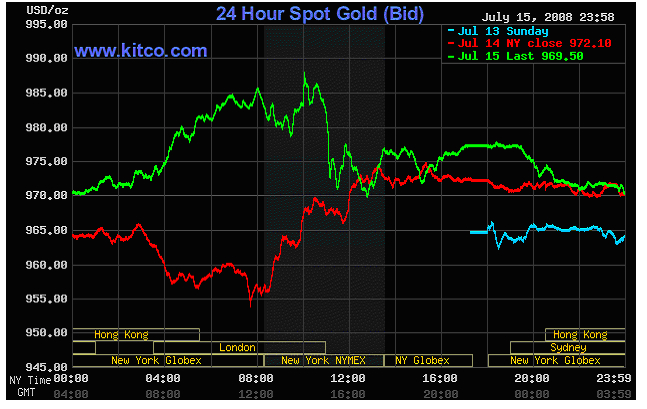

As I write Gold currently is up another $9.30 oz today! Even more importantly it is well above the psychologically important price level of $900 oz. A new high will confirm the breakout and BANG! we’re off to the races. Todays past has some good articles detailing why could could be breaking out here. Enjoy and Good Investing!- jschulmansr

============================================

Here is a safe way for even a small investor to get in on the Gold Rush! You can buy quantities as little as 1 gram to 1000’s of oz. I personally use Bullion Vault for my physical metal purchases.

Catch the New Bull! – Buy Gold Online – Safely, quickly, and at low prices, guaranteed! Bullion Vault.com

============================================

Could There Be a Real Breakout In Gold?— Seeking Alpha

By: Trader Mark of Fund My Mutual Fund

After a series of head fakes much of the past half year, the most watched move in the market might finally be “real” this time. With all the world’s printing presses going on overdrive, and currencies being mocked – gold “should” have been rocketing. Many theories persist on why it hasn’t, but really it does not matter. The price action is all that matters and this type of movement will get the technicians very interested.

Things to like

Things to like

1) a series of higher lows

2) the trendline of lower highs has been penetrated

Things to see for confirmation

1) any pullback is bought

2) price prints over October 2008’s highs, signaling the end of “lower highs”

When last we looked about 6 weeks ago [Dec 11: Dollar v Gold – Can we Trust this Change?] , it was just another headfake – this formation on the chart does look more promising.

These are 2 names; one in gold and one in silver we’ve had our eyes on.

Or just play it simple and go double long gold

Or just play it simple and go double long gold

==================================================

Happy Days For Gold? —Seeking Alpha

By: Jeff Pierce of Zen Trader

Gold was in the spotlight on Friday in a big way, nearly moving $39. Is this a hat tip to the big move that many goldbugs have been anticipating? Is all the money printing that the Federal Reserve finally catching up with the US Dollar? Should you have bought gold on Friday because it’s a straight line up from here? Let me preface my answers by saying that I’m a short term trader that will sometimes allow a trade to turn into a longer term trade but that doesn’t happen very often. I’m currently flat precious metals but will be looking for a good risk/reward, but for anybody reading this know that this analysis is from a momentum based perspective.

So the answers to the previous questions I believe are yes, yes, and no.

I’m a big fan of gold for a number of reasons (fundamental, technical, historical) but I know from experience that it trades much different from a momentum point of view. It tends to sell off once it goes outside it’s upper bollinger band as seen by the arrows above. Just when it looks like gold is going to bust out and move to blue skies it seems to run out of buyers and reverses. As you can see GLD and many individual gold miners moved outside this indicator on Friday and I expect a small pullback before it begins a new wave up.

Judging by the negative divergence on the RSI you can easily see that momentum is waning. As the stock has been making higher highs, the RSI has not been confirming the move. We could possibly move up to the 92 level before profit taking hits, but I just don’t see a good entry at this point if you’re not already invested in these stocks. It would be more prudent to wait for a slight low volume pullback before entering. The only problem with this way of thinking is there could possibly be many with this outlook and that could actually propel gold to higher levels, but I’m willing to risk that because if it does move up even more, then that will confirm the strength and I’ll buy even more on the eventual dip.

If you are long from lower levels I would consider taking some profits off the table now to prevent yourself from giving up any of your gains.

“I made all my money selling to soon.” ~ JP Morgan

I like silver’s chart a tad better from a technical aspect as the base that it’s been building since last September seems a little more stable. The RSI trendline has been steadily moving higher as the price has been trending higher which is very bullish. I think we’re a tad overbought here and will be looking to get long stocks such as PAAS, SLW, and SSRI when we pullback or move sideways for a week or two.

