Tags

agricultural commodities, alternate energy, Austrian school, banking crisis, banks, bear market, Bollinger Bands, bull market, capitalism, central banks, China, Comex, commodities, communism, Copper, Currencies, currency, deflation, depression, diamonds, dollar denominated, dollar denominated investments, economic, economic trends, economy, financial, Forex, futures, futures markets, gold, gold miners, hard assets, heating oil, India, inflation, investments, Keith Fitz-Gerald, market crash, Markets, mining companies, Moving Averages, natural gas, oil, palladium, Peter Schiff, physical gold, platinum, platinum miners, precious metals, price, price manipulation, prices, producers, production, protection, rare earth metals, recession, risk, run on banks, safety, Saudi Arabia, Sean Rakhimov, silver, silver miners, socialism, sovereign, spot, spot price, stagflation, Technical Analysis, timber, U.S. Dollar, volatility, warrants, Water

My Note: The Charts are looking great for Gold and Silver. Included in today’s post, the latest from Peter Schiff on Gold, An overview of the Charts for Gold and Silver. Finally, a very interesting article on Comex and a short squeeze, what could happen? My Disclosure Long Precious Metals and Stocks and more… Get aboard the Gold Train now… Last Call! – jschulmansr

Peter Schiff: Outlook for The Gold Market

By: Peter Schiff of Euro Pacific Capital

The Wall Street Transcript recently interviewed Peter Schiff, President and Chief Global Strategist of Euro Pacific Capital, Inc., on his outlook for the gold market. Key excerpts follow:

TWST: These are somewhat trying times. What has this meant so far for the gold market and where do we go from here?

Mr. Schiff: Gold has actually held up very well compared to other asset classes. If you look at the price of gold relative to its peak, it’s only off about 25%, whereas if you look at stock markets around the world, most are off 50% or more, certainly if you price them in US dollars. If you look at how gold has held up relative to industrial metals, relative to energy, relative to agriculture, gold has done extremely well. I think the fact that it has gone down in dollars has caused a lot of people to assume that gold is not performing in this correction whereas, in fact, it has. Also if you look at gold in terms of other currencies, recently you’ve seen all-time record highs in the price of gold in South African rand, in Australian dollars, in Canadian dollars. So gold has actually had a very strong, stealth move when viewed from the prism of something other than the US dollar.

TWST: Why does everybody key in on the US dollar side of the equation?

Mr. Schiff: Because gold was priced in dollars, it’s traded in dollars and so we all look at it as the dollar price, and the fact that gold has not made a new high in dollars during this economic crisis has led some to believe that maybe it’s lost its luster, it’s not a safe haven. But this rise of the dollar is very suspicious to me, I don’t think it’s justified. But it’s been the unlikely beneficiary of all the problems. You’ve got the problem centered in the US economy; the epicenter of the financial crisis is in America. The reason that the world is in trouble is mainly because of bad loans made to Americans and it’s our economy that I think is a complete facade, a house of cards that has now collapsed, so this dollar rally actually makes no sense.

And especially in light of the monetary policies that we pursued over the course of the last six months, the bailouts, the stimulus, all of the things that are likely to happen with Barack Obama saying that the sky is the limit on budget deficits, we’re going to print money until we run out of trees. Everything that we are doing is so negative for the dollar, yet the dollar has managed to rally. So I think temporarily the fundamentals are on hold, but I think once the dollar really resumes its decline, you’re going to see gold really shine again not only in terms of the dollar. It will continue to do well against other currencies, but it will do particularly well against the dollar.

TWST: Isn’t gold normally the “safe haven” that investors seek?

Mr. Schiff: I think it’s a safe haven. A lot of people are seeking safety right now in the US dollar, but that makes no sense to me. That’s like jumping out of the frying pan into the fire. I think the dollar is a fundamentally flawed currency that is doomed to collapse, and temporarily it’s benefiting from the fact that it’s seen as the alternative to everything else. People are worried about all asset classes, nobody wants to own anything and somehow by default, the dollar is the opposite of owning other things. People are keeping score in terms of dollars and I’d certainly think that some of the most impaired financial institutions are in the United States. I think some of the losses are very heavy here and that has made a lot of American institutions — investment banks, hedge funds, mutual funds —liquidate assets all around the world, many assets in other countries; those institutions require the liquidation of those currencies to repatriate the dollars necessary to meet their margin calls, to fund their redemptions, and so that might also be temporarily propping up the dollar.

