Tags

2008 Election, agricultural commodities, alternate energy, Austrian school, banking crisis, banks, Barack Dunham, Barack Hussein Obama, Barack Obama, Barry Dunham, Barry Soetoro, bear market, Bollinger Bands, bull market, capitalism, central banks, Chicago Tribune, China, Columbia University, Comex, commodities, communism, Copper, Currencies, currency, Currency and Currencies, D.c. press club, deflation, depression, diamonds, dollar denominated, dollar denominated investments, economic, economic trends, economy, Electoral College, Electors, Finance, financial, Forex, fraud, Free Speech, futures, futures markets, gold, gold miners, hard assets, Harvard Law School, hawaii, heating oil, id theft, India, Indonesia, Indonesian Citizenship, inflation, Investing, investments, Joe Biden, John McCain, Keith Fitz-Gerald, Latest News, legal documents, market crash, Markets, mining companies, Moving Averages, name change, natural born citizen, natural gas, Oath of Allegiance of the President of the United State, Occidental College, oil, palladium, Peter Schiff, Phillip Berg, physical gold, platinum, platinum miners, Politics, poser, precious metals, Presidential Election, price, price manipulation, prices, producers, production, protection, rare earth metals, recession, risk, run on banks, safety, Sarah Palin, Saudi Arabia, Sean Rakhimov, silver, silver miners, socialism, sovereign, spot, spot price, stagflation, Stocks, Technical Analysis, timber, Today, treason, u.s. constitution, U.S. Dollar, Uncategorized, volatility, voter fraud, warrants, Water, we the people foundation

By Luke Burgess of Gold World

Jesse Lauriston Livermore is perhaps the most famous stock trader of the early 20th century.

Famous for amassing and subsequently losing several multi-million dollar fortunes, Livermore also shorted the stock market heavily during the crashes of 1907 and 1929.

Livermore, who was also known as the Boy Plunger, is famed for making—and losing—several multi-million dollar fortunes and short selling during the stock market crashes in 1907 and 1929.

One of Livermore’s core trading rules was…

Be Right and Sit Tight

It’s simple…

Invest in a growing trend and have the courage to hold long-term for really big gains.

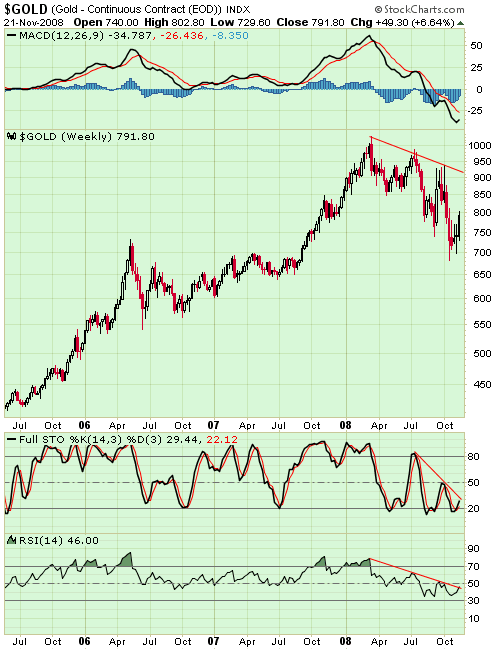

Clearly, the gold bull market is one such growing trend. And investors who “sit tight” will undoutbly see big gains by owning the precious metal now.

Buy Gold Now

The bull market has already pushed gold prices over 300% higher since 2001. And now with the world’s demand for gold is starting to significantly outpace supplies, even higher prices are on the horizon.

During the third-quarter there was a colossal 10.5 million ounce deficit (worth $8.5 billion) in world’s supply and demand of gold. World gold demand increased over 50% since the second-quarter while supplies dropped 64% year-on-year.

Gold demand, particularly in the investment sector, is currently at all-time highs. But estimates suggest that the world will only produce 76.8 million troy ounces during 2008. This represents a 9% decline in world gold production since 2001.

Gold Mine Supplies to Continue Falling

The world financial meltdown has forced the shut down of hundreds of gold mines around the world and slashed exploration and development budgets across the board. And the near-term future of new investment still looks pretty grim.

The effects of these budget cutbacks won’t be felt in the gold market for several months to years. But the lack of investment money going into gold mines right now-and probably for over the next several months-will certainly have an effect on global gold supplies in the future.

And the lack of these supplies will positively affect gold prices.

