As I write there is selling pressure or maybe price manipulation on the gold market right now. Are we going to let them do this? Especially with everything else in the markets i.e. the dollar, banks, stock markets in chaos and dissarray? The best way to fight back is to keep buying gold especially on Comex and taking delivery. That would catch them and for once the little guy wins! The Gold price is holding steady at $990 oz after being tested early this morning, Gold bounced right off the $975 – $977 support and is now holding steady. Today’s articles do talk about the manipulation going on in the Gold and Silver markets. To date the largest short positions and majority of the short interest on Comex consists of a few banks who went short in the $750 to $950 range ( I know a large spread but they have been cost averaging their positions). If all the longs would start taking possesion of their gold and silver off of Comex, I am telling you this, we would have one of the largest “Short Squeezes” in history! – Good Investing! -jschulmansr

=======================================

“Nothing will unnerve the paper gold shorts more quickly and do more to undercut their confidence than to strip them of the real metal and force them to come up with more hard gold bullion to make good on deliveries. “Stand and Deliver or Go Home” should be the rallying cry of the gold longs to the paper gold shorts.” –Trader Dan Norcini

=======================================

This is an older article which explains the manipulations which have been going on. The same banks still hold teir positions of as last published Comex reports.– jschulmansr

Chris Powell: Gold and Silver Market Manipulation Update – Gold Anti Trust Action Committe GATA

Submitted by cpowell on Fri, 2008-11-14 20:51. Section: Essays

Good afternoon and thank you for being here. It’s an honor to get to speak with so many interested in silver, especially at such an interesting time in history. I’m going to ramble a bit, and try not to get too detailed and save some time for questions where you can get specific.

Remarks by Chris Powell, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

New Orleans Investment Conference

New Orleans Marriott Hotel

Thursday, November 13, 2008

Why are the gold and silver markets manipulated by governments and the financial houses that serve as their agents? Because gold and silver are competitive currencies and because their value greatly influences interest rates, which ordinarily governments like to keep low.

Last year at this conference I reviewed in detail the official documentations and admissions of the gold price suppression scheme. Those documentations and admissions remain posted at GATA’s Internet site:

Maybe most interesting have been the studies of the U.S. Commodity Futures Trading Commission market reports done by silver market analyst Ted Butler and by Gene Arensberg, a market analyst for ResourceInvestor.com. Butler and Arensberg reported that as of August just two banks held more than 60 percent of the short positions in silver on the New York Commodities Exchange. This was an unprecedented and seemingly illegal concentrated short position, and it implied that the smashing down of silver was very much a manipulation by one or two very rich and powerful market participants, a destruction of the free market. Complaints about this concentrated short position prompted the CFTC to undertake still another investigation of the silver market, this time by a different division of the commission, its enforcement division. Further, CFTC Commissioner Bart Chilton has told GATA that the agency is investigating the gold market as well.

This week Arensberg found that the CFTC’s latest report shows that just three or fewer banks now hold half the short positions in gold on the Comex and more than 80 percent of the silver short positions.

Also this week Butler obtained a copy of a letter from the CFTC to U.S. Rep. Gary G. Miller, R-California, that sought to explain the concentrated short position in silver. The CFTC’s letter implied that this extreme short position resulted from JPMorganChase’s acquisition of Bear Stearns in March. If we construe the CFTC’s letter correctly, that would make MorganChase the big short in silver now and imply that, in financially underwriting MorganChase’s acquisition of Bear Stearns, the Federal Reserve was also underwriting MorganChase’s assumption of that short position in silver.

Of course MorganChase was also the bullion banker to Barrick Gold, the biggest gold shorter over the last decade. In 2003 Barrick told U.S. District Court Judge Helen Berrigan right here in New Orleans that, in shorting gold, Barrick had become the agent of the central banks in regulating the gold market and thus should share their sovereign immunity against lawsuits.

MorganChase is also the world’s biggest issuer of interest-rate derivatives, instruments by which interest rates are suppressed.

All this causes GATA to believe that MorganChase is in effect an agency of the U.S. government, or rather, perhaps, that the U.S. government is an agency of MorganChase. In any case, MorganChase has had an intimate relationship with the U.S. government since the days of J. Pierpont Morgan himself.

Incidentally, Jean Strouse’s 1999 biography of Morgan, which won the Bancroft Prize for American History and Diplomacy, recounts that Morgan’s first big triumph in finance was to corner the gold market in New York in 1863 during the Civil War. Nearly 150 years later there really may be nothing new under the sun.

