. Things would have to get really bad to force gold selling by these institutions.

New Demand

It’s hard to imagine a source of new demand entering the picture. While consumers globally are stretched, expensive jewellery is the last thing on your shopping list. With the majority of gold demand coming from jewellery, it’s unlikely that we seen a strong increase in net demand. You can make an even stronger argument by looking at some evidence of gold being pawned worldwide and demand for jewellery being even lower than published statistics.

Then there’s gold coin demand. This is retail investment demand and if history has taught us anything, it’s that betting against retail speculators is a good strategy. Many dealers are reporting shortages due to the higher demand for gold coins by retail purchasers. This has led many an unsophisticated investor to conclude that there is a shortage of gold and price must go up. As this group of investors continues to load up on coins, this contrarian speculator continues to get more bearish.

Supply

Gold miners just got huge production cost cuts. Mining is an energy intensive business, with tons upon tons of rock needed to find just a little gold. As their core costs come down, their margins increase relative to the market price. However, this is not a market in which to expect rising profit margins. This will enable the miners to decrease the price for the raw metal and try to make sales in a time of falling demand. Lower production costs may also stimulate supply in the short term as miners try to benefit from the lower energy prices and wider margins they are currently seeing.

What About Future Inflation?

What about it? I take two approaches here:

- The current trend is falling prices, a shortage in supply of credit globally, and weakening physical demand. You can try to catch a falling knife or claim that commodities aren’t in a bear market, but that is risky business.

- The reflationary trade will likely result in gold prices moving up at some point in the future, but outperforming equities? I don’t think so. At least not from the lows that we ultimately reach. But the government stimulus is inflationary! While that may be true, where is that stimulus going? Take Caterpillar (CAT) for example, who would have to increase in value by 150% to reach its previous highs. This isn’t a dotcom company with no real business behind it, this is the leader in global infrastructure. So when global fiscal stimulus picks up and that money finds its way to the market, credit is expanded, but the net benefit that a company like CAT realizes far exceeds the dilution effects of expanding the money supply. Also, companies own lots of real assets which will adjust up in value on top of the contracts they will receive which will expand their bottom line. Cost cutting is another avenue where good managers can increase value. It’s almost a nice excuse to clean house, then when things start moving again, they can be prudent and try to get technology to replace labor where possible.

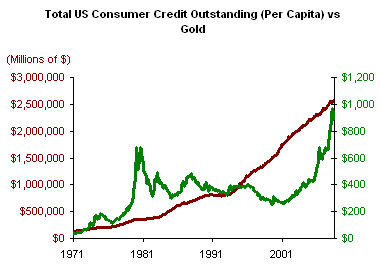

(Please note that the above chart is dated July.)

What the chart above shows is a graphical interpretation of my argument. Firstly, gold rose far more significantly than consumer credit in the 70s. To hit the inflation adjusted high, gold would have to outpace the growth in consumer credit by a large margin which I don’t think is happening. In fact, I see consumer credit having low or negative growth for the next 12-18 months as mortgage, credit card and auto loan terms get stricter. As you can see in the chart, this happened in the early 90s as consumer credit didn’t grow. Gold price remained relatively flat and then dropped significantly (in percentage terms), once credit started rising again. Why?

In recoveries, the expectation is decreasing risk and an eventual boom. In that environment, the opportunity cost of holding gold increases significantly and money rushes out of cash, gold, and treasuries and into equities. Although this causes a drop in gold price in the medium term, constantly rising credit will still result in a higher gold price as the cycle plays out, but from trough to peak, equities will outperform gold. It is during the second half of the credit boom that investors are advised to shift out of equities and increase gold holdings.

Gold’s Status as a Safe Haven

So has gold’s position as a safe haven been threatened? In a way, yes. It’s not that the fundamentals of gold aren’t attractive, but rather the existence of alternative safe havens. As far as the fundamentals go, gold’s biggest strength is also its biggest weakness. The limited supply of gold is often argued to be the reason for its great store of value, but that limited liquidity also makes it subject to volatile swings, usually into overvalued territory. As word of gold’s safe haven status has spread over the decades, worrying times bring a rush of people into gold, often more demand than the metal can handle. For that reason we see spikes that leave buyers at the peak feeling like they’ve been cheated.

Access to global markets changes the entire landscape, and the nature of a safehaven can change. Whether it’s unfairly beaten down equities, raw land in a politically stable country, or fiscally sound sovereign debt, the global markets present a wide variety of safehaven alternatives. In general, these investments require more sophistication to identify bargain prices and thus don’t have the same over crowding problem as gold.

As an example, Buffett’s 10% preferreds implicitly (in my opinion) backed by the government in the case of Goldman (GS) and with a solid company like GE, these investments may in fact be lower risk than gold and on an adjusted return basis should significantly outperform gold over the next 5 years, even though he may have acted too early.

Gold’s Performance

That being said, gold has outperformed since the peak and YTD – so it’s safe haven status isn’t totally destroyed – it just has competition. That being said, other investments like Japanese Yen have far outperformed gold.

Conclusion

The gold trade was over crowded and is likely going to continue to unwind as commodity prices have retreated signfiicantly and might continue to do so. Structural issues such as ETFs which have never experienced liquidation strain may become a big piece of the puzzle. Although gold will likely be at a higher price than today’s at some point in the future, speculators should brace for lower prices in the interim. Then, once prices turn around, investors should take careful note of trough equity valuation before dumping their funds into gold.

Disclosure: Trading with a bear bias

Related Articles

|

|

This article has 4 comments:

0

0

Nov 13 09:05 AM

0

0Nov 13 09:10 AM

0Nov 13 09:49 AM

I do take goldbugs into account (I’m not a fan of gold bugs). The truth is that being a gold bug is such a weak investment strategy that although they are fairly large in numbers (and very loud), they don’t collectively have enough capital to really affect the market. What happens with jewelery demand and industrial use is far more important. At present the amount of fund liquidation far exceeds the dollar cost averaging going on. Take a look at the gold COT’s.

Marp,

That kind of simplistic analysis is exactly why the gold space gets crowded and overvalued. All goldbugs do is preach value (with regards to inflation), yet don’t care what price they’re buying gold at. Take a look at this chart and tell me that there’s no basis risk in that strategy www.plusev.ca/gold-usd…/. Gold has strengthened far more than the dollar has weakened.

Moses,

I agree with that strategy.. I think that gold stocks will beat gold price out of the gate when the time comes. Energy costs come down 2/3rds and if gold only comes down 1/2 then theres lots of extra cushion on their margins