Are We Getting Ripped Off? Read Today’s Post dealing with the Bailout, Gold Price Manipulation and more. I’m back, we have a new President, what does this mean for your investments… Read On and Good Investing! – jschulmansr

Preventing The Greates Heist In History- Seeking Alpha

By: Whitney Tilson of Value Investing

There’s currently an idea to fix the financial system that’s getting quite a bit of traction: an RTC-type program whereby the government would buy $1 trillion of troubled assets from struggling U.S. banks, with the goal of restoring them to health so they can begin lending again, leading to an economic recovery.

The problem with this idea (let’s call it “New RTC”) is that either the government will pay market prices for the toxic assets – in which case, it will simply accelerate the collapse of our financial system – or pay above-market prices, in which case taxpayers will likely suffer big losses.

De-Leveraging Is Not Deflation-Seeking Alpha

By: Paco Ahigren of Ahigren Multiverse

“Inflation, as this term was always used everywhere and especially in this country, means increasing the quantity of money and bank notes in circulation and the quantity of bank deposits subject to check. But people today use the term `inflation’ to refer to the phenomenon that is an inevitable consequence of inflation, that is the tendency of all prices and wage rates to rise. The result of this deplorable confusion is that there is no term left to signify the cause of this rise in prices and wages.”

— Ludwig von Mises

It’s true that just about every asset class is coming down in price right now. This, however, is not deflation — as I have said so many times recently, much to many readers’ unqualified chagrin. To the contrary, these declines are the products of de-leveraging — not deflation — and the distinction is nearly incalculably important, although the subtlety seems to elude even the most astute these days.

If the previous premise is true (which it is), any removal of money from the economy would eventually result in an increase in the value of our currency, relative to everything else. And that, in turn, would eventually translate into lower prices in dollars. But that’s clearly not what is happening. No, the Fed is printing money, sending the amount in the economy higher than ever seen in U.S. history. That’s not deflationary. That’s inflationary.

Just so you’ll know, here’s the definition of inflation I’m using. And before you pooh-pooh it with too much eagerness, remember that one of its authors, F.A. Hayek, won the Nobel Prize in economics in 1974.

Look, the thing we should be worried about is relative value, not “inflation,” per se. It’s not about the growth of M0, or M1, or M2 (or even M3, if you keep up with shadowstats.com), so much as it is about what the money supply is doing relative to everything else that is happening. I know assets are falling in price — believe me, I get no shortage of reminders every single day. But the amount of money in the system — not just M0 — is increasing at a tremendous rate. I won’t argue that the relative value of things like real estate and equities are going to continue to drop — maybe even dramatically, and for a long time — in terms of demand (or lack thereof). No, what I’m most concerned about is that demand will stay extremely low, and yet prices will rise anyway because of the increase in the amount of money in the system.

But it’s not just money; it’s also Treasuries. The Fed has specifically stated that its objective is to stimulate “inflation” (by its definition). It wants prices to rise, and it’s going to do everything it can to find success. But the amount of money in the system is unprecedented. When the Treasury bubble starts to collapse, yields are going to explode. Yes, the Fed will probably print more money to buy down the long-end of the curve, but how long will that work? Some people say years, but how? Do you really think the Chinese and the Japanese are going to keep funding that sort of behavior? Or even more importantly, do you think they’re just going to sit on their current holdings? Probably not, and if they start dumping Treasuries, yields are going much higher.

It’s not a matter of if this is going to happen. Yields can’t stay where they are for any sustained amount of time, and once they start rising, so will prices. But will demand for, say, houses have increased? No. Cars? No. Boats? Televisions? No. Why? The American consumer is tapped out.

Credit card companies are tightening limits prodigiously. Teaser rates are all but gone. Home equity has dried up. The consumer has driven two-thirds of our economy for at least the last few decades, and now the consumer is dead. There’s another aspect to this that I won’t go too deep into: the American consumer protects his or her credit score for one reason — to obtain future credit. But the consumer also knows that loans have dried up — not just today, but for the very distant future as well. You know these consumers have to be thinking about defaulting; if they can’t get loans anyway, why would they not default on thousands of dollars in unsecured credit card debt? I plan on writing more about this in future articles, but suffice it to say, I think credit card companies are going to give us the next blow to our collective stomach, and it’s going to hurt.

So here we have a situation in which demand is gone, and yet prices and rates are rising — because of inflation (printing money) and the Treasury collapse. And that’s the point: it’s not going to come from just one source. It’s not just going to be inflation (printing money). It’s not just going to be the collapse in Treasuries. It’s not just going to be the nearly unfathomable costs of the stimulus packages that are coming online in the next two years. It’s going to be the confluence of all of it. And if I’m right about the continued deterioration in credit markets, things will be even worse.

You think it’s not different this time? Add it all up, in real dollars — the staggering amount of debt, the parabolic rise of currency in the system, the annihilation of real-estate investment, and the demise of the consumer. $8.5 trillion committed to bailouts and stimulus packages. Oh, yes it is different this time. It’s very different.

Credit cards didn’t even exist in 1930, and the dollar was backed by gold. Credit cards barely existed in 1973. Nixon had just taken us off the gold standard, and look what happened? Volcker was immensely lucky to have stopped hyperinflation, and look at the extreme measures he had to employ to do it.

Of course, every time I bring all of this up — which is a lot lately — somebody starts talking about the velocity of money. And pretty soon after that, somebody starts talking about the multiplier effect.

Yes, the U.S. employs a fractional reserve system, and while that system certainly lends to rising prices and yields, the amplifier effect is not inflation. Like the printing of money, the fractional reserve system is only one ingredient in the poison that lends to the ultimate catastrophe inspired by central banks: rising prices and increased costs of borrowing.

And then there’s velocity…

While I am eternally grateful to my critics for forcing me to defend the theories I hold dear, I sometimes fatigue of the incessant snapping at my heels by people who want me to know that the velocity of money has slowed down. I know the velocity of money has slowed. It doesn’t matter. It’s not going to stay this low for long, and when it starts speeding up, it’s not going to be a “good thing.” Treasuries are going to break, rates and prices are going to rise, and all that money pressing against the dam is going to find a crack. Why? It has to. People will flee from dollars that are losing value. They will extract all the dollars sloshing around the system, and they will buy commodities and durables in order to preserve the value of their wealth.

Remember, just because the dollar is losing value does not mean that the concomitant subsequent rise in certain asset classes necessarily means that demand for all assets has increased dramatically — as it did during previous eras of easy money. Demand for assets economy-wide can continue to wane even as people spend dollars as fast as they can get them in the midst of rising prices. And this is a very important distinction: prices can rise because of demand, but prices can also rise because of excessive increases in the amount of money in the system. If prices are rising without a simultaneous increase in demand, well, I can’t think of a more dangerous economic environment to be in.

You don’t believe it can happen? You think there’s a huge demand for houses, cars, and boats in Zimbabwe? Prices there are rising exponentially, but there is very little demand for assets — other than staples, of course. What do you think their velocity of money is?

The other day I wrote that Treasuries and the dollar are not “safer” than gold, and for my efforts I was heckled by several readers. Ultimately, however, flight-to-quality will seek the true risk-free rate of return, and this is yet another factor that will contribute to the imminent ferocity of the move that’s coming. Once Treasuries unwind, people and institutions will scramble to find a place to put the money they had once placed in the “safety” of U.S. government debt. And unless you know of a medium whose historical consistency and safety surpasses gold’s, that will be the place investors find haven.

Just for future reference: when I say the dollar’s going to fail (which it is), and you’re hovering over your keyboard, poised like some bird-of-prey, ready to strike me with all the ire of God-upon-Sodom, will you try to remember that I acknowledge velocity is, at least for the time-being, near zero. Will you also try to remember that I don’t believe the massive increase in currency alone will not be responsible for imminent rising rates and prices? In fact, I think Treasuries are going to play a greater role in the beginning.

Also, I agree with many of you that my timing may be a bit premature, and I exited my TBT after the last run-up. Unfortunately, today the stock market and Treasuries are getting crushed as gold rallies. I wouldn’t want to declare myself “right” based just on the behavior of these markets in recent days. That would be stupid. And yet I sit here and watch TBT move higher, wondering if getting out was even more stupid.