Also lately raising suspicion about surreptitious government intervention in the precious metals markets has been the refusal of the Federal Reserve and the Treasury Department to release to GATA hundreds of pages of government documents about the disposition of the U.S. gold reserve. The Fed has told GATA’s lawyers that the documents are being withheld in part because their release might compromise information that is proprietary to private companies. Why anything about the U.S. gold reserve should be considered proprietary to anyone is beyond those of us at GATA — unless, of course, the reserve is being used to manipulate markets surreptitiously.

But we at GATA do not feel picked on by the Fed and the Treasury. For the Fed and the Treasury seem to be treating everybody as if the disposition of public assets is nobody’s business but Wall Street’s. This week Bloomberg News Service reported that the Federal Reserve is refusing to disclose how much it has lent to particular banks and exactly what sort of collateral the Fed has accepted for those loans, which have reached hundreds of billions of dollars. For example, is the Fed valuing the same kind of collateral from different borrowers the same way, and lending against it at the same rate? Or is the Fed giving advantages to certain borrowers and not others, depending on their political influence and straitened circumstances? That is, are the Fed and the Treasury Department now being operated as the greatest patronage and market-rigging schemes in history? The government is concealing the evidence.

Since we last gathered here in New Orleans many of us been cowering under the prospect of more official-sector gold sales, particularly gold sales by the International Monetary Fund, which has approved a plan of selling gold to raise cash to replace the income it is no longer getting from interest on loans to developing countries. But despite more than a year of loud talk about it, the IMF has not sold any gold yet, and GATA suspects that the IMF really does not have the 3,200 tonnes it says it has, only a tenuous claim on the gold reserves of its member nations, particularly the United States, which has a veto on any IMF gold sales and has not approved any yet.

Back in April I tried to engage the IMF in a dialogue about its gold and I had an exchange by e-mail with an IMF publicist, Conny Lotze.

My first question was: “Your Internet site says the IMF holds 3,217 metric tons of gold ‘at designated depositories.’ Which depositories are these?”

Conny Lotze of the IMF replied, but not specifically. She wrote: “The fund’s gold is distributed across a number of official depositories,” adding that the IMF’s rules designate the United States, Britain, France, and India as depositories.

My second question was: “If you’d prefer not to identify the depositories for security reasons, could you at least identify the national and private custodians of the IMF’s gold and the amounts of IMF gold held by each?”

Conny Lotze replied, again incompletely: “All of the designated depositories are official.”

My third question was: “Is the IMF’s gold at these depositories allocated — that is, specifically identified as belonging to the IMF — or is it merged with other gold in storage at these depositories?”

Conny Lotze replied, still not very specifically: “The fund’s gold is properly accounted for at all its depositories.”

My fourth question was: “Do the IMF’s member countries count the IMF’s gold as part of their own national reserves, or do they count and identify the IMF’s gold separately?”

Conny Lotze replied a bit ambiguously: “Members do not include IMF gold within their reserves because it is an asset of the IMF. Members include their reserve position in the fund [the IMF] in their international reserves.”

This sounded to me as if the IMF members are still counting as their own the gold that supposedly belongs to the IMF — that the IMF members are just listing the gold assets in another column on their own books.

My fifth question was: “Does the IMF have assurances from the depositories that its gold is not leased or swapped or otherwise encumbered? If so, what are these assurances?”

Conny Lotze replied: “Under the fund’s Articles of Agreement it is not authorized to engage in these transactions in gold.”

But I had not asked if the IMF itself was swapping or leasing gold. I had asked whether the custodians of the IMF’s gold were swapping or leasing it.

This prompted me to raise one more question for Conny Lotze. I wrote her: “Is there any audit of the IMF’s gold that is available to the public? I ask because, if the amount of IMF gold held by each depository nation is not public information, there doesn’t seem to be much documentation for the IMF’s gold, nor any documentation for the assurance that its custody is just fine. Without any details or documentation, the IMF’s answer seems to be simply that it should be trusted — that it has the gold it says it has, somewhere.”

And Conny Lotze … well, she never wrote back to me again. After all, I had uttered the dirtiest word in government service: A-U-D-I-T.

That the International Monetary Fund refuses to account for the gold it claims to have should be potential news for the financial media. It would be nice if the financial media pursued that issue before their next attempt to scare the gold market with stories about IMF gold sales.