=================================================

Now- Some Commentary by Dennis Gartman

Dennis Gartman on Gold, Oil, Government and the Economy- Seeking Alpha

Source: The Gold Report

With a real roller-coaster year behind us, how would you characterize your macro overview of major economic trends for 2009?

Dennis Gartman: It’s abundantly clear that we have been in recession; we’re in a recession; and we’re likely to remain in a recession through the greatest portion of 2009. The monetary authorities around the world have done all the things they’re supposed to do, which is during a period of economic weakness throw liquidity in the system as abundantly, as swiftly, as manifestly as possible and expect the liquidity eventually to wend its way through the economy and strengthen economic circumstances. That may be sometime late in 2009. In the meantime, we’ll see continued bad economic data and continued increases in unemployment. It’s going to seem like things are really, really, really bad.

But let’s remember that things are always their worst at the bottom. By definition, recessions begin at the peak of economic activity when all economic data looks its best. So while things will start to look very bad through the rest of 2009, I bet that by late this year and early 2010 we will start to see economic strength coming at us because of the liquidity injections going on everywhere.

TGR: What will be the first signs that we’ve reached the bottom in terms of the recession and are starting to turn around?

DG: The signs of a turnaround will be that everybody believes that there are no signs of a turnaround. We’ll see Newsweek writing a series of cover stories talking about the end of Western civilization. The Financial Times of London headlines will read, “The Recession Seems Endless” and “Depression Is Upon Us.” Every day’s Wall Street Journal articles will be just manifestly bleak in nature. That’s what the signs will be.

And then all of a sudden, things shall begin to turn around. But the signs are always their worst at the bottom. That’s how things function.

TGR: So the popular press is in essence on a delay mode.

DG: Oh, it always is.

TGR: By three months, by six months, by a year?

DG: It’s probably a little less slow to react than it used to be, but let’s say three months.

TGR: So you like the fact that the monetary authorities have put liquidity into the system?

DG: Absolutely.

TGR: And it sounds as if you think it just takes time to work through the system.

DG: Always has; always will. That’s how these things go about. You have recessions because you had an economic advance where, in Greenspan’s terms, “irrational exuberance took over.” You have to dash that irrational exuberance and make it into irrational depression. Irrational, manifestly bleak, black philosophies have to make their way to the public. That’s just how these things happen; it’s happened time and time again.

The recession that I recall the most clearly is that of ’72-’74. We have to remember that unemployment was high up in double digits. We saw plenty of articles in the press about the new depression. If you go back and read articles from July through September of 1974, you will be convinced that we will never have an economic rebound in our lives again. Well, clearly, that’s just not the case.

TGR: What about the bearish people who say we’ve never seen worldwide conditions like this and that we’re in the “new era”?

DG: We probably haven’t seen the world going into recession at one time such as we are now. But I think that’s simply indicative of the fact that today’s communications are so much better. People in the United States or Canada or Europe really never would have known much about a recession in India 20 years ago, because the news media would not have covered it. Nothing told you about economic circumstances abroad. Now, with the Internet, information comes at you absolutely one-on-one.

All correlations have gone to one in this present environment. When stocks go down in the United States, they go down in India. When they go down in India, they go down in Vietnam. When they go down in Vietnam, they go down in Australia. That wasn’t the case 20 years ago; you didn’t have the small world united through communications that we have now. And now the correlations of emerging markets and large markets have all come together.

TGR: If that’s true, and worldwide financial markets are all tied together, could any given country “emerge” as a growth country while the rest remain in recession?

DG: Oh, it’s possible, but I don’t think we’ll call them “emerging markets” anymore. You’ll just find that one country pursued better economic policies, probably by cutting taxes or increasing government spending or doing away with some onerous legal circumstance that might have previously inhibited economic activity. The Chinese are doing any number of good things at this point, and that country may just have been more enlightened and it may come out of the recession faster than the others do. But now they won’t do it on their own, and anybody who does do it will be watched and understood much more swiftly than in the past. For example, did you ever know what was going on in Iceland 10 years ago? Of course not; but now you do.

TGR: Right. The only emerging markets we heard about were China and India. No one ever discussed South America.

DG: And now they’ve emerged. But now we understand. We hear news from Venezuela every day. Now we hear news from Sri Lanka every day if we want it; we can get it very easily. We couldn’t do that 10 years ago; 20 years ago clearly we couldn’t. That’s been the big change. Information travels so much more rapidly. That’s why all the correlations have gone to one. We are now one large economic machine that maybe one of the component parts does a little bit better, but it won’t shock anybody, and there won’t be anything “emerging.”

TGR: Back to the bear people. You referenced the ’72-’74 economy, but this time, many are pointing to the debt situation that the U.S. and probably a bunch of the world economies are in and the fact that we’re committing to billions—and in the U.S., trillions—of dollars more. Won’t that influx of new money have some kind of significant bear impact going forward?