TWST: Has the supply/demand situation in gold changed at this point because of the problems with the hedge funds?

Mr. Schiff: Yes, I think that the credit crunch has certainly put the screws on a lot of gold exploration. A lot of the junior miners are basically on the verge of going bankrupt right now. I’m sure a lot of projects are on hold; a lot of exploration is simply not going to get funded. This is simply improving the supply and demand imbalances that have favored gold for some time and other commodities too. Certainly in industrial metals, in the energy complex, a lot of exploration, a lot of development projects have been cancelled or are never going to see the light of day for many, many years because of the credit crunch and because of the fear of falling prices, which I think is unwarranted. But even when prices start to recover, I think there will be a lot of suspicion of the rally. So people are going to be reluctant to commit capital to a market they have no confidence in.

So I think the supply and demand imbalances for commodities are going to continue, and that commodities themselves are still one of the best asset classes around the world to own. As for the commodity producers, it all depends on their balance sheets. Some of them are going to be spectacular buys. Looking at the gold complex, I think one positive development I’ve seen has been the strength of the South African miners, which seem to have bottomed first. They started to decline before the overall sector; when many of the Canadian miners were making new highs, the South African stocks were falling. But it seems like the South Africans have bottomed here. They’ve made significant rallies, some of them have even doubled from their lows and they seem to be stronger. So they topped out first; maybe the fact that they have bottomed first is a positive sign. Maybe they are going to lead on the way up just like they led on the way down.

TWST: How about on the political side of the equation? What’s going to be the position of central banks now relative to gold?

Mr. Schiff: The Bank of Canada just slashed rates down to 1.5%. Central banks all around the world are reducing interest rates. It’s the most inflationary monetary policy globally that we have ever experienced and ever will experience in our lifetime. That’s a very favorable market for gold. When central banks are just putting the pedal to the metal on the printing presses and driving interest rates down to nothing, how can you not own gold? Gold is money, the supply of gold is going to grow very slowly over time, and the supply of all fiat currencies is going to grow rapidly. You’re looking at maybe 10%, 20% per year or more annual increases in money supply in every country in the world, and then they pay you next to nothing for holding it. If you want to take currency that is rapidly being debased and you want to deposit it someplace, you are barely getting interest, so why not own gold instead? Even though gold doesn’t pay interest, at least it’s not being debased.

TWST: What about the central banks selling gold? Are they going to back off now due to the financial crisis?

Mr. Schiff: At some point, the central bank selling is going to turn into buying. Who are these guys kidding? They need to have real reserves behind their currencies. They can’t simply hold the US dollars and say our currency has real value because it’s backed by the dollar. When the dollar is backed by nothing and being rapidly debased and paying no interest — our rates are down to 1% and likely to head lower. What’s the justification for foreign central banks holding dollar deposits rather than gold, when the dollar yields next to nothing? It doesn’t make any sense. So I think central banks are going to become buyers and the central banks that own the most gold are going to have the most influence, the strongest currencies, etc. I think people are going to see that and right now, if you look at the percentage of gold owned by central banks, it’s at the lowest it’s ever been.

TWST: Silver and platinum have come down much more than gold. Is that because of supply/demand or just because of what’s going on in the market?

Mr. Schiff: I think there are more industrial uses for those metals and so more of this whole idea that the global economy is going to collapse and no one is going to buy anything is hurting those metals relative to gold. I think gold is more of a pure monetary metal. Sure there’s some jewelry demand for gold, but it’s not used as much in industry, and I think it’s more of a monetary metal, a safe haven metal and so, because of that function, it is holding on to its value. I think there are a number of individuals around the world who understand the difference between gold and fiat money, and I think a lot of people are worried and want to protect their wealth. There is a minority of investors who see through the smokescreen and are not buying US Treasuries, they are buying gold. At some point, the people who are doing that are going to be the ones who are going to be vindicated as gold prices ultimately make new highs, and I still think that we could hit $2,000 an ounce next year in the price of gold.

ps- Peter Schiff has been very accurate recently!-jschulmansr

============================================

Great Looking Precious Metals Charts

By: Jeff Pierce of Zen Trader

I’ve had mixed results trading gold stocks in the past but those stocks have some of the best looking charts in the market pointing to higher prices very soon. I’m not going to speculate on why they’re rising when you consider how much money has been printed by the US and the inflation/deflation debate, but the fact is, they are rising and have the right price/volume action you want to see for near term price appreciation.

While I am near term cautious on the overall markets, I do have a buy signal on the gold/silver stocks as they have the capability to rise even when the general markets are falling.