But even if such sales by the IMF should be undertaken, they might not be much for gold investors to worry about. For a month ago I happened to attend in New York City the annual fall dinner of the Committee for Monetary Research and Education, and it had an unscheduled speaker, Columbia University Professor Robert Mundell, who, as you may recall, won the Nobel Prize in economics in 1999 and is regarded as the father of the euro. Through great luck I got to sit next to Mundell on the platform and so heard him clearly as he went out of his way to join the discussion of my topic, gold. Mundell remarked that if the IMF sold any gold, China should buy all of it to diversify its foreign exchange reserves. Since Mundell is a consultant to the Chinese government, the Chinese government surely heard this advice from him long before the CMRE meeting did.

You can do a lot of market rigging when you can print legal tender to infinity, pass out huge amounts of it to your friends, and induce them to use derivatives to siphon speculative demand for real stuff away from actual possession of that real stuff. But in the end printing legal tender and contriving promises to deliver real stuff don’t produce real stuff. With infinite legal tender and derivatives you can push the futures price of a commodity below its production costs and below its free-market price for a while, but you risk causing shortages. And of course that’s what we have in gold and silver right now — falling prices for the paper promises of metal even as little real metal is to be had and the spread between the futures price and the real price grows. Last night a GATA supporter in Bangkok, Thailand, who long has been in the silver business e-mailed me that real silver there is priced at $18 per ounce for orders of 1 kilo or more and $23 per ounce for smaller orders. Our friend in Bangkok added that when he shows silver dealers there the New York silver futures price on the Internet, they laugh at him. Shortages can have various causes but generally they are their own cure. When shortages persist, they well may result from government intervention in markets.

Of course prices always have been determined to a great extent by the volume and velocity of money and credit, and so the creation of money and credit is, all by itself, inevitably an intervention into markets. But lately money and credit have been disappearing and reappearing in a flash in the billions and trillions. How can so much come and go so quickly? Maybe because what passes for money and credit today is a bit too ephemeral, having little connection to reality and a lot of connection to politics.

That is why market advice today is more doubtful than ever: Markets have become more politicized than ever. Supply and demand and profitability are no longer the primary determinants of markets. No, the primary determinant of markets is now politics: Which countries will cut interest rates the most? Which countries will subsidize their banks and corporations the most? Which countries will get IMF and World Bank loans? Which countries will be given unlimited currency swap lines and which won’t? Which companies will get bailed out and which won’t? How much more dishoarding of gold will central banks do to keep the price down, and which central banks? When will central banks run out of gold or decide to stop spending it this way? Most importantly, when will the world decide to stop financing the wild irresponsibility of the United States by lending the U.S. money that can never be repaid?

These are all political questions, and only political decisions will answer them. Some of these questions may be answered as soon as this weekend at the international conference in Washington. Answers to some of the other questions probably will be conveyed in advance to certain insiders — like the financial houses that serve as the market agents of the central banks — and those insiders will get richer. As good as this conference is, you will not be hearing from any of those insiders here.

But we may gain some confidence from politics too, since we know that governments are no longer shy about intervening in the markets and since central banking was invented precisely to inflate, to avert debt deflation, to devalue the currency when that is deemed necessary or convenient by those in power — which is most of the time. We know that the world is now drowning in debt, and in a research paper published in May 2006 a British economist, Peter W. Millar — founder of Valu-Trac Research in London, formerly an executive with the Abu Dhabi Investment Authority — forecast that to avert debt deflation and to increase the value of their monetary reserves, central banks would need to increase the value of gold by at least 700 percent and maybe by as much as 2,000 percent. This could be done easily, for to increase the value of their monetary reserves central banks need only to stop selling and leasing gold and to stop subsidizing the sale of gold derivatives by their agents, the financial houses. Revalued high enough, gold could cover all government debts and let the world start over again.

Millar kindly has given GATA permission to post his research paper at our Internet site, and you can find it here:

http://www.gata.org/files/PeterMillarGoldNoteMay06.pdf

When Millar made his forecast about such an upward revaluation of gold — 2 1/2 years ago — gold had just reached $700 per ounce, not far from where it is now. Multiplied by 700 percent, that would mean a gold price of about $5,000 per ounce. Multiplied by 2,000 percent … well, if that happens, we may be able to afford to hire someone to do the math for us — if, of course, those of us who do not live in free countries like China and Russia are allowed to keep our gold. But that is still another political question.