DG: No, it will have a bullish impact. Unless all the rules of economics have been rescinded, money pushed into a system will push economic activity higher.

TGR: But it will also push inflation higher.

DG: Oh, that’s very likely to happen. The question is whether it will be inflation of 1%, 2%, 5%, or will it be a Zimbabwean-like inflation? The latter isn’t going to happen, and 1% isn’t likely going to happen. But 2% to 5% inflation? Yes, that’s likely to happen several years down the line.

TGR: Gold bugs are saying, “Buy gold now.” What would be your advice under these circumstances?

DG: I happen to be modestly bullish on the gold market, but not because of inflationary concerns. It’s more that I think gold has quietly moved up the ladder of reservable assets, a reservable asset being one that central banks are willing to keep on their balance sheets, all things being equal. Dollars are still the world’s dominant reservable asset. The Euro is next and gold is probably the third.

The Fed has thrown off a lot of other assets and taken on securities, debt instruments, mortgages and the like, but I think they’re doing exactly the right thing. Some central banks with a lot of U.S. government securities on the balance sheet may decide that going forward, they may buy more gold rather than more U.S. government securities if they’re running an imbalance of trade surplus. For instance, if I’m the Bank of China and I hold a minuscule sum of gold, maybe I should own a slightly larger minuscule sum.

TGR: That’s really diversifying your monetary assets.

DG: I think that’s all that will drive the gold prices quietly higher. I am not a gold bug; I don’t think the world’s coming to an end. I think the history of man is to progress. And yes, we have relatively large amounts of debt, but you can go back to the recession of 1974; you can go back to 1980-81; you can go back to the recession of 1907, and you will see the same arguments—that the world is too debt-laden. And the same arguments, the same language, the same verbiage was always written in exactly the same circumstances. Guess what? We moved on. This time might be different, but I’ll bet that it won’t be.

TGR: What would your recommendation for investors to do in gold? If they want to do any type of holding assets in monetary value, should they be looking at holding physical gold or buying ETFs or buying into the equity?

DG: For the past several years, I’ve told people that if they’re going to make the implied bet on gold, bet on gold. The gold bugs tell you that you have to own bullion. I say, no, you should really own the GLD, the ETF. It trades tick-for-tick with gold. If some truly untoward chaotic circumstance ran through the world’s banking system I guess maybe GLD and bullion would diverge at some point, but we’d have other problems long before that would occur. So if you’re going to make the implied bet on gold, bet on gold. Do the GLD.

TGR: But not physical gold?

DG: I do own some physical gold. But do I own a lot of it? No. And quite honestly, I hope I lose money on the physical gold I have. It’s an insurance policy. Nothing more than that.

TGR:: Are you looking at physical gold as the insurance policy or any investment in gold as an insurance policy?

DG: There’s the old saying, “Those aren’t eatin’ sardines; them is trading sardines.” Some gold I consider to be tradable, and that’s ETF-type stuff, and I have a small amount in the lockbox in the form of gold coins. That’s my insurance policy.

TGR: That would be what the typical investment broker might advise, 5% to 10% in gold.

DG: That’s it. Exactly, that’s it. Don’t get overwhelmed by it.

TGR: How about mining stocks?

DG: If you’re going to bet on gold, there’s nothing worse than being bullish on gold and owning some mine—especially in some junior fly-by-night—and walking in one morning and finding out that the mine you thought you had got flooded or all of your workers were unionized and walked off or management was somewhat derelict. You may have been right on the direction of gold, but your stock went down. So I’ve told people to stay away from the juniors; that’s a terrible bet on gold. If you’re going to bet on gold, bet on gold.

Maybe you’ll want to start punting on Barrick Gold Corporation (NYSE: ABX) or Newmont Mining Corp. (NYSE: NEM) or the real large names, rather than the juniors. There’s just too much risk in the juniors. Yes, everybody says, “I bought this junior at a nickel and now it’s at 15 cents.” Well, jolly for you, but you probably bought 15 others at a nickel, and they’re all bankrupt. If you’re going to bet on gold, bet on gold.

TGR: So you’re saying with that advice that if you want to bet on gold equity, bet on blue-chip gold equity stocks that have just been hammered down through the market.

DG: That’s correct, Agnico-Eagle Mines (TSX: AEM), ASA Ltd. (NYSE: ASA), the Newmonts, the Barricks, that sort of thing.

TGR: If we take that logic and look across the broad array of sectors, would you also recommend looking at other blue chips that have just been battered? Or do you think that some sectors will recover faster than others? Such as the financial sector, the energy sector, the housing sector, the precious metals sector?