To add to my trepidation, some sort of manager in the South Korean finance ministry came out over the weekend and announced that the time has come to sell U.S. Treasuries. How do you think that made my stomach feel? Of course, Bernanke keeps promising to do battle with the long end of the curve, so maybe he’ll make good on his threat and I can find a point to get back in comfortably.

Of course, if I miss the move because I listened to some of you cynics. Well, at least I still own gold.

Disclosures: Paco is no longer short U.S. Treasuries (although he hopes to be again soon). He is long physical gold, and the Proshares Ultra long gold ETF (ticker: UGL).

Copyright 2009, Paco Ahlgren. All Rights Reserved.

================================================

On Gold Price and Market Manipulation

Questions Begging Answers- GoldSeek.Com

By: Rob Kirby of Kirby Analytics

To say that markets have been behaving “strangely” recently is an understatement. In recent weeks and months we’ve been witness to historic lows in sovereign interest rates in-the-face-of record amounts of debt being issued by governments? We’ve seen the price of gold behave counter intuitively by “not rising” in-the-face-of unprecedented systemic global economic malaise? Last, but not least, we’ve witnessed a “complete flip-flop” in the traditional pricing of Brent Crude Oil [IPE-London] versus West Texas Intermediate [NYMEX-N.Y.]?

So we have the price of gold, the price of crude oil and interest rates – three items vital to the integrity of the U.S. Dollar – ALL trading in total disregard for their underlying fundamentals?

The following is a thought provoking analysis with commentary:

The Situation In Gold

First and foremost it is imperative that everyone realize and understand that Gold “is” Money. We know that gold is money because every Central Bank in the world carries gold on their balance sheets as ‘an official reserve asset’.

With that in mind, folks would do well to read one of James Turk’s latest articles titled, The Fed’s blueprint for market intervention . In this article, Turk offers commentary on a recently unearthed 1961 document from the archives of the late, long-time former Chairman of the Federal Reserve, William McChesney Martin Jr. which details in the Fed’s own pen; their plans to intervene surreptitiously in the currency and gold markets to support the dollar and to conceal, obscure, and falsify U.S. government records so that the intervention would not be discovered. In Turk’s words,

“In short, [the newly unearthed document] lays out what the Treasury and Federal Reserve needed to do in order to begin intervening in the foreign exchange markets, but there is even more. This document plainly shows what happens when government operates behind closed doors. It also makes clear the motivations of the operators of dollar policy long described by the Gold Anti-Trust Action Committee and its supporters — namely, that the government would pursue intervention rather than a policy of free markets unfettered by government activity. The run to redeem dollars for gold had put the government at a crossroads, forcing it to make a decision about the future course of dollar policy. This paper describes what the government would need to do by choosing the interventionist alternative.

This document provides primary, original source supporting evidence that GATA has been right all along.”

In Feb. 2007 here’s what the Royal Bank of Canada’s Chairman, Tony Fell had to say, confirming unequivocally that gold is money,

“At Royal Bank of Canada, we trade gold bullion off our foreign exchange desks rather than our commodity desks,” says Anthony S. Fell, chairman of RBC Capital Markets, “because that’s what it is – a global currency, the only one that is freely tradable and unencumbered by vast quantities of sovereign debt and prior obligations.

“It is also the one investment and long-term store of value that cannot be adversely impacted by corrupt corporate management or incompetent politicians,” he adds – “each of which is in ample supply on a global basis.”

In short, says Fell, “don’t measure the Dollar against the Euro, or the Euro against the Yen, but measure all paper currencies against gold, because that’s the ultimate test.”

Fell’s admission coupled with the recently unearthed account of the Fed’s game plan shows that gold “is” and always has been feared as competition for the U.S. Dollar and a game plan has long been in place to thwart it. This explains why economic data has been falsified and the price of gold has been surrepticiously managed and interfered with by the United States Treasury and the Federal Reserve.

The mounting evidence is this regard is so compelling that from this point forward any ‘economist’ attempting to explain our current situation without prefacing their explanation with an EXPLICIT ACKNOWLEDGEMENT that our capital markets are not free and are in fact RIGGED by officialdom – their analysis is not worth the time to read it. In this regard, perhaps never have more prescient words been uttered than GATA’s Chris Powell in Washington in April, 2008 – when he opined, There are no markets anymore, just interventions.

The recent decoupling in price of gold as measured by the spread between the futures price and the cost to obtain physical ounces is a stark reminder that smart money is beginning to repudiate fiat money by seeking tangible ownership of goods perceived to posses value instead of derivative ‘promises’ to deliver the same.

The Oil Picture

Back in June, 2007, Market Watch reported,

Normally, Brent crude costs $1-$2 less than WTI crude, according to James Williams, an economist at WTRG Economics. At its peak, the price spread between the two topped $5, according to his data.

The article went on to explain,

WTI usually trades at a premium to Brent “because of the slightly higher quality, and the extra journey” oil tankers have to take to get the oil to the U.S., according to Amanda Lee, a strategist at Deutsche Bank. So “WTI minus dated Brent should be roughly equal to the freight rate,” she said. Indeed, “crude-oil prices usually depend on two things: quality and location,” said Williams. “The greater the distance from the major exporters, the greater the price.”

But here’s what’s happened recently in the global crude oil market:

Brent Crude trading at a 7 Dollar premium to West Texas Intermediate is like the SUN rising in the west and setting in the east – and no-one asking any questions why?

Thanks to the unearthing of the Fed’s Playbook Document, referenced above, along with cumulative knowledge of the existence of the President’s Working Group On Financial Markets [aka the Plunge Protection Team]; we know that interference in strategic markets with national security implications is now practiced commonly by the Government and the Fed working together. No other explanation for this distortion is plausible other than NYMEX regulators like the Commodities Futures Trading Corp. [CFTC – Plunge Protection Team members] are more brazen and actively complicit in market rigging of strategic commodities than their London counterparts. This manipulation is all being done in desperation; to preserve U.S. Dollar hegemony by perpetuating the illusion that inflation is being held at bay. Ample anecdotal evidence exists in a host of articles – particularly relating to derelict CFTC oversight of COMEX gold and silver futures – archived at kirbyanalytics.com to support this position.

Spiking VLCC Rates Reflect “The Movement to Tangibles”

The “unusual” premium for Brent Crude is even more perplexing given that crude oil shipping rates [unlike their dry goods shipping counterparts, as depicted by the Baltic Dry Index] for VLCCs [very large crude carriers] have, as recently as Dec. 2008, been enjoying robust and improving charter rates,

Last week the spot rate for Suezmax tankers was in the low $40k per day range. Yesterday, I check the rates and they have popped to over $90k this week! VLCC (very large crude carriers, i.e. supertankers) rates have not jumped as much but appear to be following the trend. So what is the deal here? Oil prices are falling and so is the apparent global demand for oil. Are not oil tankers just sitting around idle like the dry bulk carriers?

The answer is somewhat counter intuitive. The spike in spot tanker rates is actually the result of the low oil prices. Many tankers are being leased on the spot market as storage tanks. Oil producers, for whatever reason, do not want to significantly slow their oil production, but at the same time do not want to sell it for $45 a barrel. So they are leasing tankers to store oil in the hope or belief that oil prices will recover shortly. Two names in news articles that I have read doing this are Royal Dutch Shell and Iran. The majority of the planet’s oil production is owned by national oil companies that have policy and employment as well as financial reasons to keep the oil flowing. So at least in the short term, the current low oil prices are a boon for tanker owners.

Oil tanker companies, like their dry cargo brethren, can sign their ships to either long term, multi-year leases or charter them on the spot market where they are leased for a single voyage at the current spot rate.

The fact that “smart money” is now paying elevated prices to lease very large crude carriers [to store physical crude for later sale] is further evidence that faith in fiat money is waning simply because – you can do the same “trade” on paper – utilizing futures – without the bother and nuisance of leasing ships and handling the physical. Ask yourself why smart money has recently become engaged in buying ‘relatively illiquid’ physical crude oil, in a world allegedly awash in the stuff, for resale at a later date – instead of playing futures, accepting promises and holding cash?

Smart money is in the process of losing confidence in cash.