==========================

“Nothing will unnerve the paper gold shorts more quickly and do more to undercut their confidence than to strip them of the real metal and force them to come up with more hard gold bullion to make good on deliveries. “Stand and Deliver or Go Home” should be the rallying cry of the gold longs to the paper gold shorts.” –Trader Dan Norcini

==========================

Gold’s Assault on the Clueless – Rick’s Picks

By: Rick Ackerman of Rick’s Picks

We’ve been monitoring gold’s vital signs closely, since any foray above $1000 is cause for nervousness. The yellow stuff has always been free to roam, and even to misbehave, below that threshold; but once above $1000, the bankers regard each rally with a glower of malice. While it is clear that debt deflation’s overwhelming power has rendered the central banks impotent in their efforts to arrest the collapse of the global economy, the bankers still retain the ability to crush any hint of rebellion by gold bulls who would deign to challenge the monetary order. With their relatively large stocks of physical gold, and the complicity of institutional agents such as JP Morgan to help suppress “paper gold” in futures markets, the bankers and the IMF have enough influence over bullion’s price to temporarily suspend the laws of supply and demand.

The politicians are on board, of course, although not as conspirators. They are all knee-jerk Keynesians at the moment, either too stupid and/or lacking in imagination to understand why fiscal spending, no matter how much of it, cannot possibly extricate the economy from a deflationary black hole. They have put their trust in eggheads and MBAs to fix things, even if most of us have begun to suspect that throwing yet more trillions of dollars into the maw of deflation will not solve anything. And although our elected leaders might not feel so strongly about gold as Keynes, who was appalled by the popular appeal of “that barbarous relic,” they are nonetheless dumbfounded as to why anyone would prefer gold-backed currency to the Monopoly money that The Government has empowered as legal tender.

Concerning our immediate outlook for gold, we have identified 1025.20 as the next significant point of resistance for the Comex April contract. The number is yet another in a series of Hidden Pivots that have told us unequivocally and at each step along the way whether buyers were ready to forge effortlessly higher. So if 1025.20 gives way easily, as other points of resistance already have, we’re ready to infer that the benighted acolytes of Keynes are about to get fragged by investors who are growing increasingly restless, if not to say panicky, about The Government’s apparent powerlessness to ameliorate economic distress.

(If you’d like to have Rick’s Picks commentary delivered free each day to your e-mail box, click

==========================================

====================================

Only Seller Left? – Silver Seek

Source: Silver Seek Author: Ted Butler

The COT, for positions as of the close of business February 10, the total commercial net short position increased by 1864 contracts for the week. However, the net short position of the 4 largest traders increased by 2832 contracts. This means that of all the commercial traders, the only short selling came from the 4 largest traders, with all other commercial traders (the 5 through 8 largest traders and the raptors, the 9+) buying. This was very unusual, in that the commercials generally operate as one cohesive unit, all buying on the way down in price and selling on the way up.

Even more unusual is that this pattern has persisted back to the December 22, COT report. On an almost $2.50 rise in the price of silver since then, the total commercial net short position has increased by 4357 contracts, yet the big 4 have increased their net short position by 5396 contracts. This means all new short selling in COMEX silver has come from the biggest traders, for the first time in memory. That should be enough for any semi-alert regulator to conclude manipulation, as such concentrated short selling by so few participants should have every alarm and whistle blaring at CFTC headquarters. After all, there could be no clearer motive for such selling – the capping of price for the purpose of protecting already obscenely large short positions.

But even while it is easy to conclude that all new short selling is coming from the same four or less large traders, where do I get off suggesting it is one entity behind all the new silver short selling over the past 7 weeks? Here we have to look at another CFTC data source, the Bank Participation Report. Since the Bank Participation Report (BP) is a monthly publication, while the COT is weekly, we must make appropriate calibrations between the reports. The two most recent BP reports are as of January 6 and February 3. Using those two reports, plus the COTs of the exact same dates, this is what the reports show. Between those two dates, the COT indicates that the total commercial short position increased by 2253 contracts, with the big 4 category increasing by 2256 contracts, once again accounting for more than the entire increase in the commercial category.

The Bank Participation Reports corresponding to January 6 and February 3 indicate that the two U.S. banks increased their net short position by 2500 contracts in that same time period. This proves, at least during this specific period of time, that one or two U.S. banks accounted for more than 100% of all the commercial short selling and all the selling in the big 4 category. One or two entities, accounting for more than 100% of all total short selling for more than a month is manipulation. Period. It can only have occurred to attempt to cap the price and protect the existing short position.

Please remember that while I have been documenting the incremental changes in the concentrated short position of what may be one large trading entity, those changes are small compared to the total short position of this entity, which I estimate to be back above 30,000 contracts, or 150 million ounces. That’s more than 22% of the entire annual world mine production of silver. It is impossible for such a large concentrated short position not to be manipulative.