DG: I’m really quite bullish on infrastructure—the movers and the makers of the things that if you drop them on your foot, it will hurt. I think I want to own steel and copper and railroads and tractors because I think we’re going to be building roads and bridges. That’s probably one of the things that probably will bring us out of the economic morass. Along those lines, I wouldn’t mind owning a little bit of gold at the same time.

TGR: Unlike gold that you can buy and own, if you look at steel and copper, are there specific companies and equities that are appealing to you?

DG: Again, as in gold, if I am going to buy gold equities, I’m going to buy the biggest names. If I’m going to buy steel, I’m going to buy the biggest names. U.S. Steel comes to mind. That’s the easiest; that’s the best; that’s where liquidity lives. It has been bashed down from the highs made last July; it’s down—what?—75% from its high. Recently it stopped going down and is in fact starting to go up now on bad news. So if you’re going to buy steel, buy the most obvious ones—U.S. Steel or buy Newcorp.

TGR: You talked about the energy market being weak in one of your recent newsletters. Do you see this weakness continuing or do you see a turnaround happening in ’09?

DG: The one thing that we can rest assured in the rest of the world is that OPEC chiefs cheat on each other—they always have and they always will. So when OPEC says that it’s cut production, that’s a lovely thing. No, they haven’t, and they don’t. Because the problem OPEC has is they’ve all raised their standards of living and the expectations of their people, and they all have cash flow requirements. You have to sell three times as much $50 crude oils as you sold $150 crude oil to meet the demands of your populace that you have increased. So the lovely thing from a North American perspective is that Chavez finds himself in a very uncomfortable position and needs to produce a lot more crude oil to keep his public happy. It’s rather comical, isn’t it, that Chavez was giving crude oil away to the Kennedy family to be distributed to people in the Northeastern United States until two weeks ago when he had to stop. He had to stop because he needs the crude oil on his own to sell, not to give away, to meet cash flow demands.

Iran is in exactly the same position. Isn’t it lovely to see that Putin, who was really feeling his military oats six months ago with $150 oil, has to pick fights with Ukraine and smaller countries now with crude at $45 a barrel? Where is crude going to go? I wouldn’t be surprised if we make new lows.

TGR: Will there be new lows for ’09? Are you buying into this whole peak oil argument that production eventually will be unable to meet demand?

DG: Do I believe that we’re going to run out of crude oil in the next 100 years? Not on your life. Sometime in the next 10,000 years we probably will run out of crude oil. In that instance, I am a peak oil believer. It’s not going to happen soon though. I remember they told me when I was in undergraduate school back in the late ’60s that we would be out of crude oil by 1984.

TGR: Do you mean out of oil? Or at a point where demand exceeds production?

DG: We would be out! Gone, done! There would be no more. Isn’t it interesting? We’ve pumped crude oil for 28 more years. This is an interesting statistic: We have either seven or eight times more proven reserves now than we had in 1969. And I think we have used a bit of crude oil between now and 1969.

TGR: Just a wee bit.

DG: A wee bit, and yet we have seven or eight times more proven reserves. Every year we have more proven reserves. So, yes, I’m a peak oil believer. Sometime in the next 10,000 years we will run out of crude.

TGR: With Obama now in office and talking about getting off our reliance on foreign oil, what’s your view of the future on all the alternative energies that are being so pushed by many people in the U.S. government?

DG: I think it’s wonderful job-creation programs, none of which will prove to be of much merit at all. All of the Birkenstock-wearing greens will feel very good about having their rooftops covered by solar panels, but is that going to resolve any energy problems we have? No. No. Nuclear power will do that. Maybe using the oceans will do that, but wind power, probably not. Solar power, probably not. It makes everybody feel good, but are we going to power our cars in the next 40 years with solar power? I doubt it. Do I expect some sort of material technological breakthrough in the next 100 years that will change what we use as energy? Oh, absolutely. Do I have any idea what it will be? Of course not.

TGR: If the price of oil if it remains low, is there a role for nuclear in the next 50 years?

DG: Oh, absolutely.

TGR: What will drive that?

DG: It’s absurd that we don’t use nuclear energy. Even the French derive 80% of their electricity from nuclear energy, cleanly, efficiently, without any problems whatsoever. Why we don’t do the same in the United States other than the left and the eco-radicals keeping us from doing it is really quite beyond me.

TGR: So, given that we still have eco-radicals and a big push toward alternative energies, do you see anything happening in the U.S. in nuclear in the near future?