Interest Rates

It is vital that everyone understand that the function of interest rates in a system of usury is to solemnly act as the efficient arbiter of capital – rising to restrict money / credit growth when the economy overheats and falling to create the opposite when the economy cools.

Interest rates no longer serve this function.

As deceitfully disastrous as the surreptitious interventions in the crude oil and gold markets has been – they pale in comparison to the travesty which has been perpetrated through the premeditated hobbling of usury.

The roots of this most wicked experiment are traceable to the appointment of Alan Greenspan as Chairman of the Federal Reserve and then to academia – Harvard – where Robert Barsky and Lawrence Summers co-authored an academic research paper in the 1980s titled, Gibson’s Paradox and the Gold Standard. The “elevator speech” of what the paper examined was the co-relation between bond prices, inflation and the price of gold and, by extension, theorized that interest rates could be driven down [or kept low] – without sacrificing the currency – in the face of and despite profligate monetary policy so long as gold prices declined or did not rise.

After a stint as Chief Economist at the World Bank, Mr. Summers brought this “theory” to Washington mid-way through the first Clinton Administration [late1993] as Under Secretary of Treasury to Robert Rubin where he began laying the groundwork – with co-conspirators Greenspan, Rubin and Clinton – for the implementation of his “theoretical research”:

Gold price suppression began in earnest concurrently with changes in how the Office of the Comptroller of the Currency [OCC] begins records the mushrooming growth of derivatives [mostly interest rate swaps which – absent end user demand – only create artificial demand for government bonds]:

The Federal Reserve acting in cahoots with the U.S. Treasury utilizing the futures pits in N.Y. [COMEX] and the obscenity that has become J.P. Morgan’s Derivatives Book – the Fed / Treasury combo seized control of both the gold price and interest rates. The mechanics of how interest rate swaps were utilized to suppress interest rates is chronicled and explained in detail at Kirbyanalytics.com in a paper titled, The Elephant in the Room.

Subscribers are reading about the logical implications, and what comes next, as a result of the market manipulations outlined above as well as actionable suggestions to help insulate your investment portfolio from the inevitable fallout.

====================================================

Gata’s Tenth Anniversary: Gold Manipulation Evidence Mounts-Gold Seek.Com

By: Bill Murphy of LeMetropole Cafe

“Faced with the choice between changing one’s mind and proving that there is no need to do so, almost everyone gets busy on the proof.” … John Kenneth Galbraith

“An error does not become truth by reason of multiplied propagation, nor does truth become error because nobody sees it.” … Mahatma Gandhi

GO

This week marks GATA’s tenth anniversary of our efforts to expose the manipulation of the gold market. In another few weeks we will mark the tenth anniversary of my appearance on CNBC (interviewed by Ron Insana) … the first and last GATA appearance on the US TV media to date … for once they heard what GATA had to say, we have been blackballed ever since. It also marks a shameful period for the US financial market press, which is now clamoring for answers as to how we ever got in the financial market/banking mess we are presently facing. For that answer they ought to first look at themselves and their dismal way of kowtowing to the rich and powerful, and banning those who are willing to challenge the Orwellian grip on what Americans are allowed to hear and know.

America is facing quite a dichotomy at the moment. We are on the Inaugural Eve of our first black President, with all the hopes and dreams he is envisioning for our country. At the same time we are enduring the most horrific financial crisis since the Great Depression.

President-elect Obama, a superb orator, is calling for Americans to pull together to effect the CHANGE he called for in his campaign, and for all of us to contribute individually to make that change happen. He has wisely warned of the tough times ahead while going all-out to ready policies ASAP which he believes are the correct way to remedy the growing economic problems of the day.

He has also assembled an economic team of advisors which are acclaimed and generally very highly regarded … including Robert Rubin, Lawrence Summers, Timothy Geithner and Paul Volker. Unfortunately for the GATA camp, they are the ALL-PROS of the gold price suppression scheme. It is almost like our worst nightmare. On paper it represents anything but change as far as US gold policy is concerned, and has the potential to make our investment lives miserable for years to come. After all…

*Robert Rubin coined the phrase “US Strong Dollar Policy,” and flaunted the phrase. Rigging the price of gold was that policy’s lynchpin. What else was there? Steve Forbes was on Fox News Saturday talking about how important he believes it is for America to MAKE the dollar strong again. He talked sheepishly about gold in vague terms and referred to Rubin.

Robert Rubin hatched the gold price suppression scheme while running Goldman Sachs’ operations in London. This was many years ago, when interest rates were very high (say from 6 to 12% in the US). Rubin had Goldman Sachs borrowed gold from the central banks at about a 1% interest rate. Then he sold the gold into the physical market, using the proceeds to fund their basic operations. This was like FREE money, as long as the price of gold did not rise to any sustained degree for any length of time.

He continued his innovative money ploy as CEO of Goldman Sachs in New York and then put his Strong Dollar Policy ploy on steroids as Treasury Secretary under President Clinton.*Lawrence Summers followed Rubin as Clinton’s Treasury Secretary, and who could be more qualified to continue Rubin’s gold price suppression scheme than him? After all, while at Harvard he co-authored a paper, “Gibson’s Paradox and The Gold Standard.” The bottom line of Summers’ analysis is that “gold prices in a free market should move inversely to real interest rates.” Control gold and it will help to control interest rates.

Obama has designated Mr. Summers to be the Director of the U.S. National Economic Council.

*Which brings us to Timothy Geithner, who is President-elect Obama’s nominee to be U. S. Treasury Secretary. Geithner was named president and chief executive officer of the Federal Reserve Bank of New York on November 17, 2003. In that capacity, he serves as the Vice Chairman and a permanent member of the Federal Open Market Committee, the group responsible for formulating the nation’s monetary policy.

Mr. Geithner joined the Department of Treasury in 1988 and worked in three administrations for five Secretaries of the Treasury in a variety of positions. He served as Under Secretary of the Treasury for International Affairs from 1999 to 2001 under Secretaries Robert Rubin and Lawrence Summers.

Geithner is also happens to be a member of the Bank for International Settlements and since 2005 has been Chairman of the Committee on Payment and Settlement Systems. You might want to see what The CPSS undertakes “at their own discretion” as listed here:

http://www.bis.org/cpss/index.htmLike outgoing Treasury Secretary Hank Paulson, Tim Geithner is a graduate of Dartmouth College. Talk about knowledge of the gold price suppression scheme!

*And then there is the venerable Paul Volcker, who so effectively brought down runaway inflation in the US, starting in 1980. His one regret:

“Joint intervention in gold sales to prevent a steep rise in the price of gold (in the 1970s), however, was not undertaken. That was a mistake.” … Former Federal Reserve Chairman Paul Volcker (writing in his memoirs).

All-Pros? All-World is more like it when it comes to devotees of suppressing the price of gold. Outside of Volcker, the other three are those most responsible for making it happen in the first place.

So what’s the point? To get us all depressed over what lies ahead? NO, just the opposite.

On December 18th, on GATA’s behalf, I met with Bart Chilton, a CFTC commissioner who showed interest in hearing what we had to say. There were three others from the CFTC in attendance, including Elizabeth L. Ritter, Deputy General Counsel of that organization.

From my MIDAS commentary later in that afternoon…

Bart listened intently and took notes, as did one of the others, and asked numerous questions. Basically, I laid out our GATA presentation as I explained in the Sunday Midas. I am not going to get into all the details of what they said, as we will see what takes place in the months to come … except to say that I chuckled when saying to them if they really wanted to comprehend what the real gold price suppression scheme is all about, all they have to do is go to their new proposed Chairman … at the right time. No one knows what is going on better than he does.

(Insert- Gary Gensler was nominated that day to be the new chairman of the CFTC. Gensler was Undersecretary of the Treasury (1999-2001) and Assistant Secretary of the Treasury (1997-1999).

Gensler spent 18 years at Goldman Sachs, one of the ringleaders of The Gold Cartel, making partner when he was 30, becoming head of the company’s fixed income and currency operations in Tokyo by the mid-90’s.

As the Treasury Department’s undersecretary for domestic finance in the last two years of the Clinton administration, Gensler found himself in the position of overseeing policies in the areas of U.S. financial markets, debt management, financial services, and community development. Gensler advocated the passage of the Commodity Futures Modernization Act of 2000, which exempted credit default swaps and other derivatives from regulation.