I’m fed up with the CFTC and their so-called investigation. They claim to be investigating , while the manipulation grows more obvious. I think we’ve passed the point where we can eliminate incompetence as the explanation for their inaction. I have a good idea of what is behind their refusal to right a very obvious wrong, although I won’t get into those details here. Let me just remind them that while they may fear the possible ramifications of a truly free silver market, after decades of manipulation, the greatest damage is their abandonment of the rule of law.

(Editor’s note – here’s a detailed report of Ted Butler’s past and present dealings with the CFTC regarding the silver manipulation –

http://www.investegate.co.uk/invarticle.aspx?id=66705)

====================================

“Nothing will unnerve the paper gold shorts more quickly and do more to undercut their confidence than to strip them of the real metal and force them to come up with more hard gold bullion to make good on deliveries. “Stand and Deliver or Go Home” should be the rallying cry of the gold longs to the paper gold shorts.” –Trader Dan Norcini

====================================

Silver, Past, Present, Future – Phoenix Silver Summit Speech – Silver Seek

Source: SilverSeek.com

By: Theodore Butler

Second, I’d like to thank my friend of 25+ years, Israel Friedman. It was Izzy, who back in 1984, issued to me the challenge to prove him wrong in his analysis of silver. Although I had traded and invested in silver for years before his challenge, I admit to never having studied it in depth. Izzy’s claim that the world was and had been consuming more silver than was being produced seemed so at odds with the price at that time, that I took up his challenge. I also admit that I thought it would be easy to prove him wrong, although I was well aware of his buying of silver in the $4 range and then selling it in the $40 range a few years later. When I discovered that he was correct, it set off a thought process that I couldn’t satisfy. I couldn’t reconcile how there could be greater demand for an item than there was current production with prices not moving higher. I’m sure that many had also been deeply perplexed with that puzzle.

For some reason, rather than to simply dismiss and put out of mind something I couldn’t figure out, I thought long and hard about the silver supply/demand/pricing enigma. It was that thought process, plus my background as a commodity broker, that led me to the conclusion that the silver market was manipulated by excessive short selling on the COMEX. The actual Eureka Moment came one day as I reading the Wall Street Journal Commodity Tables. It wasn’t an accidental discovery. I was looking for something wrong. I was looking for anything that was different about silver that could account for it’s very different behavior compared to other commodities. After all, we were all taught that when consumption is greater than production, price must rise. Yet silver didn’t. The light bulb went off in my head when I realized that COMEX open interest, when converted into real world supplies was completely out of line with every other commodity. This meant that the derivatives market in silver was larger than the underlying host market from which it was derived. A complete absurdity. The paper market tail was wagging the physical market dog. This is something that has remained constant in the subsequent 25 years of manipulation.

Much later, I would come to understand the role of leasing in the silver manipulation, which answered a lot of open questions in my mind. It was Izzy who caused me to be bitten by the silver bug, just as I may have, in turn, infected others, who in turn infected still more. The good news about this silver virus is that instead of giving you the flu or killing you, it could make you rich. For introducing me to silver, thanks Izzy

Finally, I’d like to thank my wife, Mila, who has been subjected to my preoccupation of silver for the entire duration. While I have both suffered along the way and enjoyed the journey, it was always my choice to continue or not. I know it was much harder for Mila as a partner, and a I marvel at her ability to persevere where I know I could not, were our roles reversed. Thanks Mila.

The Past.

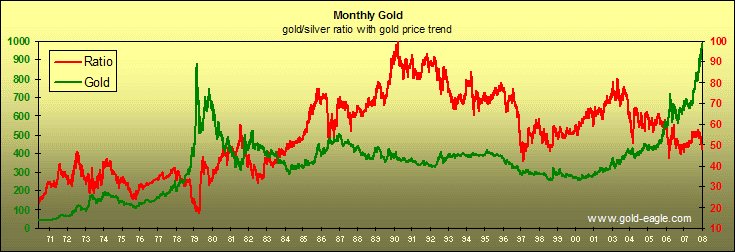

The silver story goes back, quite literally, for thousands of years. You won’t find many stories of longer duration, except if you’re an archeologist. For those thousands of years, it was prized as money and jewelry and for ornamental objects and as a measurement of wealth. Silver’s history is similar to its precious metals brother, gold. Both precious metals were the cause of exploration and the discovery of new worlds, and instrumental in the development and formation of nations, including war. Both gold and silver were dug out of the ground and held and accumulated throughout the ages. For use as money, governments for hundreds of years assigned a fixed ratio of roughly 15 to 16 ounces of silver being worth one ounce of gold. This made sense, because that ratio was close to the rate at which silver came out of the ground compared to gold. There was a lot more silver accumulated above ground than gold, so it further made sense that 16 ounces of silver was equal to one ounce of gold. In the late 1800’s tremendous new silver production came to market, due to the massive supplies from the Comstock Load in the western US. Coupled with a demonetarization of silver, but not gold, by many world governments the price of silver plummeted and with that the amount of silver needed to buy one ounce of gold rose to 100 ounces in the 1920’s. The world was truly awash in silver.