The global economic crisis has motivated miners of all metals to cut back on exploration and development activities. Below is a just partial list of mine closures and delays that have been announced over the past several weeks:

| August 21 HudBay Minerals [TSX: HBM] closes its Balmat zinc mine and concentrator. October 13 October 20 October 20 October 21 October 21 November 6 November 10 November 10 November 10 November 11 November 11 November 13 November 13 November 14 November 17 November 18 November 18 November 19 November 20 November 21 Novmeber 21 November 24 November 26 December 1 December 3 December 8 |

With demand soaring and supplies plummeting, there’s never been a better time to own gold. Gold prices could go to as high as $5,000 once this gold bull market plays out.

Be right and sit tight.

Buy gold.

Good Investing,

Luke Burgess

Managing Editor, Gold World

P.S. It’s simple, really. Demand is soaring. Supplies are plummeting. And if you don’t buy gold now, you may not get the chance to later.

==============================================

Troubling Questions For Obama Team

By: Linda Chavez of GOPUSA

A corruption scandal in President-elect Obama’s backyard is the last thing this country needs. But like it or not, that’s exactly what we have in the unfolding drama of Illinois Gov. Rod Blagojevich’s arrest earlier this week for trying to sell Barack Obama’s Senate seat. The federal prosecutor in the case — Patrick Fitzgerald, the man whose investigation of the Valerie Plame leak case nearly paralyzed the Bush White House for a time — has made it clear that nothing ties Obama directly to the Blagojevich scheme. But the timing of Fitzgerald’s announcement raises some serious questions.

Apparently, Fitzgerald knew that Blagojevich was trolling for bidders for the Obama seat in the waning days of the general election. Before the first votes were counted to elect Obama president, Blagojevich was so confident in Obama’s victory he was already soliciting bids for the seat. And Fitzgerald already had substantial evidence that Blagojevich was engaged in major corruption before the governor put a “for sale” sign on the Senate seat. So why didn’t the federal prosecutor act prior to the election? Had he done so, of course, it could have damaged Obama.

Many would argue that bringing down another Illinois Democrat before the election would have smelled like a dirty trick. The federal prosecutor, after all, was a Republican appointee, and the McCain campaign had already run ads trying to tie Obama to political corruption in Chicago. One of Obama’s early financial supporters, land developer Tony Rezko, was convicted on corruption charges earlier this year, and Rezko figures prominently in the Blagojevich scandal. Had Blagojevich been forced to do a perp walk before Election Day, voters might have asked why Obama had endorsed Blagojevich just two years earlier, considering the governor was at that time under investigation for taking bribes. The endorsement would have been yet another example of Obama’s bad judgment in his associations from Rezko to the Rev. Wright to Bill Ayers.

But even if Fitzgerald acted fairly and prudently by not moving against Blagojevich in the heat of a political campaign, why did he decide to act this week? His explanation was that he was trying to stop “a political corruption crime spree.” Under existing Illinois law, the governor has final authority to appoint someone to fill a vacant U.S. Senate seat and wiretaps suggest Blagojevich was about to do just that. According to the criminal complaint, Blagojevich had found at least one bidder — identified only as Senate Candidate 5 — who offered to raise the governor $500,000 and another $1 million if he got the appointment. Perhaps Fitzgerald simply wanted to go public before Blagojevich sealed the deal.

But there are other possible explanations. Fitzgerald’s hand may have been forced by the Chicago Tribune, which reported Dec. 5 that Blagojevich’s phone lines were being tapped. This information signaled everyone — the governor and anyone talking to the governor or his aides — that they could become ensnared in a huge criminal investigation leading to indictments.

President-elect Obama has emphatically denied that he ever talked to Blagojevich about his Senate replacement. And certainly Fitzgerald has done everything he can to confirm that Obama is not implicated in any way. But there are a number of unanswered questions about what contact members of the president-elect’s team might have had with the governor or his aides, directly or through intermediaries. A number of aides, including the incoming White House Chief of Staff, Rahm Emmanuel, and former campaign leader David Axelrod, have long-standing ties to Blagojevich. And Axelrod has already had to revise his earlier assertion that Obama had spoken with Blagojevich about candidates to replace him in the Senate.

The president-elect has said “I want to gather all the facts about any staff contact that may have taken place. We’ll have those in the next few days and we’ll present them.”

The president-elect’s credibility is on the line. For the good of the country, we must all hope this scandal doesn’t infect anyone in the new administration. The best way to ensure that is for the president-elect and his aides to be forthcoming quickly.