Could The Gold Cartel have recruited a better ALL-PRO/ALL-WORLD man for their team? It is also important to keep in mind that chairman of the CFTC is one of the four members of the President’s Working Group on Financial Markets. Now why does a bureaucrat need to participate with the President and US Treasury Secretary on the markets? I thought the CFTC was supposed to regulate them, not be a part of policy.)

I did not hold back and said the main culprit of The Gold Cartel was our own government (their own boss), who has been in league with bullion banks like JP Morgan Chase, and others, to suit their own hidden agenda….

I was very impressed with Bart Chilton (very sharp guy) and he mentioned that my trip to D.C. would not be in vain.

***

What I stressed most at the meeting was that the gold price suppression scheme would not survive another four years, over the length of Obama’s elected term … and presented lengthy documentation to prove my point … meaning The Gold Cartel would run out of enough available central bank gold to meet a growing annual supply/demand deficit over the next four years. The bottom line was that Obama could stop the gold price manipulation scheme now and allow the price of gold to trade freely, thereby letting the Bush Administration be the fall guy; or he could let his economic team persuade him to carry on the status quo, in which case the price of gold will blow sky high in the years ahead, and he would have to take the blame for the resulting ramifications … especially when the gold scandal becomes a huge public ordeal.

What better way for Obama himself to understand the true gold situation than to ask his top economic advisors what the real deal is. If GATA is correct, and we have been on target for years, the U.S. has a BIG problem when it comes to its gold reserves (how much of it has been encumbered and is therefore GONE?) That is an essay unto itself, with many variables to be discussed, and for another time. All Obama has to do is get the five above-mentioned gentlemen in a room and get right to the nitty-gritty. They can start with the extensive package I handed to Bart Chilton, who is a member of the Obama transition team, and someone who once worked for Tom Daschle, formerly the Democratic leader in the Senate for ten years, and is now Obama’s Secretary of Health and Human Services nominee.

What Bart Chilton does with what I gave to him is his business, but since he told me my visit would not be in vain, I assume GATA’s extensive presentation did not go into the dumpster.

Meanwhile, in GATA’s tenth anniversary year, we are making our own call for CHANGE, and are pressing on. Obama has stated over and over again he wants THE PEOPLE to be represented and asked us to give him input. Who has more pertinent input go get to him than our camp? Therefore, we are asking everyone interested in a free gold market to make a renewed effort to further disseminate our decade’s worth of evidence of gold market manipulation into the public domain by contacting the financial market media and to others in the Obama transition team (if you have any contacts).

I know how frustrating it has been to get the jaded financial market media to listen to, and then acknowledge, what we have to say, but that was yesterday and perhaps times have changed due to the growing financial market crisis, and yearning to understand how we got here. After all President-elect Obama is urging for “government accountability” and “transparency.”

This call to arms has been instigated by the dramatic and sudden discovery of an important document buried in the Federal Reserve’s archives by writer and researcher Elaine Supkis. This document is posted on her blog at:

http://emsnews2.wordpress.com/2009/01/15/1961-top-

secret-fed-reserve-gold-exchange-report/

The document, which is marked “Confidential,” is from the papers of William McChesney Martin, Jr., and this collection is held by the Missouri Historical Society. A scanned image of the original document is posted by the Federal Reserve Bank of St. Louis at the following link:

http://fraser.stlouisfed.org/docs/histor ical/martin/23_06_19610405.pdf

Most importantly, GATA consultant James Turk has brilliantly dissected this document in an essay titled, “The Federal Reserve’s Blueprint for Market Intervention,” which has been served at The Matisse Table and at www.GATA.org…

http://www.gata.org/node/7095The title of this confidential report is:

Confidential – – (F.R.)

U.S. Foreign Exchange Operations: Needs and Methods

James Turk notes:

In short, it lays out what the Treasury and Federal Reserve needed to do in order to begin intervening in the foreign exchange markets, but there is even more. This document plainly shows what happens when government operates behind closed doors. It also makes clear the motivations of the operators of dollar policy long described by the Gold Anti-Trust Action Committee and its supporters — namely, that the government would pursue intervention rather than a policy of free markets unfettered by government activity. The run to redeem dollars for gold had put the government at a crossroads, forcing it to make a decision about the future course of dollar policy. This paper describes what the government would need to do by choosing the interventionist alternative.

This document provides primary, original source supporting evidence that GATA has been right all along.

I have long hoped that a “confidential” document like this one would eventually emerge. There are no doubt countless more like it, as evidenced by the Federal Reserve’s and the Treasury’s refusal to provide all the documents requested by GATA under its recent Freedom of Information Act request. Maybe those documents will eventually see the light of day too.

***

James makes a key point regarding one of the assertions of this report…

“The basic purpose of such operations would be to maintain confidence in the dollar.”

James T notes…

“This statement confirms one of the basic planks of much of the work by me and others that has been published by GATA over the years. The efforts to cap the gold price have one aim. It is to make the dollar look worthy of being the world’s reserve currency when in fact it is not.”

***

This significant report was written some 48 years ago, yet could have been written at any time in the past 10 years during which GATA has discovered blatant manipulation of the prices of gold and silver … as well as noted ludicrous counterintuitive dollar market action, which has been most noticeable in recent days, as our hysterical financial crisis in the US intensifies.

James Turk’s title says it all: it is a blueprint for the gold price and financial market manipulation so prevalent now. Ironically, there is a common misconception out there that the US is in the financial market mess it is in today because of too much deregulation. To some extent that is very true, as the likes of Secretary Paulson and Gary Gensler urged Congress to allow the US investment banks to increase the allowable debt/credit on their books from 12:1 to 40:1.

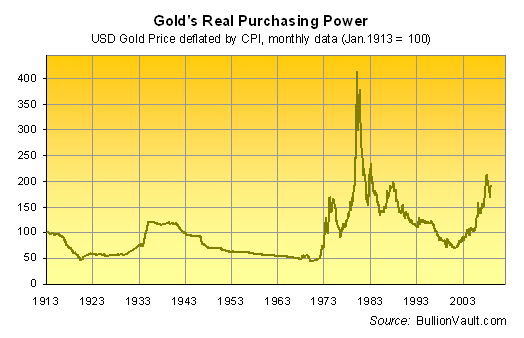

Yet, just as big a problem was the secretive interference in the US financial markets which allowed credit and risk issues to go completely out of control in America … meaning too much secretive market manipulation … and in a hidden way, too much regulation. Had the gold market not been artificially suppressed and allowed to trade freely, the price would have soared these past years, interest rates would have risen dramatically, and there would have not been the reckless investment bank shenanigans that have put our financial system in such peril. Simplistically, it is generally acknowledged that if gold had been allowed to keep up with inflation for the past 28 years, the price would be over $2,000+ per ounce. The GATA camp knows why it is not there RIGHT NOW!

Had the Plunge Protection Team (Working Group on Financial Markets) not stepped up their constant Hail Mary play activity after 9/11 to drive the DOW mysteriously higher in the last hour of trading on the New York Stock Exchange, the market probably would have broken down much earlier than it did and given the investing public more of a clue that something was wrong, instead of the misleading Stepford Wives drill that “Everything is fine.”

What is profoundly disturbing about the discovery of this confidential document is it fits in with much grander conspiracy theories than where GATA is coming from. Since this document, based on what has happened, really is a blueprint for market manipulation since 1961, it feeds into the worst fears of those who are constantly on the case about the Bilderbergers, Council on Foreign Relations, Trilateral Commission, and so on. This document to William McChesney Martin, Jr. is EXACTLY what I have been seeing and reporting over the past decade … not that much different than those who pointed out the Madoff Ponzi scheme during the same period of time. To learn that this market deception and manipulation was conceived when I was a freshman in high school is almost beyond comprehension, especially since the Wall Street crowd hasn’t permitted a serious discussion about it ALL THIS TIME! Nor has our government allowed a true independent audit of US gold reserves since the Eisenhower Administration in 1955.