Coincident with these developments, starting about 100 to 150 years ago, around the same time that the world found itself awash in silver, something else dramatic was occurring. We began to enter the industrial age. Inventions and devices of all kinds began to be introduced, impacting the world as never before. Electricity came into wide use. The automobile was born. Photography was introduced. As dramatic as this overall change was to how people lived, the transformation in silver was even more dramatic. It turned out that the substance that the world was awash in, the substance that had been accumulated for thousands of years, had properties that no one could have contemplated through the vast sweep of history. This largely too abundant material was a perfect fit for the rapidly transforming modern and industrial world. Silver was, and is, the best conductor of electricity, the best heat transfer agent, the best reflector of light, a marvelous lubricant, a versatile catalyst and alloy for a wide range of industrial applications, including medical. Silver was the key ingredient that made photography possible. All these uses, plus abundant supply and cheap prices. It was the perfect consumption set up. And consuming silver is something the world took to in a very big way, until this very day.

It was the push into the modern age that caused a parting of the ways between silver and gold in how they were used. Gold has many potential industrial applications, although not near as many as silver. But because gold was, and is, so high-priced compared to silver, it wasn’t practical to use it in widespread industrial applications. Because silver was so cheap and abundant, it was used extensively. So extensively, that not only did the world begin to consume every ounce of silver that was taken from the ground, it also began to consume the accumulated inventory from the past.

In 1940, there were approximately 10 billion ounces of silver above ground in the world, with half owned by the US Government. At that time, there was about a billion ounces of gold. Ten times more silver existed in the world than gold. After more than 60 years of over-consumption of silver, of drawing down and depleting the inventories built up over hundreds and even thousands of years, the relationship of how much silver exists above ground compared to gold has flipped. Now there is much more gold left in the world than silver. Currently there are up to 5 times more gold in the world than silver, depending on how you define inventory. Silver inventories have declined from 10 billion ounces in 1940 to 1 billion today. The U.S. government, the largest owner of silver in 1940, with over 5 billion ounces, now owns zero ounces. Gold world inventories, including jewelry, have increased from 1 billion ounces in 1940 to 5 billion today, according to all reputable sources like the World Gold Council.

I ask you to think about that for a moment, there being more gold than silver aboveground, as this is one of the most important factors in silver today. It is also one of the least known facts, even though it is easily verifiable and has evolved over such a long time. When people first hear or read it, they instinctively disbelieve it. 99.9% of the people on the planet, to this day, would tell you that it can’t possibly be true that there is more gold than silver in the world. Or even that there is an equal amount of gold and silver. None of this 99.9% has ever taken even a minute to think about it or read or try to verify how much of each remains above ground. They don’t have to. Their verification comes everyday, as it has everyday for decades, from one simple source – the daily price of each. The price of silver and gold is broadcast constantly, to every nook and cranny around the world, that there are 60 to 70 to 80 times more silver in the world than there is gold. That’s what 99.9% of the people in the world think. And I’m not just talking about uneducated people in third world countries. I would include the most sophisticated, wealthy and educated people, who have come to believe that the price doesn’t lie. I do hope 99% of the people here don’t think that.

It is this simple fact, that the relative price of silver compared to gold is so distorted, relative the their respective quantities in existence, that is all anyone needs to know to buy silver. This is not a knock on gold. I will stipulate to and accept as true every bullish argument that anyone could make on gold. You could spend hours or days lecturing me on all the good things that gold has going for it, and I will accept them without dissent. When you are done giving all the bullish gold arguments, I would just add two things. One, all those arguments apply to silver as well, and two, there is less silver than gold.

I’m compressing hundreds and even thousands of years of silver history into a few minutes of time. For many centuries, the world dug up and used silver for money and beauty and wealth. In the last century or so, we discovered incredible new uses for this age-old material and continued to dig it out of the ground, in ever increasing quantities, basically consuming all the newly mined silver plus almost all of the old stuff as well. And even though this is a fairly easy set of facts to verify, only an infinitesimal amount of people are aware of how little silver remains. And in spite of the growing rarity of this age-old cherished and desired material, its price, on any objective measure, is dirt cheap. There is less silver in the world on a per capita basis, than in history, yet the price still reflects super abundance. At the risk of over using a statement I’ve made in the past, I couldn’t make this up if I tried.