DG: Yes, actually. It’s interesting. There are a lot of new nuclear facilities on the drawing boards, and they’re probably going to be approved. If there’s going to be one surprise by the Obama Administration, it will be that you don’t get nuclear energy advances under a right-wing government; you always get them under a left-wing government. Obama will be smart enough to understand that that’s the only way—that’s the best and cleanest methodology to use. And the left won’t argue with a fellow leftist pushing for nuclear energy. Only Nixon could go to China; only Obama can push nuclear energy.

TGR: And you think that he will?

DG: Oh, yeah, he’s smart enough to understand that.

TGR: Going back to your investment strategy, which big blue chip players in oil and nuclear would you point out as good investments?

DG: In oil, I’d want to take a look at companies such as ConocoPhillips (NYSE: COP), which dropped 70% from its highs. How can you go wrong with the Conocos and the Marathons and the large oil companies whose price-to-earnings multiples are down to at single digits and their dividend streams are 5%, 6%, and 7%? Why would you not want to own those? That’s the best investment.

And at the same time, the volatility indices on the stock market are so high that, gee, you can buy Conoco, get the dividend, and sell out of the money calls at very high premiums and ramp your dividend yield up. It’s like a gift; it’s like manna.

TGR: Well, what about in terms of the nuclear sector and uranium?

DG: I really don’t understand uranium. I don’t know where to go, and I don’t how to buy it yet. So I’ll just say there’s a future for it, but I don’t know what to do with it.

TGR: What other sectors should be looking at for 2009?

DG: Banks, banks.

TGR: They’re making a comeback. Do you think there will be more consolidations?

DG: There will be more consolidations; there has to be. But look at the yield curve—what a year to be a bank! The overnight Fed funds rate, the rate banks are going to pay depositors for their demand deposits or checking accounts is zero. And you’re going to be able to lend that out to hungry borrowers at 7%, 8%, 9%, 10% and 12%. The next three years will be the greatest three years banks have ever seen. Banks will just make money hand over bloody fist in the next three years.

TGR: Are you talking about the big boys?

DG: No, I’m talking about the regionals. The big boys have problems in toxic assets. I am not even sure there is a Peoples Bank & Trust in Rocky Mount, North Carolina, but a bank like that—or the First National Bank of Keokuk, Iowa or the First National, or the Peoples Bank & Trust of Park City, Utah—those are the banks that are going to make lots of money.

TGR: Do you see an explosion in regional banks? Will move of them come into the marketplace?

DG: I think we’ve probably got all we need. It’s just that they’re very cheap.

TGR: What will the role of the international banks be?

DG: Mopping up the disasters that they’ve created for themselves for the past decade, trying to survive, being envious of the decent regional banks that are going to be earning enormous yields on this positively sloped yield curve and wishing they were they.

TGR: Do you see a role long term for international banks?

DG: Oh, sure, of course. How could there not be? It’s a smaller world; it’s an international world; it’s a global world. International banks will be back in full force a decade from now. They’ve got some wound-licking to do, and they’ll do it.

TGR: In addition to regional banks as being a great play to look at for ’09, ’10, any other interesting plays to bring up?

DG: You want to own food and grains again.

TGR: Are you talking about grains or food producers like Nabisco?

DG: No, I think you want to own grains. If you’re going to make a speculation, I think you want to own on the grain markets again.

TGR: Grain for human consumption or grain for livestock consumption?

DG: Yes and yes.

TGR: Are you looking at buying that on the commodities market?

DG: You can actually buy that on ETFs now. The wonderful world of ETFs is just extraordinary. You can actually buy a grain ETF now. DBA (DB Agriculture Fund) is one; JJG (iPath Grains) is another. Those are basically long positions in the grain market. Wonderful things to use.

TGR: You like ETFs; but the naysayers will say that ETFs could be encumbered and there’s actually no guarantee that they hold any assets.

DG: That’s true; that’s correct.

TGR: But you’re comfortable that people should go into an ETF for grains?

DG: I didn’t say that. What I said is if you wish to trade in grain, there are ETFs that will do that. Do I know for sure that they will all perform perfectly and that if the world were to come to a chaotic banking circumstance that there wouldn’t be problems? I don’t know that. Does that bother me? No. It doesn’t bother me even slightly.

Should you worry about [not trading] an ETF just because there might be some problem under an untoward economic environment? No, it’s illogical. And shame on those people who say those sorts of things or who tell you not to use them because they ETF may not function properly if there is some total breakdown in the banking system. Well, if that happens, we have other problems.

TGR: And what’s your projection for the overall investment market? We’ve been hearing speculation that it will rise through April, bottom out even deeper than it is today, and then a slow climb in 2010.

DG: Gee, I have no idea. I just think that stock prices will be higher six months from now than they are now, much higher 12 months than they will be six months from now, and higher still in 24 months than they will be 12 months from now. But where will they be in April? Golly, I don’t know. I think the worst is far behind us and better circumstances lie ahead. And that’s the first time in a loooonnnng while that I’ve said that.