While SLV didn’t rebound like the individual stocks in the silver sector did on Friday, it does look poised to move higher after a retest of the higher trendline of the triangle formation below.

============================================

Gold and Precious Metals Likely to Improve in 2009

By: Boris Sobolev of Resource Stock Guide

In this short update we focus on the long term technical picture for gold and precious metals stocks since the fundamentals have not changed and remain bullish. The technical picture, however, is getting very interesting.

Gold price action in the past half a year can best be characterized (especially after the recent rally) as consolidation. Such a consolidation is reasonable after a huge spike last year into early 2008, where gold exploded from $650 to over $1000 per ounce.

The long term monthly chart is encouraging. There is the clearly evident higher lows pattern, the RSI has bottomed and the MACD histogram is starting to curve higher.

Most importantly the 20-month Exponential Moving Average (EMA) is turning up, reversing a first-time-in-eight-years bearish turn downward. It is very important to see gold close above the 20-month EMA two months in a row; this would give further evidence of a bullish reversal.

The bull market in gold will resume in full force after gold penetrates its downtrend line which is currently at around $930.

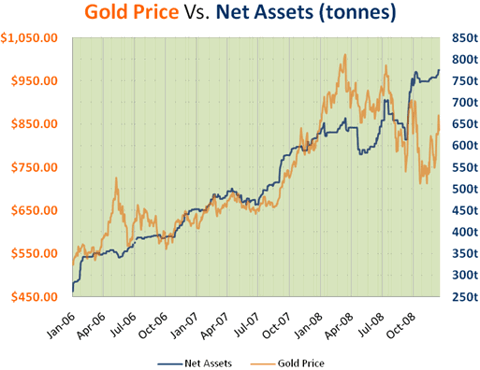

Another bullish factor for gold is the renewed investment demand by the StreetTRACKS Gold Shares (GLD). Gold holdings have now reached an all-time-high of 775 tonnes.

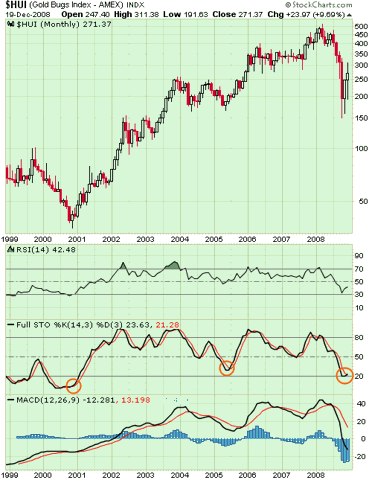

On the monthly charts of a Gold Bugs Index ($HUI), highly significant buy signals have been generated. There have been successively higher lows for three months in a row, the RSI has bottomed and started moving higher, the stochastic indicator reversed from a very low level (a rare signal) and the MACD histogram is starting to curve.

These long term reversals in indicators are highly reliable and rarely fail. There is a good probability that 2009 will turn out to be a complete opposite of the brutal 2008 for the precious metal stocks.

As stated several times before, we are starting to accumulate precious metals stocks having low exposure to base metals, with high gold and silver grade deposits, healthy balance sheets and prospects for internal growth.

===============================================

Will Comex Default on Gold and Silver?

By: Avery Goodman

Gold and silver were once the most stable of all goods. Extreme volatility, however, is now a part of their nature. It comes from being made a part of the commodities casino, known as the American futures market, where speculators are allowed to use margin to control 14 times as much metal as they actually have money to buy. When the price drops a little, the “stop loss” orders of these leveraged players are triggered, and that amplifies the price move such that the price collapses on the futures market. Similarly, when gold fever begins, the prices can shoot into the sky, as the leveraged longs begin buying again. That is why the price for futures based gold and silver is still very low compared to March, 2008, even though the real world investment demand for both metals is higher than it was, back then (higher than ever before in history, actually), mining supply for gold is down by 5%, and the mine based supply of silver has utterly collapsed.

It should be noted that precious metal volatility is a short and sometimes medium term phenomenon. Since 1913, when the Federal Reserve was created, the dollar has depreciated by 97% against gold. The dollar has depreciated by about 90% against silver in that same 95 year time period. Gold has also appreciated tremendously in price as compared to 8 years ago, 2.5 times against the Euro and 3 times against the dollar. Rational people, therefore, cannot deny that, using a multi-year or, even more, a century long point of view, gold and silver are the best stores of wealth. When looking at long term family legacies, therefore, a large position in gold and silver should be a part of every estate plan. That is especially true now, given that demand currently substantially exceeds supply, the imbalance has every likelihood of becoming more severe in the near future, and the “futures” exchange prices are now very low compared to the real market.