The Present

I’m going to include the 5 years or so, maybe even a little longer, as part of the present. Today, thanks to the Internet and other means of communication, including conferences like this, the true silver story is coming out. I think I’ve played some role in that. Investors, in ever growing numbers are grasping the disconnect between the price and the true value existing in silver. It is this disconnect that presents an exciting investment opportunity.

Perhaps the most unique and attractive characteristic about silver is its dual role as a vital industrial material and its history and desirability as an investment asset. No other commodity comes close to silver in this regard. Of course, we need copper and zinc and lead for industrial purposes, but they have never been considered popular investments in their pure metal state. Same with other natural resources, like oil. None of these commodities can be practically held in one‘s personal possession. Gold is the primary investment metal, but its high price prevents widespread industrial use. Platinum and palladium are both precious metals and are used extensively in industrial applications, but have not evolved into broad and popular investment assets.

As the true dual role material, silver stands alone. In its industrial consumption role, silver demand has been so strong for the past 60 years, that it has depleted inventories that took hundreds of years to accumulate. Now that industrial demand has been interrupted by current bleak economic circumstances, investment demand is stepping in to take up the slack. And make no mistake, the evidence clearly indicates that an investment rush is developing in silver.

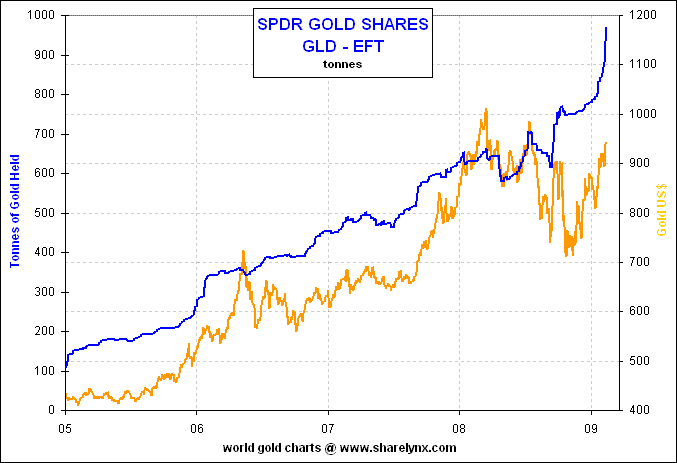

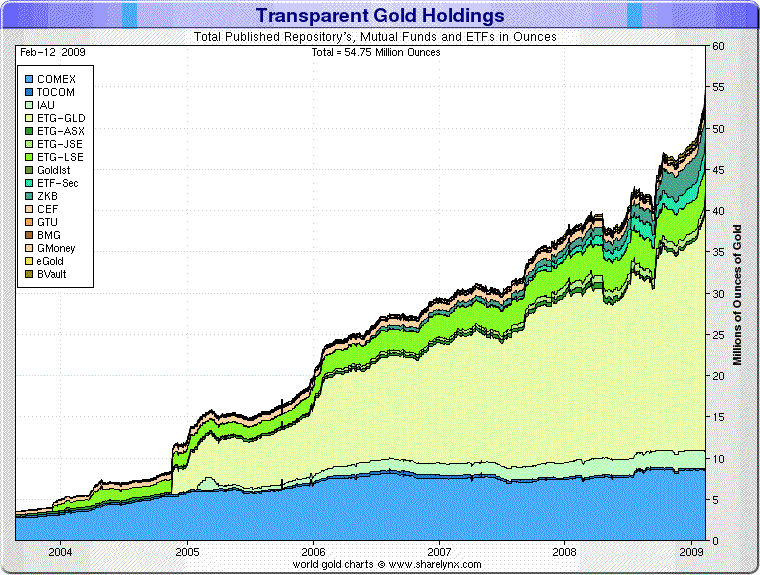

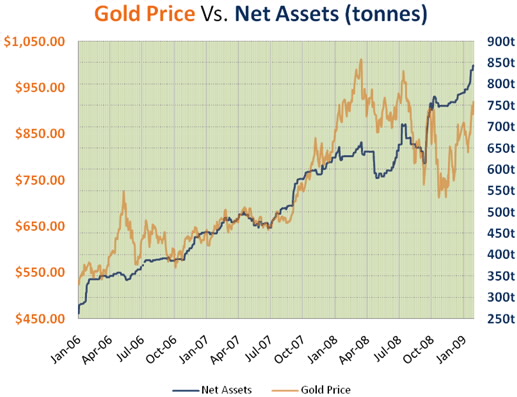

The introduction of the silver and gold ETF’s (Exchange Traded Funds) has been the single most important factor on the investment side of silver’s dual role. Since the introduction of the first silver ETF, less than three years ago, over 300 million ounces have been absorbed by the various silver ETF’s. That is remarkable and much more than I ever thought they could accumulate. More importantly, these ETF’s will turn out to be, in my opinion, what my friend Carl Loeb has nicknamed, the Death Star, in that they may absorb all the world’s available silver.