TGR: Yeah, now if the media will just catch up with you, we can enjoy watching it again.

DG: It won’t. Watch the news; it will just get bleaker and bleaker as the year goes on. And watch the unemployment rate; it’s going to be a lot higher.

TGR: Other than Barack Obama saying we’re going to start building infrastructure, do you anticipate any dramatic changes in the U.S.? Right now we’re a services country, and we need to move back to being a manufacturing country.

DG: We’ll never move back to being a manufacturing country. Won’t happen. Here’s an interesting bit of data. Do you know what year that we had the absolute high number—not just as a percentage of population—but the absolute high number of manufacturing jobs was in the United States?

TGR: Somewhere around the World War II era.

DG: Very good, 1943. We have lost manufacturing jobs since 1943. I think that’s a fairly well-established trend.

TGR: Is there a future for the services sector, though? That’s the key.

DG: It will be larger. And so what? It’s like saying we need more farmers. No. We need fewer farmers. We have one-hundredth as many farmers as we had at the turn of the 20th century. We now 500 times more grain? Seems to me every time we lose a small farmer, we get better. So, we need fewer farmers. And we need fewer manufacturing jobs.

TGR: But doesn’t that put the onus on the United States as the economic world leader? Considering the fact that, as you mentioned, information now is instantly available everywhere, just in terms of worldwide confidence; it seems like every time we hiccup, the planet hears it?

DG: There is probably some truth to that fact. But it is probably not us that will lead; it’s probably Australia or New Zealand or the Baltic States or some smaller country that actually changes policies and frees up markets and cuts taxes, and all of a sudden their economy starts to turn around. Then people elsewhere will say, “Oh, look! That’s the right thing to do. Let’s us go do that.”

TGR: Really? Economic recovery worldwide will not come from the United States?

DG: Well, if we don’t recover, the rest of the world won’t, but we won’t be the first. What I am saying is that some smaller country will do the right things faster than we do.

TGR: Isn’t what Australia does irrelevant to what the U.S. needs to do?

DG: No, it’s dramatically relevant. If Australia starts to do things properly—if Australia were to suddenly come out and slash taxes and go to a flat tax and cut paperwork by 50% and it’s economy starts to turn higher, wouldn’t that be a good incentive for us to do the same thing?

TGR: But that implies that every country should use the same economic strategy; that we’re all basically at the same state in our economic development. That what will work for Zimbabwe or China will work for the U.S.

DG: I think anywhere in the world that you have smaller government, lesser taxes—every time you do that, that economy, no matter where it is, does better. It does better. And anywhere you put higher taxes and more government, that economy usually does worse. It does; it just does.

TGR: You’re looking at it from a macro point of view.

DG: I’m looking at it just from an economic point of view, whether macro or micro. Look at Ireland, for example. Why was Ireland for many years the “Celtic Tiger” of Europe? Their tax regime was lower than the rest of Continental Europe. The Germans and the French, who are statists, who are collectivists, instead of emulating the Irish, kept trying to drag Ireland down to their level. Now, that was stupid, wasn’t it? That didn’t work.

My favorite example is New Zealand back in the 1980s. Every year from the 1970s through the 1980s, New Zealand ran a budget deficit and a trade deficit. Every year the IMF said, “You must raise your taxes and cut the value of your currency to try to balance your budget and run a trade surplus.” So New Zealand would do that, and every year the deficit got worse and their trade imbalance grew larger. They did this for five or six years and it got worse every time they did it—every time they followed the IMF tactic of raising taxes and cutting the value of the currency.

Finally New Zealand Treasury Secretary Graham Scott (Secretary from 1986–93) told the IMF, “Don’t ever come back here. Everything you’ve told us to do has proven to be utterly worthless. We’re going the other way. We’re slashing taxes.” From I think a 75% marginal tax rate, over the course of five years, they cut it to like 18%. And every year they took in more money—more money—every time they cut taxes they took in more money. And when they strengthened their currency, their exports picked up; as their currency got stronger, they exported more stuff. Isn’t it fascinating?

TGR: That’s the paradox.

DG: It got to be so interesting—it wasn’t Gordon Campbell—I’m trying to remember; I just went blank for his name. But he passed the baton on to a woman by the name of Ruth Richardson, who was a little more leftwing than her predecessor—the tax rate was down to a flat 18%. They asked her if she was going to cut it again, and she said, “You know, I don’t think I can cut it any more; I can’t spend the revenue I am taking in now.” It’s a classic line. So, what does she do? They actually started raising the tax rates again, and what happened? Tax revenues fell.