—

Linda Chavez is the author of “An Unlikely Conservative: The Transformation of an Ex-Liberal.”

COPYRIGHT 2008 CREATORS SYNDICATE, INC.

============================================

By: Michael Barone of US News And World Report

I have not seen it recorded whether John F. Kennedy, after he was elected president in 1960, held conversations with Massachusetts Gov. Foster Furcolo as to who would be appointed to fill his seat in the Senate. History does record that Furcolo, just nine days before turning the governorship over to the Republican elected to succeed him, appointed one Benjamin A. Smith II, a college roommate of Kennedy’s and former mayor of Gloucester, who chose not to seek the seat in the next election in 1962, which happened to be the year in which Edward Kennedy turned 30 and was therefore old enough to run for it.

Memory tells me that there was little fuss made of this at the time. Ambassador Joseph P. Kennedy obviously wanted someone appointed to keep the seat warm for Teddy, and so it was done. And Edward Kennedy has turned out to be an able and accomplished senator.

That was a different tableau from the one we have seen unfold in Chicago this past week. Furcolo was an intelligent man, disappointed to have failed to win the state’s other Senate seat and destined not to win elective office again. But he knew that it would not pay to buck the Kennedys.

Rod Blagojevich, the governor who under Illinois statute has the power to appoint a senator to fill out the remaining two years of Barack Obama’s Senate term, is made of different stuff. He was arrested last Tuesday, and the U.S. attorney filed a criminal complaint and made public tapes of Blagojevich seeking personal favors in return for the Senate seat.

Obama denied having conversations with Blagojevich about his choice, though his political strategist David Axelrod said last month that Obama had. Obama declined further comment when asked whether his staff members had discussed the matter with the governor, but he then promised to reveal the details later.

In the ordinary course of things, there would be nothing wrong with such conversations (did Foster Furcolo decide on Benjamin A. Smith II without prompting?). And the construction of the evidence most negative to Obama one can currently make is that someone in Team Obama suggested nominating Obama insider Valerie Jarrett, Blagojevich simply refused or asked for something improper in return and Team Obama promptly broke off communications. Any impropriety in this version was on Blagojevich’s part, not on Obama’s.

Still, these are not headlines the Obama transition team wants. So far, the president-elect has won wide approval for his performance since the election, with poll numbers significantly higher than George W. Bush or Bill Clinton got in their transition periods. His leading foreign, defense and economic appointments have won high praise from all sides, in some cases more from conservatives than liberals. And in a time of financial crisis and foreign threats, he has seemed to keep a clear head and a steady hand.

He has appeared to avoid all but small mistakes, and his theme of unifying the nation — muted perhaps necessarily in the adversary environment of the campaign — has come forth loud and clear.

From all this the Blagojevich scandal is an unwanted distraction. It is a reminder that, for all his inspirational talk of hope and change, Obama, like Blagojevich, are both products of Chicago Democratic politics, which is capable of producing leaders both sublime and sordid.

Obama has not always avoided the latter. For 20 years he attended the church of the Rev. Jeremiah Wright, now thrown under the bus, and for more than a decade engaged in mutually beneficial exchanges political and financial with the political fixer Tony Rezko, now in federal custody.

Blagojevich, never a close political ally, has now been thrown under the bus, too, and seems likely to share Rezko’s fate. Obama fans can point out, truthfully, that other revered presidents had seamy associates and made common cause on their way up with men who turned out to be scoundrels. Franklin Roosevelt happily did business with Chicago Mayor Ed Kelly, though warned that he was skimming off money from federal contracts. John Kennedy no more thought to deny a request from the Mayor Daley of his day than Obama has thought to buck the Mayor Daley of his.

But as Kennedy supposedly said of a redolent Massachusetts politician, “Sometimes party loyalty asks too much.” The man in question was the Democratic nominee for governor and was not elected. Until Patrick Fitzgerald released his tapes, Barack Obama never said the same of Rod Blagojevich.

Obama has profited greatly from his careful climb through Chicago politics. But there is an old saying that in politics nothing is free — there is just some question about when you pay the price. Obama is paying it now.

To read more political analysis by Michael Barone, visit http://www.usnews.com/baroneblog

COPYRIGHT 2008 U.S. NEWS AND WORLD REPORT

DISTRIBUTED BY CREATORS SYNDICATE INC.

")

")