In the last decade, central banks selling and leasing made up the long time shortfall between supply and demand. But, given the financial crisis, and the fear that the U.S. dollar will eventually collapse, central banks no longer want to hold all their exchange reserves in U.S. dollar cash, U.S. dollar denominated bonds and other investments. They are also unwilling to hold everything in other paper currencies, like the Euro. Some governments, including those in Europe and the USA, still have large gold hoards. But, China wants to buy 3,600 tons of additional gold for its reserves. The only way that this demand can be fulfilling without exploding the price is through a “privately negotiated” off-market sale of IMF gold. European banks don’t want to continue selling what gold hoards they still have left, after 20 to 30 years of participation of selling and leasing gold.

In the case of silver, almost all government stockpiles are now gone. The only ones left are in Russia and China, and China restricted the export of silver last year. The U.S.A., for example, has already expended every last ounce of its strategic silver reserves years ago. The U.K. and all other western nations exhausted their supplies even before the U.S.A. Newly mined supplies have never been sufficient, and demand continues to increase. The imbalance between supply and demand is becoming especially severe, and, in the case of silver, is going to increasingly be a difficult industrial use issue in the next few years.

Because of the severe shortages, retail dealers are charging hefty premiums for both gold and silver. This is dissuading many people from buying, but it shouldn’t, because there are ways to buy the metals without paying any premium at all. Gold and silver are selling cheaply, without premiums, on the American futures markets. Most futures contracts allow buyers to demand delivery of the metal, so the futures market is an excellent way to obtain comparatively cheap precious metals. This has already been noticed by astute investors. In the past, most traders used futures markets solely for purposes of speculation. Normally, delivery demands average less than 1% each month. Now, however, because of the premiums available in the real market, buying a futures contract and demanding physical delivery upon maturity has become a cheap method of obtaining substantial quantities of physical gold and silver. With respect to the December contract, for example, exchange records show that more than 5% of people holding open standard sized (100 ounce) gold futures contracts, and about 10% holding open silver futures contracts (5,000 ounce) demanded delivery. The delivery demands are happening even more often among deliverable mini-contracts (33.2 ounce gold/1,000 ounce silver) purchased on the NYSE-Liffe exchange.

Some speculate that clearing members of the exchanges, who have sold gold and silver short on the futures market, will eventually be bankrupted by these delivery demands. According to these skeptics, the gold and silver consists mostly of fake claims to vaulted supplies that do not exist. They say that futures contracts are nothing more than “fake paper gold” and most refuse to buy on the futures markets, opting, instead, to pay huge premiums at retail gold and silver dealers. The skeptics may be right about the failure to keep adequate supplies of vaulted metal, but it doesn’t really matter. If you buy gold and silver on the futures exchanges, you will get your metal, whether or not the short sellers are trying to defraud you, and I’ll now explain why.

The Commodities Futures Trading Commission is charged with the responsibility to monitor and regulate American futures markets. In spite of this, the futures markets have morphed from a legitimate place to hedge the risk of commodities, into a worldwide casino, which has a gaming commission that claims all of games of chance are really “investing”. This is nonsense. The exchanges are mostly used as gambling halls, with banks as casino operators, and speculators serving in the role of casino guests. All types of bets, from taking odds on interest rates to taking odds on the volatility of the stock markets (with no underlying security except the VIX!) are allowed, and are available to anyone who enjoys games of chance. If the CFTC ever bothered to enforce its own enabling act, and associated regulations, most of these games of chance would be quickly closed. For example, CFTC regulations require 90% of all deliverable commodity contracts (including gold and silver) to be covered by stockpiles of the real commodity, and/or real forward contracts from real producers (like miners). In practice, however, CFTC has never done a spot audit of even one vault. We really have no idea whether or not short sellers really have the gold or silver that they claim to have. We can assume that they probably don’t, given that the number of futures contracts issued has often exceeded the entire known supply of silver, for example, in the entire world.

Indeed, in spite of rampant speculation as to their identity, in truth, we don’t even know who the short sellers are. Other countries, like Japan, have full disclosure of identities and positioning, in open and transparent futures markets, but this is not true of the much larger futures markets based in America. American futures markets are mostly opaque, because the CFTC keeps the information secret. Lack of transparency always is a recipe for fraud and corruption. The likelihood of widespread violations, occurring at exchanges regulated by CFTC, is very high. Logical people, therefore, can make some reasonable assumptions. It is quite likely that the sellers on COMEX do not have 90% of their silver contracts, for example, backed by stockpiles of the metal.