It also feeds right into the scary notion revealed in a famed President Clinton comment that goes something like … “I didn’t realize I wouldn’t be in control here when I became President.” … meaning there were far more powerful background forces pulling the strings and on how he must operate.

GATA doesn’t want to go there, but based on this new discovery, it certainly opens up further comments for fair game, even for some of GATA’s Board of Directors. Adrian Douglas (an oil industry consultant who is presently off to Angola) sent the following email to James Turk:

James,

Congratulations. This was an excellent analysis. What a stunning document! Real dynamite.

It got me thinking as to whether the heist they have pulled is bigger than we think. The BIS as we know, and as mentioned in this memo, is the organization that allows for cooperation behind the scenes of the Central banks. We know they went private to prevent any need for public disclosure seeding the opportunity for Reg Howe’s lawsuit. We have plenty of evidence that Central Bank gold holdings have been depleted. We keep saying that the gold is “gone”. But what do we mean by “the gold is gone”? Gold is not like crude oil, expensive wine, even silver… it does not get consumed. It has not “gone”; it has changed ownership. The Central Banks leased out gold to the bullion banks. Now who did the the bullion banks sell the gold to? We know that the bullion banks can’t get the gold back. If the central banks ask for the gold back the bullion banks can declare bankruptcy or settle in cash. How convenient! The Central bank gold has gone into someone else’s hands that are unknown and the loss will eventually be written off. We know that Central Banks are owned or controlled by some of the richest families and/or entities in the world. Is it possible that these “bankers” can benefit from a fiat Ponzi scheme while it can be maintained AND still end up with the gold in which case they can benefit from a return to a gold standard and when the gold standard eventually gets abused and abandoned in the future they will play the whole fiat game over again? It would certainly require cooperation between central banks to pull off such a heist.

It would be great to have the whole world sitting in a room and ask those who own more than 10 million ozs of gold to raise their hands!

The crime may be more than manipulating the price of gold to “defend the US dollar” and concealing the evidence from the public. The Cartel may well have aided and abetted embezzlement of the citizens’ gold of the Western world. And who ever has it, they bought it perfectly legally from the bullion banks with fiat currency.

This seems to make sense because Central bankers and the “elitists” (Rockefellers, Rothchilds, Morgans, Mellons, Carnegies, Vanderbilts etc etc) are not stupid. They must know gold is real money. They can study monetary history too. The fiat money game in this context is a decoy for the theft of sovereign gold.

It is not without precedent, the great inflationist, John Law, was arrested escaping with a coach loaded with gold and silver!

Is this a bridge too far in conspiracy theory?

Cheers

Adrian

Which provoked this reply from another GATA Board member, Catherine Austin Fitts (Assistant Secretary of Housing/Federal Housing Commissioner at the United States Department of Housing and Urban Development in the first Bush Administration)…

Adrian:

My hypothesis since 2001 is that the NWO is shifting assets out of sovereign governments and shifting liabilities back in. The goal is to reengineer global governance into the hands of private banks and corporations in a manner that dramatically centralizes control. This is why the creation of a genetically controlled seed and food supply, etc.

To achieve such centralization requires the centralization of the gold and silver stores. Whoever has the gold has the most powerful financial asset. So if you want a new centralized currency, you need a monopoly on gold and silver. I think part of the end game is to shift back to something involving some kind of gold standard.

If you use fiat currency to acquire ownership and control of all the real assets on the planet, then you need a gold standard to make sure you keep them.

So, it would not surprise me to see G8 and GATA start to move into alignment, strange as it may sound.

Catherine

Neither opinions are official GATA viewpoints, but they are intriguing, eye-opening and worth pondering.

When I met with Bart Chilton I said GATA’s high command is just a bunch of proud Americans who have stumbled across a profoundly disturbing situation. I showed the four CFTC individuals in attendance GATA’s full-page color ad in the Wall Street Journal on January 31, 2008. It was titled, “Anybody Seen Our Gold?” …

http://www.gata.org/node/wallstreetjournalSome of you are very familiar with this copy in the ad…

“The objective of this manipulation is to conceal the mismanagement of the US dollar so that it might retain its function as the world’s reserve currency. But to suppress the price of gold is to disable the barometer of the international financial system so that all markets may be more easily manipulated. This manipulation has been a primary cause of the catastrophic excesses in the markets that now threaten the whole world.”

… and then…

“Surreptitious market manipulation by government is leading the world to disaster.”

The DOW was a little below 13,000 at the time. I mean how right could we have been? Yet the US financial market press completely ignored this very visible ad. There was not even a query of what we were talking about and why we would spend $264,400 to make such a warning.

So now we are fast forwarding virtually a year later and the US financial markets and economy ARE in chaos. If soon to be President Obama really wants CHANGE and TRUTH, we will give him critical input on one way he can effect what he says he is looking to do.

To increase the likelihood that what GATA has discovered actually reaches him, GATA is asking all who read this, and agree with GATA, to make some small effort to get this commentary to the financial market media in the world, especially the US financial market press.

That means contacting writers and media outlets such as the Wall Street Journal, Washington Post, Washington Times, New York Times, Forbes, Fortune, CNBC, CNN, Reuters, Bloomberg, the AP, Fox News, Newsweek, Time, etc. In addition, sending this Tenth Anniversary GATA commentary to widely-followed internet bloggers would also be helpful; perhaps stirring up so many out there who are searching for the reasons behind what has happened financially and economically in the US and why.

In such troubling times, Obama’s coming Presidency has given optimism and hope to many. For that to occur there must be true change, the desires for which have swept him into office. President-elect had some army. And GATA has its army.

Please take a little time and make just a small effort to help Obama help himself, even if our issue is the last one he is thinking about at the moment. Funnily enough, it ought to be one of the first, as it is one of the most prominent ones which got us into the financial market/economic nightmare we are in today. After all, it is many of the same bullion banks/investment houses our government is bailing out that were so instrumental in the gold price suppression scheme. Our mission is to let him know, via all sources possible, what the heck has happened and continues to go on.

Bill Murphy

Chairman

Gold Anti-Trust Action Committee

Copyright (c) 1999 – 2009

Le Metropole Cafe, Inc

================================================

John Doody: A Winning Situation For Gold Stocks- Seeking Alpha

Source: The Gold Report

By: John Doody of The Gold Stock Analyst

Heralded as “the best of today’s best,” John Doody, author and publisher of the highly regarded Gold Stock Analyst newsletter, brings a unique perspective to gold stock analysis. In this exclusive interview with The Gold Report, Doody ponders the efficacy of the Keynesian approach, makes a case for gold equities and explains how the GSA Top 10 Stocks portfolio has outperformed every other gold investment vehicle since 1994.

The Gold Report: John, you’ve stated in your newsletter, Gold Stock Analyst: “It’s clear the U.S. is going down a Keynesian approach to get out of this recession/depression.” I am curious on your viewpoint. Will the Keynesian approach actually work, or will they need to eventually move over to the Chicago School of Free Markets?

John Doody: A free market approach of letting the crisis resolve itself would work, but would cause too much damage; we’d probably lose our auto industry, and it would take too much time. As Keynes said: “In the long run we’re all dead,” so the government is trying to get a faster resolution. The Treasury is pursuing his fiscal policy idea of deficit spending. They’re borrowing the money to bail out the banks. When Obama’s plan is implemented, which could be another $700 billion in stimulus, it will be funded with more borrowings.

Bernanke and the Fed are pursuing a loose monetary policy with a now 0% interest rate. There’s actually no way we can not end up with inflation. This is much bigger than ‘The New Deal’ under Roosevelt. And I think that the market disarray over the last several months has confused investors; but when the markets settle down, it’s clear to me that it will be up for gold and gold stocks.

TGR: Is there any economic scenario that you wouldn’t see gold going up in?

JD: Basically, we’re pumping money into the system, but it’s just sitting there. It’s not being put to work, so there are those who think that we are going to enter a deflationary era. But I can’t see that. Some don’t like Bernanke, but I think there’s probably nobody better prepared to be in his role.

Bernanke is a student of the Great Depression and knows the mistakes the Fed made then, such as forcing banks to upgrade the quality of loans on their balance sheets. His approach is to buy the banks’ low quality loans, enabling them to make new loans. They haven’t done much of the latter yet, which is probably a fault of the Fed not requiring the funds received for the junk to be redeployed, but they ultimately will lend more as that’s how banks make money.