But New Zealand had taught a lot of people that cutting taxes and strengthening your currency is the best thing you can do. And as they were cutting taxes, they kept cutting prohibitions and regulations; they kept chopping them back. They were the real precursors of the Free Market Movement that developed in the early ’90s and the early ’00s.

TGR: Let’s hope the United States learns from that. Obama announced his tax cuts; we’ll see what comes of that.

DG: He said entitlements are even on the table. Can you imagine a Republican ever making that statement? They would boo him. But here’s a leftist who puts it on the table. He can say that.

Irreverent, outspoken, entertaining, sardonic and—in his own words, a “glib S-O-B,” Dennis Gartman has been producing The Gartman Letter for more than 20 years. His daily commentary on global capital markets as well as short- and long-term perspectives on political, economic and technical circumstances goes to leading banks, brokerage firms, hedge funds, mutual funds, energy companies and grain traders around the world.

A 1972 graduate of the University of Akron (Ohio), he undertook graduate studies at North Carolina State University in Raleigh (where he remains involved as a member of the Investment Committee.

Before devoting himself full-time to The Gartman Letter, Dennis analyzed cotton supply and demand in the U.S. textile industry as an economist for Cotton, Inc.; traded foreign exchange and money market instruments at North Carolina National Bank, went to Chicago to serve as A.G. Becker & Company’s Chief Financial Futures Analyst and then become an independent member of the Chicago Board of Trade, dealing in treasury bonds and notes and GNMA futures contracts; and moved to Virginia to run Virginia National Bank’s futures brokerage operation.

In addition to publishing The Gartman Letter, Dennis delivers speeches to audiences around the world (including central banks, finance ministries, and trade groups), teaches classes on derivatives for the Federal Reserve Bank’s School for Bank Examiners, and makes frequent guest appearances on CNBC, ROB-TV and Bloomberg television.

==============================================

Finally for the Technical Analysis Junkies (like me!) here is an awesome article!

===============================================

Market Leaders Hesitate on Stimulus Plan— Seeking Alpha

By: Chris Ciovacco of Ciovacco Capital Management

Proposed Economic Stimulus Plan May Not Stimulate Much

The new administration is proposing an $825 billion “stimulus” plan. Most of the package is geared toward helping existing or expanded programs such as unemployment assistance, law enforcement, food stamps, etc. Much of this spending will “save” existing jobs or keep existing programs already in place. This may help prevent things from getting worse, but it will offer little in the way of providing new stimulation for the economy. Another large portion of the stimulus plan is in the form of tax cuts. While depreciation incentives may spur some new business spending, credits to individuals may offer little incentive to spend given the state of their balance sheets and concerns about employment. After all the hype about infrastructure spending, only about 25% of the package is geared toward this area.

Tug of War Between Liquidity and Economic Weakness

The chart below was created on the website of the Federal Reserve Bank of St. Louis. It shows the eye-popping expansion of the money supply as financial institutions have swapped securities and other “assets” for cash via borrowing from the Federal Reserve. Borrowing prior to this crisis is barely visible on the graph. Recent borrowing is an extreme example of the term “spike” on a graph. Despite the never before seen tapping of the Fed, financial assets show little evidence of reflation taking place.

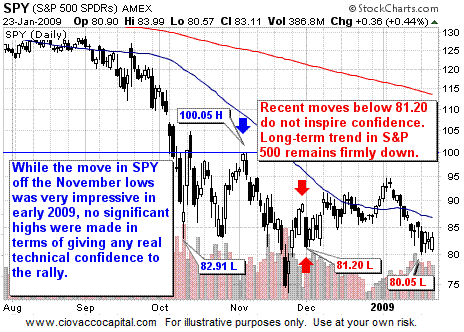

U.S. Stocks: Downtrend Remains In Place

U.S. Stocks: Downtrend Remains In Place

If you compare the long S&P 500 ETF (SPY) to the short S&P 500 ETF (SH), it is clear the short side of the market is in better shape. There is little in the way of fundamentals, except hope of government bailouts, to expect any change to these trends.

Recent weakness in the S&P 500 Index leaves open the possibility that we will revisit the November 2008 lows around 740 (intraday). If those lows do not hold, a move back toward 600 becomes quite possible. On Friday (1/23/09) the S&P 500 closed at 832. A drop back to 740 is a loss of 11%. A move back to 600 would be a drop of 28%. These figures along with the current downtrend highlight the importance of principal protection and hedging strategies. SH, the short S&P 500 ETF, can be used to protect long positions or to play the short side of the market.