Yet, adherence to Federal regulation is an implicit provision in the terms and conditions of every futures contract. If COMEX and/or NYSE-Liffe short sellers are entering into naked short contracts, they are violating market rules, falsely presenting their contracts to the public, and doing all this with a premeditated intent to defraud buyers. Knowingly making false assertions and promises is fraud in the inducement. Violation of the market rules is also “fraud upon the market”, and a federal and state felony level crime that can result in a long jail sentence. The vast majority of short positions in gold and silver appear to be held by only 2 – 3 American banks, so, it would be extraordinarily easy to pinpoint the perpetrators. Potentially, they could be prosecuted for market manipulation, common law fraud, state and federal RICO actions, as well as other counts.

In other words, a large scale default on COMEX or NYSE-Liffe would not only trigger the paying of money damages, but would also involve criminal liability. Even if a few individuals within the federal government are complicit, as has been alleged, and the U.S. Justice Department refused to prosecute, there are enough politically ambitious state prosecutors to take up the baton. Futures market short sellers would pay a heavy price if there were ever a big default. Because of this, they will spend whatever money is needed to make sure it never happens.

If a clearing member of an exchange fails to deliver, the futures exchanges are legally liable on the debt. If a clearing member goes bankrupt, performance becomes the obligation of the exchange. If a short position holder cannot or does not deliver, the exchange must either deliver, or pay in an amount equal to the difference between the contract price, and the amount of money needed to buy the physical commodity in the open market. Generally speaking, contract holders are allowed to purchase silver or gold on the spot market in a reasonably prompt manner, and all costs of doing so must be reimbursed.

Contrary to the claims of some sincere but misguided metal aficionados, while gold and silver may be occasionally in so called “backwardation”, both are readily available at the right price. That price, of course, may be considerably higher than the reported prices on futures markets. Precious metal will continue to be available so long as the price is “right”. If short sellers on COMEX are really as naked as some claim, the only result of technical “default” at the COMEX will be a huge “short squeeze”, sending precious metals prices to the roof. During this squeeze, movement of the U.S. dollar, up or down, will be irrelevant. If delivery demands exceed supplies in futures market warehouses, metal will be purchased on the spot market. Short sellers or the exchange will be forced to make good on whatever price is paid.

Here’s how it would work. Let’s say you buy a futures contract for February delivery of 100 ounces of gold at $800 per ounce in December. In February, spot gold is selling for $1,000 per ounce, and you deposit the full cash cost of your futures contract into your account, instructing your broker to issue a demand for delivery. The counterparty can’t deliver because the COMEX warehouse runs out of “registered” metal. There is a huge short squeeze as short sellers run around the world physical market, trying to buy gold. The short seller misses the last day to deliver. Because everyone starts hearing about the missed deliveries, by the next day after the last possible delivery date, spot gold in London starts selling for $1,359 per ounce. Your commodities broker must take the money you deposited and buy the commodity on the spot market for $1,359. The broker will be reimbursed by the short seller and/or the exchange in the amount of $55,900, plus any expenses you incurred in buying physical gold on the spot market. In the end, you get your gold or silver at the price you paid for the futures contract, regardless of the default.

A number of well intentioned, but misinformed, precious metal commentators have claimed that exchanges will escape from this obligation by a declaring a co-called “force majeure” event. Force majeure is a legal doctrine which says that compliance with a contract is excused if an “act of God” makes it impossible to comply. Formal force majeure provisions exist in many NYMEX contracts, including gas and oil contracts, for example. After recent hurricanes in Louisiana, a NYMEX committee declared force majeure, and an extension of time for delivery of natural gas pursuant to the contracts. Unlike gas, however, which is produced from the ground, or must be moved long distances under sometimes difficult conditions, gold and silver are commodities that normally reside in vaults, and are easily transported. It should be noted that, as of this date, no formal written force majeure provision exists in the specifications of COMEX gold and silver contracts. Admittedly, force majeure is a legal doctrine that is implied in every contract, and need not be written down. However, higher gold prices and/or failure to comply with the 90% cover rule are not acts of God and will not excuse contract performance.