He knows in the early 1930s we went into a deflationary period of falling prices. For three or four years prices were down about 10% annually. He fully understands the risks of that, one of which is the increased burden of existing debt payments on falling incomes. The debt burden is lighter in an inflationary environment and that’s his target. Long term, he knows he can cure inflation; Volker showed us how with high interest rates in the 1980s. But there’s no sure way to cure deflation, and so Bernanke’s doing everything possible to avoid a falling price level. And I think that, because this is a service-driven economy, companies won’t lower prices to sell more goods—they will just lay off more workers, as we’re seeing now. I don’t think we’ll get the price deflation of the ’30s, and I’m sure Bernanke is going to do everything to prevent it.

TGR: But aren’t we already in a deflationary period?

JD: Well, we may be to an extent; you can get a better buy on a car. But, to put it in the simplest terms, has your yard guy lowered his price, or your pool guy, or even your webmaster?

TGR: Yes, but people opt to do things themselves versus paying other people to do it.

JD: Maybe, but if they do, it won’t show up in prices—it will show up in the unemployment statistics. So if the yard guy, pool guy or webmaster don’t lower prices and their clients become do-it-yourselfers, the effect will show up in unemployment, not inflation data.

TGR: So if every major country in the world is increasing their monetary supply, we would expect inflation. Will there be any currency that comes out of this to be considered the new base currency, sort of like the U.S. dollar is now?

JD: Well, that’s the $64,000 question. We don’t really know and, because there’s no totally obvious currency, that is why the dollar is doing well of late. But the dollar is in a long-term downtrend, in part because interest rates in Europe remain higher than here. Higher interest rates, as you know, act like a magnet in attracting investment money, which first has to be converted to the higher interest currency and that bids up its value versus the dollar.

The Euro represents an economy about the size of the U.S., so there may be some safety there. You could argue for the Swiss Franc maybe, but you know the Swiss banks (Credit Suisse, for example) have had some problems, so we’re not quite sure how that’s going.

So, to me, the only clear money that’s going to survive all this and go up, because everything else is going to go down, is gold.

TGR: What’s your view of holding physical gold versus gold equities?

JD: I only hold gold equities. They’re more readily tradable; when gold goes up, the equities tend to go up by a factor of two or three times. Of course, that works to the reverse, as we know. As gold went down, the equities went down more. But because you hold them in a government-guaranteed SIPC account, it provides ease of trading—you don’t have the worries of physical gold. . .insurance, storage or whatever. You may want to hold a few coins, but that would be about it in my opinion.

TGR: On your website, your approach to investing in gold equities is to choose a portfolio of 10 companies that have the opportunity to double in an 18- to 24-month period with the current gold price.

JD: Yes. We don’t really look forward more than 18 or 24 months; but within that timeframe, say a year from now, we could reassess and raise our targets so that, in the following 18 to 24 months, the stocks, while having gone up, could go up more still. There are lots of opportunities to stay in the same stocks as long as they continue to perform well. We’re not a trading newsletter, and as you probably know, the way we define an undervalued stock is based on two metrics.

One is market cap per ounce. The market capitalization of a company is the number of shares times its price. You divide that by its ounces of production and its ounces of proven and probable reserves, and you see how the company’s data compares to the industry’s weighted averages.

Second, we look at operating cash flow multiples. Take the difference between the gold price and the cash cost to produce an ounce, multiply that by the company’s production per year, and you get operating cash flow. Divide that into its market capitalization and you get its operating cash flow multiple. We look at that this much the same as one looks at earnings per share multiples in other industries.

For reference, we last calculated the industry averages on December 29, 2008 for the 50+ gold miners we follow, which is everyone of significance. At that time, the average market cap for an ounce of production was $3,634, an ounce of proven and probable reserves was $194, and the average operating cash flow multiple on forecast 2009 production, assuming $900/oz gold, was 7.4X.

We focus companies that are below the averages and try to figure out why. An ounce of gold is an ounce of gold, it doesn’t matter who mined it. If you’re going to buy an ounce of gold from a coin dealer, you want to get the cheapest price. Well, if you’re going to buy an ounce of gold in the stock market, you should want to get those at the cheapest price, too. It’s oversimplified, as there are other factors to be considered, but this is a primary screening tool to determine which stocks merit further study. The method works, as the GSA Top 10 Stocks portfolio has outperformed every other gold investment vehicle since we began in 1994.

TGR: Are all the companies in your coverage producers or have 43-101’s??

JD: Yes, all are producing or near-producing. They may be in the money-raising stage to build a mine, but they’ve got an independently determined reserve. And that part of the market has done better than the explorers because it has more data to underpin the stocks’ prices.

TGR: And you focus in on having 10 just because, as you point out in your materials, it allows you to maximum upside at minimum risk (i.e., if one of the 10 goes down 50%, you will only lose 5% of your money). Is your portfolio always at 10 or does it ever expand more than that?

JD: No, earlier in 2008 we were 40% cash, so it was six stocks. For a couple of months later in 2008 it was 11 stocks. But 90% of the time it’s at 10.

TGR: What prompted you to be 40% in cash?

JD: That was when Bear Stearns was rescued in March and gold went to $1000; we were just uncomfortable with that whole scenario. And actually we put the 40% in the gold ETF; so it wasn’t true cash.

TGR: Okay. And as you’re looking at these undervalued companies, are you finding that there are certain qualifications? Are they typically in a certain area, certain size?

JD: While we follow Barrick Gold Corporation (NYSE:ABX) and Newmont Mining Corp. (NYSE:NEM) and they’ve both been Top 10 in the past, neither is now. We’re currently looking further down the food chain. There’s one with over two million ounces growing to four million a year. Another has a million growing to two million. So, some are still pretty good sized. And then there are others further down that are either developing mines or are very cheap on a market cap per ounce basis.

Earlier, one of the Top 10 was selling at its “cash in the bank” price. We’ve had a nice little rally since October and this stock has doubled, but it’s still cheap. It has 9 million ounces of reserves at three mine sites in European Community nations, and it’s not Gabriel in Romania. It has no major troubles with permitting its mines and it was selling at its cash/share. Then the chairman of the board bought 5 million more shares. It was already top 10, but I pointed this out to subscribers as great buy signal. It’s doubled since and will double again, in our opinion.

TGR: Can you share with us some of the ones that are in your top 10?

JD: Well, the astute investor would probably recognize Goldcorp (NYSE:GG) as the one at two million ounces growing to four million ounces. Their tremendous new mine in Mexico, Penasquito, which I have been to and written about, is going to average half a million ounces of gold and 30 million ounces of silver a year. It’s going to be the biggest producing silver mine in the world, momentarily anyway, and will produce huge quantities of lead and zinc. At current prices, it’s going to be a billion-dollar-a-year revenues mine, which is enormous. And because of by-products, and even at current prices, the 500,000 ounces of gold per year will be produced at a negative cash cost per ounce.

TGR: Wow. Because of the credits?

JD: Because of the by-product credits. Another one would be Yamana Gold Inc. (NYSE:AUY), which is growing from a million ounces to two million ounces. Both Yamana and Goldcorp are in politically safe areas—no Bolivia, no Ecuador, no Romania—none of the places where you have to take political risk. I think we’ve learned enough from the Crystallex International Corp. (KRY) and Gold Reserve Inc. (NYSE:GRZ) situation in Venezuela, where they’re both on portions of the same huge deposit that is probably 25 million ounces or more. It looks to me that the government is going to take it away from them. So, I would just as soon not be involved in that kind of political risk scenario. There’s enough risk in gold just from the mining aspects of it that you don’t have to take chances on the politics too, as in some nations that’s impossible to assess.

TGR: Yes, another one that is really doing quite well is Royal Gold Inc. (Nasdaq:RGLD). Can you speak about that company?

JD: Yes. Royal Gold has been GSA Top 10 for 18 months now. We put it on in part because of the Penasquito deposit that I mentioned earlier. Royal has a 2% royalty on that, and 2% of a billion dollars is $20 million a year. Royal is unique in that they haven’t prostituted themselves by selling shares on a continuous basis. They only have 34 million shares outstanding and they will have royalty income this year of about $100 million. Penasquito is just coming on line, so its $20 million per year won’t be fully seen until late 2010.