Recent weakness in the S&P 500 Index leaves open the possibility that we will revisit the November 2008 lows around 740 (intraday). If those lows do not hold, a move back toward 600 becomes quite possible. On Friday (1/23/09) the S&P 500 closed at 832. A drop back to 740 is a loss of 11%. A move back to 600 would be a drop of 28%. These figures along with the current downtrend highlight the importance of principal protection and hedging strategies. SH, the short S&P 500 ETF, can be used to protect long positions or to play the short side of the market.

Gold & Gold Stocks Still Face Hurdles

Gold & Gold Stocks Still Face Hurdles

Friday’s big moves in gold (GLD) and gold mining stocks (GDX) have some calling a new uptrend. While recent moves have been impressive some hurdles remain.

Gold stocks (GDX) look a little stronger than gold, but any entry in the market should be modest in size. If $38.88 can be exceeded, our confidence would increase and possibly our exposure.

Gold stocks (GDX) look a little stronger than gold, but any entry in the market should be modest in size. If $38.88 can be exceeded, our confidence would increase and possibly our exposure.

Run In Treasuries Is Long In The Tooth

Run In Treasuries Is Long In The Tooth

Investments with the highest probability of success are those with positive fundamentals and positive technicals. Conversely, the least attractive investments have poor fundamentals and poor technicals. With the U.S. government issuing new bonds at an alarming rate, a continued deterioration in the technicals could signal the end of the Treasury bubble.

TBT offers a way to possibly profit from the negative forces aligning against U.S. Treasury bonds.

TBT offers a way to possibly profit from the negative forces aligning against U.S. Treasury bonds.

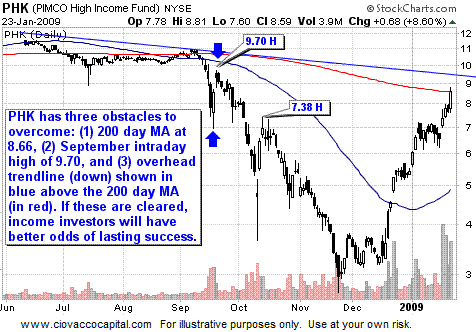

Strength In Bonds Shows Little Fear of Price Inflation

Strength In Bonds Shows Little Fear of Price Inflation

The government’s policies are attempting to stem the tide of falling asset prices. They hope to reinflate economic activity along with asset prices. The charts here show:

-

- A weak stock market (see SPY above), and

- An improvement in many fixed income investments (below: LQD, AGG, BMT, PHK, and AWF).

Weak stocks and stronger bonds tell us the government’s reflation efforts are thus far not working. If concerns about deflation remain more prevalent than concerns about inflation, fixed income assets may offer us an apportunity. With money markets, CDs, and Treasuries paying next to nothing, we may be able to find improved yields in the following:

-

- LQD – Investment Grade Corporate Bonds

- AGG – Investment Grade Bonds – Diversified

- BMT – Insured Municipal Bonds

- PHK – High Yield Bonds

- AWF – Emerging Market Government Bonds

With the economy in a weakened and fragile state, we need to tread carefully in these markets. Some key levels which may improve the odds of success are shown in the charts below. Erring on the side of not taking positions is still prudent. The markets remain in a “prove it to me” mode where we would like to see the markets move through key levels before putting capital at risk.

U.S. Dollar Remains Firm

U.S. Dollar Remains Firm

From a technical perspective, the dollar continues to look strong. Its strength supports the continuation of concerns about deflation, rather than inflation.

Disclosure: Ciovacco Capital Management (CCM) and their clients hold positions in SH, GLD, and PHK. CCM may take long positions in GDX, TBT, LQD, AGG, BMT, and AWF.

Disclosure: Ciovacco Capital Management (CCM) and their clients hold positions in SH, GLD, and PHK. CCM may take long positions in GDX, TBT, LQD, AGG, BMT, and AWF.

=============================================

Catch the New Bull! – Buy Gold Online – Safely, quickly, and at low prices, guaranteed! Bullion Vault.com

=============================================

Nothing in today’s post should be considered as an offer to buy or sell any securities or other investments, it is presented for informational purposes only. As a good investor, consult you Investment Advisor, Do Your Due Diligence, Read All Prospectus/s and related information before you make any investments. – jschulmansr

October. Still, investors can tap into non-financial bonds like

October. Still, investors can tap into non-financial bonds like  assures dollar destruction because the Fed is now on course to print money like never before to quash deflation. We all better hope and prey that the Fed can drain excess bank liquidity very quickly when this credit crisis ends. If not, we’ll have some serious inflation – much worse than what we saw prior to July 2008.

assures dollar destruction because the Fed is now on course to print money like never before to quash deflation. We all better hope and prey that the Fed can drain excess bank liquidity very quickly when this credit crisis ends. If not, we’ll have some serious inflation – much worse than what we saw prior to July 2008.