Let’s say, as some claim, that short sellers have enmeshed themselves in a web of fake contracts, wherein third parties are contracted to deliver metal to them, even though both the short sellers and the third parties know that these contracts are fake, and there really is no metal to deliver. This web of lies assumedly is designed to protect against claims that they are selling “naked” shorts. The existence of such contracts doesn’t matter to the concept of force majeure. The obligation to deliver cannot be changed by a mere failure of “third” parties to deliver. Failure of contracts owed to short sellers are not acts of God. Failure of third parties to honor their contracts does not excuse performance of the short seller’s obligation to deliver to the final contract holder. It certainly does not alter the obligation of the exchange to guarantee delivery.

Some are still skeptical. What if the entire COMEX and NYSE-Liffe exchanges fail? I doubt that will happen. First, let me say that I do not agree with bailouts. Companies, whether in the financial district or in Detroit, should fend for themselves. No one should be allowed to become parasites who feed on the taxpayers, as the big banks and automakers have now become. If companies make mistakes, behaving in an inefficient and/or outright stupid manner, they and their executives should pay the price. The process of creative destruction is essential to prosperity in a capitalist system. Bad actors and inefficient operators should be swept away to make room for innovation and steadier hands. But, my views are not shared by the U.S. government or most other governments around the world. A large number of the clearing members of both COMEX and NYSE-Liffe have already been bailed out by their respective governments. Huge institutions like JP Morgan (JPM), Citigroup (C), Morgan Stanley (MS), Merrill Lynch (MER), Goldman Sachs (GS), Bank of America (BAC), UBS and Credit Suisse (CS) are considered “too big to fail.”

Can you imagine the exchanges not being too big to fail, when their individual members are? What chance do you think there is of the Federal Reserve allowing the entire COMEX or NYSE-Liffe exchange going bankrupt? In my opinion, the chance is close to zero. A massive failure to deliver is highly unlikely, but, if it did happen, and if the exchanges were unable to comply with their legally binding guarantee, the government will step in and provide gold from Fort Knox and enough money to buy silver in the open market, no matter what the price. The end result will merely be a huge price increase, and an end to the assumed legitimacy of futures market prices, not a default.

Summing things up, if you want to buy gold and silver, but don’t want to pay high premiums, buy them on futures exchanges. First, open a futures account with a commodities broker. Make sure it is a real commodities broker and not an imitation. Stock brokers, like Interactive Brokers, ThinkorSwim, MBTrading, and a number of others claim to be “futures brokers.” In truth, they are not. They can only offer you speculation, and not hedging services. They will not deliver, and will forcibly sell you out of your positions, even at great loss to you, if it comes too close to the delivery date. So, instead, make certain that you open your account with a real commodities broker, like RJOFutures.com, PFGBest, lind-waldock.com, MF Global, e-futures.com or any other broker willing to arrange deliveries. You can speculate just as easily, using a commodities broker, as you can using a stock broker that dabbles in futures. But, if you want delivery, you must have a real commodities broker. Steer clear of stock brokers unless you want to buy stocks.

Middle class families, looking for safety in precious metals, but who don’t have enough money to buy 100 ounce contracts, can buy deliverable mini-gold and mini-silver contracts on the NYSE-Liffe futures exchange. The mini-contracts require delivery of as little as 33.2 ounces of gold and 1,000 ounces of silver. If you want delivery, however, make sure you do not buy COMEX based miNY gold and/or miNY silver contracts. These COMEX mini-contracts are cash settled. The standard contracts, however, on both the COMEX and the NYSE-Liffe (consisting of 100 ounces of gold and 5,000 ounces of silver) are all deliverable.

The highly leveraged nature of gold and silver futures contracts create high levels of volatility. That should be kept in mind when you decide to put a large portion of your investment assets into precious metal. Big price rises and deep dips are commonplace. Most of these market movements occur without much regard for the forces of supply and demand in the real world market. If you need the money tomorrow, steer clear. But, if you want to preserve your family legacy with something that will take you safely through depressions and hyperinflations, over years and decades, gold and silver are good choices.

If you demand delivery and just put your bars in a safe place, you don’t need to worry about the volatility. The price is sure to rise in the longer term because of the fundamentals. Remember, as you watch the dizzying roller coaster of so-called “official spot” prices, that you are buying for the long term and/or for emergency use. Day to day price fluctuations should be ignored.

By way of disclosure, I hold interests in GLD, IAU and SLV as well as

physical gold.

================================================

Final Note: The more buyers who take delivery on their Gold or Silver contracts, the greater the chance of a “short squeeze”- jschulmansr