Plus Royal pays a dividend. I think it could pay $1.00/share ($0.32 now). Dividend-paying gold stocks typically trade at a 1% yield. A $1.00/share dividend would make Royal a potential $100 stock. That’s my crystal ball down-the-road target.

Royal is a great play on gold price because they don’t have the aggravation of mining. They have a portfolio of mine royalties, plus a small corporate office. Royal employs 16 people, has $150 million in the bank and over $100 million a year income, which is about $3.00 per share pre-tax. Their biggest cost is taxes.

TGR: I see also that Franco Nevada Corp. (FNV.TO) has had quite a rise, though they have been kind of tumultuous between November and December.

JD: Franco is also a stock we like. About half of its royalties are from oil, so that’s why it’s suffered. The original Franco Nevada, as you know, was merged into Newmont for five years, and then they came public again in December ’07. I think it’s a good way to play gold and oil, and I think everybody agrees that oil is not going to stay in the $40 range for long.

TGR: John, can you give us a few more?

JD: A couple of smaller ones we like are Northgate Minerals Corp. (AMEX:NXG) and Golden Star Resources Ltd. [TSX:GSC]. Northgate is a misunderstood producer. Everybody thinks it’s going out of business when the Kemess Mine closes after 2011, but it’s actually not. It has 200,000 ounces a year from two mines in Australia and has a potential new mine in Ontario where they’ve just announced a 43-101 with over three million ounces. That’s potentially another 200,000 ounces a year, so we think they’ll remain at 400,000 ounces a year from Canada and Australia, both of which are countries we like. Cheap on our market cap per ounce of production and reserves metrics, it’s trading at an operating cash flow multiple under 2.0X.

Golden Star has several nearby mines in Ghana with production targeted at about 500,000 ounces in 2009. They’ve been ramping up to this rate for the past year and cash costs have run much higher than plan. If costs can be controlled and production goals met, it’s a takeover candidate for someone already in the country, such as Newmont or Gold Fields Ltd. (NYSE:GFI).

One thing I think readers should bear in mind is that gold mining will be one of the few industries doing well in 2009. Their key cost is oil, which is about 25% of the cost of running a mine. Oil’s price, as we know, is down about 75% in the $147/barrel high last July. At the average $400 cash cost per ounce mine, that’s a cut of about $75/oz off their costs. That result alone is going to give them an uptick in future earnings versus what they showed for third quarter 2008.

Something else people may not recognize is that currencies are also falling; many are down 20% to 40% versus the U.S. dollar. All the commodity nation currencies—the Canadian dollar, the Australian dollar, the South African Rand, the Brazilian Real, the Mexican Peso—they’re all down 20% to 40%. When your mining costs in those countries are translated back into U.S. dollars, they’ll be 20% to 40% lower.

So, the miners are going to have falling cash costs and even if the gold price remains exactly where it is now profits are going to soar. This will be unique in 2009. I can’t think of any other industry in which people are going to be able to point to and say, “These guys are making a lot more money.” I think the increasing profits will get the gold mining industry recognition that it isn’t getting now. Of course I’m a bull on gold because of the macroeconomic picture. When you put falling costs of production together with a rising gold price, you’ve got a winning combination for the stocks in 2009.

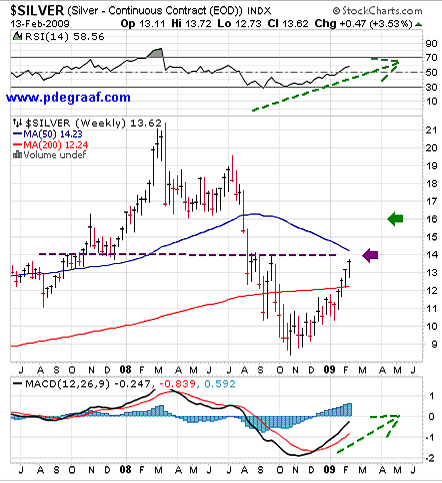

TGR: I was wondering if you could give us something on Silver Wheaton Corp. (NYSE:SLW).

JD: Well, Silver Wheaton is another royalty company; it’s not a producer. It gets its profit royalties by paying a cash sum up front and $4/ounce on an ongoing basis. It captures the difference between the silver price and $4 an ounce; if silver is $10 and it pays $4, it makes a $6 an ounce profit; at $20 silver, its profit would be $16. Aside from no pure silver miner actually producing ounces as low as $4.00, there’s a lot of leverage to silver price. I am not a silver bull, but because I’m a gold bull I think silver will follow gold higher.

Silver Wheaton is one of those companies that doesn’t have the issues of actually doing the mining. It has a portfolio of mines that it gets production from, and it owns 25% of the production from Goldcorp’s Penasquito mine that it buys at $4 an ounce, and will average about 8 million ounces a year. It’s just starting up now, but it will really get going in 2010. Silver Wheaton’s share of the total mineralization at Penasquito is 1 billion ounces. There’s 4 billion total ounces of silver there and it bought 25%. So, for a long time—the mine life of Penasquito is over 30 years—it’s going to be a big producing mine for Silver Wheaton.

TGR: Isn’t there a twin sister to Silver Wheaton in the gold area?

JD: Well, there’s Gold Wheaton Gold Corp. [TSX.V:GLW]. It’s based on the premise that some companies have a gold by-product. With their primary production in some other kind of metal, some might like to lay off the gold for a $400 an ounce on-going payment and an up-front purchase amount. Yes, some of the same guys are involved. I’m not convinced it’s going to do as well because it’s already got a lot of shares outstanding, and I just don’t like the capital structure as much. I wouldn’t bet against these guys but I’m not a believer.

TGR: And you said you’re not a silver bull. Why is that?

JD: We do cover about 15 silver miners, but reason number one for not being a bull is that it’s a by-product. Few mines are built to get just silver; 70% to 80% of silver comes as a by-product to copper, zinc, gold or some other metal. If you’re producing copper, you’re more interested in the copper price than you are in the silver price and you tend to just dump the silver onto the market.

And second, it’s not a monetary commodity. It is poor man’s gold—but it doesn’t have the universal monetary acceptance that gold does. It has a growing list of industrial uses, but it’s not growing at any rate that’s going to offset the falling use in photography. So, the overall demand for silver is not growing at any great rate. It’s not going to go from 800 million ounces a year to 1.6 billion ounces a year; it may get there in 20 years or 30 years, but that’s not our investment time horizon.

I think silver just follows gold along; but, in fact, it hasn’t been following gold along because right now silver is trading at a discount to gold. The ratio of gold to silver price, which normally runs around 50–55, is now around 80, so silver might have a little bit of a pop-up if the discount closes. But there are a lot of new silver mines coming on line and maybe that’s why the discount exists. Penasquito is one and Silver Standard Resources Inc. (Nasdaq:SSRI) has a big one starting in 2009. Coeur d’Alene Mines Corp. (NYSE:CDE) has now one ramping up and Apex Silver Mines Ltd. (AMEX:SIL) San Cristobal is now on line at 20+ million ounces per year as a zinc by-product. There’s potentially more silver coming to market than the world really needs. We do recommend Silver Wheaton, but that’s our single play.

TGR: Can you give us any comments on Minefinders Corporation (AMEX:MFN)?

JD: Well, you know, it’s in the uncertainty phase as to whether or not the new Delores mine in Mexico is going to work. Now built, it’s just starting up. We like the stock as we think it’s going to work. The question is: will it? Two mines in the area—Mulatos, owned by Alamos Gold Inc. [TSX:AGI], and Ocampo owned by Gammon Gold Inc. (GRS) did not start up smoothly. The market is betting against Delores starting smoothly, but this is the last of the three mines to come on line, and the first two mines—Alamos’ and Gammon’s—did get fixed and are now running okay. So, I think Minefinders has probably learned from the experience of the others, and the mine should start up all right. But, you know, the proof will be in the pudding. If you take its market cap per ounce on the forecast 185,000 ounces of production in 2009, or its almost 5 million ounces of reserves, and compare it to the industry averages we calculate, it’s potentially a double or triple from here.

TGR: So, the start-up issues of the other two mines, were they politically related?

JD: No, it was metal related. Processing facilities aren’t like televisions; you don’t just turn them on. It’s more like buying a new fancy computer system that needs to be twiddled and tweaked and loaded with the right programs. And you know, all geology is different, so things seldom start up properly; and, given the long teething problems at the other two mines, that’s sort of been a curse. If Minefinders can beat it and start up on plan, it’s an easy winner in 2009.

TGR: So, John do you have a prediction on where you think gold will go in ‘09?

JD: People talk about $2,000 or $5,000—it’s all pie in the sky, you know. Gold might get there; but the bigger question is: what’s the timeframe? Will I be around when gold is $5,000? I doubt it. Will it get there? Probably.

But we look for undervalued situations no matter what the gold price. And in the ‘90s—you know we’ve been writing Gold Stock Analyst since 1994—in the mid-90s gold did nothing for three years, it traded between $350 and $400. With our methods of selecting undervalued stocks, we had a couple of years of the Top 10 portfolio up 60% and 70% but gold was flat. Until mid-2008 the GSA Top 10 was up almost 800% in the current gold bull market. When gold does go up, the stocks go up more; but, in general, even if gold does nothing, we can still find good buys. Royal Gold is an example of finding winners in a tough market. Made a Top 10 stock at $23 in mid-2007, it gained 60% in 2008 and has doubled over the past 18 months.

We don’t follow the explorers, in part because there is no data to analyze beyond drill hole results, which are a long way from showing a mine can be built and operated at a profit. For us, the pure explorers are too much like lottery tickets. The producers do exploration and you can get your discovery upside from them. Bema Gold (acquired by Kinross Gold in February 2007) was a Top 10 stock with 100,000 ounces per year of production when it found Cerro Casale and it did very nicely on the back of that find. So, with the smaller producers you can get plenty of exploration upside. You don’t need to focus on the greenfield explorers because it’s just too hard to tell who’s going to win and who’s going to lose.

John Doody brings a unique perspective to gold stock analysis. With a BA in Economics from Columbia and an MBA in Finance from Boston University, where he also did his Ph.D.-Economics course work, Doody has no formal “rock” studies beyond “Introductory Geology” at Columbia University’s School of Mines.

An Economics Professor for almost two decades, Doody became interested in gold due to an innate distrust of politicians. In order to serve those that elected them, politicians always try to get nine slices out of an eight slice pizza. How do they do this? They debase the currency via inflationary economic policies.

Success with his method of finding undervalued gold mining stocks led Doody to leave teaching and start the Gold Stock Analyst newsletter late in 1994. The newsletter covers only producers or near-producers that have an independent feasibility study validating their their reserves are economical to produce.

==============================================

***All Posts are not to be considered Investment Advice, the articles/posts are presented for Informational Purposes. Consult Your Own Investment Advisors and Carefully Research and Read the Prospectus’s before making any Investment.*** jschulmannsr

As Always Bringing You The Must Have Information for Today’s Gold Markets and Hard Assets Investing- Dare Something Worthy Today Too! Brought To You By:- jschulmansr

There is another option, however, which involves debt holders taking a share of the losses. If steps are not taken to ensure that this happens, the greatest heist in history will have occurred: at least $1 trillion will be transferred from taxpayers to debt holders of failed financial institutions. This must not be allowed to happen.

Mark-to-Market vs. Real Losses

To understand the government’s dilemma, one must realize that the great majority of the not-yet-recognized losses in our financial system are not short-term, mark-to-market losses that will someday be reversed, but permanent losses. This is a huge misunderstanding that many people, especially those in Washington, seem to be suffering from.

To understand why the losses are real, consider this simple example: imagine a bank that lent someone $750,000 via an Option ARM mortgage to buy a McMansion in California at the peak of the bubble less than two years ago. Virtually all homeowners with this type of loan will default, thanks to declining home prices, the structure of the loan, and the fact that 70-80% of Option ARMs were liar’s loans. If we assume the house is only worth $400,000 today, then there’s been an actual loss of $350,000. That money will never be recovered. If one considers the millions of toxic loans made during the bubble – subprime, Alt-A, Option ARM and second mortgages, home equity lines of credit, commercial real estate, leveraged loans, credit cards, etc. – it easily adds up to at least $1 trillion in additional, unrecognized very real losses.

Imagine that New RTC buys this loan for $400,000. In this case, it might not lose money, but then the bank (or the structured finance pool) holding the loan has to immediately realize the loss of $350,000 – and it is certain that the U.S. (and world) financial system has not even come close to marking these assets to what they’re really worth, which explains why they won’t lend, even when given new money. Thus, if New RTC buys these assets at fair value, then the financial institutions suffer the losses – but this would bankrupt many of them. Yet if New RTC pays the inflated prices they’re marked at today, then it (and taxpayers) will suffer huge losses.

Who Should Bear the Losses?

To save our financial system, somebody’s going to have bear these losses – the only question is, who? Some fraction of this will certainly have to be taxpayer money, but all of it needn’t be if the government would stop bailing out all of the debt holders.

Government policy has been all over the map. Among the large financial institutions that have run into trouble (in chronological order, Bear Stearns, IndyMac, Fannie & Freddie, Lehman, AIG, WaMu, Citigroup and Bank of America), in some cases the equity was somewhat protected, while in others was wiped out, and likewise with the debt. Most likely due to the chaos that ensued after Lehman filed for bankruptcy, the current policy, as reflected in the most recent cases of Citi and BofA, is to at least partially protect the shareholders and, incredibly, 100% protect all debt holders, even junior/unsecured/subordinated debt holders.

The result is at least a $1 trillion transfer of wealth from taxpayers to debt holders. This makes no sense from a financial, fairness or moral hazard perspective. While there’s an argument that the government should protect senior debt holders to preserve confidence in the system (even though they knowingly took risk – after all, they could have bought Treasuries), the junior debt holders got paid even higher interest in exchange for knowingly taking even more risk by being subordinate in the capital structure (of course, equity and preferred equity holders are the most junior). These investors made bad decisions, buying junior positions in highly leveraged companies that made bad decisions, so why should they be protected?

Moreover, the reckless behavior of debt investors was a major contributor to the bubble. It was low-cost debt with virtually no strings attached that allowed borrowers, especially the world’s major financial institutions, to become massively overleveraged, fueling the greatest asset bubble in history. This was not an equity bubble – unlike the internet bubble, for example, stock market valuations never got crazy – it was a debt bubble, so it would be particularly perverse and ironic if government bailouts allowed equity holders to take a beating, yet fully protected debt holders.

Case Study: Bank of America

Let’s look at Bank of America (BAC), which effectively went bankrupt last week (disclosure: we are short the stock). The cost to taxpayers of avoiding this outcome wasn’t the headline $20 billion, but far more – the government is going to take a bath on the $120 billion that it guaranteed – and it’s likely that this is just the beginning of the losses.

Consider this: as of the end of 2008, BofA had $1.82 trillion in assets ($1.72 trillion excluding goodwill and intangibles), supported by a mere $86.6 billion in tangible equity – 5.0% of tangible assets or 20:1 leverage – and $48.9 billion of tangible common equity – 2.8% of tangible assets or 35:1 leverage (common equity excludes the TARP injection of capital in the form of preferred stock, which has characteristics of both debt and equity). (All data from BofA’s earnings release on 1/16/09; note that these figures include Countrywide, but not Merrill Lynch)

At such leverage levels, it only takes tiny losses to plunge a company into insolvency. It’s impossible to know with precision what BofA’s ultimate losses will be, but among the company’s loans are many in areas of great stress including $342.8 billion of commercial loans ($6.5 billion of which is nonperforming, up from $2.2 billion a year earlier), $253.5 billion of residential mortgages ($7.0 billion of which is nonperforming, up from $2.0 billion a year earlier), $152.5 billion of home equity loans (HELOCs; about $33 billion of which were Countrywide’s), and $18.2 billion of Option ARMs (on top of the $253.5 billion of residential mortgages; all of which were from Countrywide, which reported that as of June 30, 2008, 72% were negatively amortizing and 83% had been underwritten with low or no doc).