Lately, I’ve noticed quite a bit of suspicion and criticism concerning the legitimacy of the ETF’s, particularly the gold ETF’s, with the criticism centered on whether the real metal exists that is said to be on deposit. I’d like to add my two cents. Quite frankly, I don’t understand this criticism. If someone would prefer to own metal in his own possession or control, they should do so. It’s an easy choice. Certainly, this has always been my advice. And it’s not like the ETF’s are beyond criticism, and I have publicly done so in the past when I detected massive unreported short selling in the big silver ETF, SLV. I think that’s fraud, and I think there is currently a big unreported short position in SLV.

But that’s not what the current criticism of the gold ETF’s is all about. The current criticism revolves around allegations that the metal said to be deposited is not really there, even though serial numbers and weights of all bars are listed. It seems some are claiming that the big quantities of gold flowing to the ETF’s are beyond anything reasonable. Where can all this metal be coming from? While I can’t personally guarantee the metal is in the ETF’s, nor do I wish to, I don’t understand this line of thinking. The gold ETF’s have been accumulating gold for more than 4 years. In that time, roughly 50 million ounces have been absorbed by the all the gold ETF’s. That’s one percent of all the gold in the world. Even if you reduce the 5 billion ounce gold inventory by 60%, and say there is 2 billion ounces of gold in good-delivery bullion bar form, the 50 million ounces in gold ETF’s is only 2.5% of that 2 billion ounces. Is it so hard to imagine 2.5% of anything being accumulated over 4 years and with more than a doubling in price? After all, the silver ETF’s have accumulated almost 30% of total world bullion inventories and little is said of that by gold people.

The fact is, for the most part, the investors who buy the silver and gold ETF’s are institutional investors who probably wouldn’t buy the metal if the ETF’s didn’t exist. You would think the gold analysts criticizing the ETF’s would recognize that. The buying in the silver and gold ETF’s are a very big reason behind the doubling in price in a few years. You would think metal people would be cheering the ETF’s on, instead of complaining. Go figure. Look, I understand that investment demand in mining shares has probably suffered as a result of buying in ETF’s, but that’s a different issue and is no reason to claim that the gold ETF’s don’t have the metal. Metals prices wouldn’t have climbed if there was no metal demand from the ETF’s.

Back to silver investment demand. Aside from ETF demand, the past year has seen other compelling evidence of an investment rush into silver. For the first time in any of our lifetimes, we have witnessed a persistent retail investment shortage, characterized by soaring premiums and delays in product delivery. I have to laugh when some people say there is no retail shortage, as the very definition of a shortage is rising premiums and delays in deliveries.

Also, we have witnessed, for twelve straight months, something never seen before. The US Mint, even after doubling its production capacity, hasn’t been able to fully supply Silver Eagles in the quantities demanded, for the first time in the 23 year history of the program. There is no doubt in my mind that my friend Izzy is responsible for kicking off the rush into Silver Eagles with his article in December 2007. I know of no one else who recommended Silver Eagles, then or now.

The current economic collapse has resulted in a sharp drop in industrial consumption of all commodities, including silver. Production, while falling, has not yet fallen as much. It will, given silver’s byproduct production profile. So, temporarily, we have a “surplus” of silver. Unlike other industrial materials, the surplus in silver is being gobbled up as an investment. Instead of being dumped into exchange warehouse inventories, like copper, zinc, or other industrial metals. Once production of all these metals falls sufficiently enough to balance with industrial consumption, as it must, there should be a shortage in silver that will seem unreal.

The economic condition of the world is dreadful. That it came like a thief in the night makes it more ominous. When and how we turn this around, I haven’t a clue. Many of us have worried about this for 30 years or more, hoping it would never come. Despite that hope, the wolf has come to the door. We must deal with it. Fortunately for silver, these scary economic times rev up investment demand. The worse economic conditions become, the more silver investment demand should grow. Silver is positioned well for whatever economic conditions prevail.

The Future

I want you to do me a favor. I want you to play a little game of imagination with me. It may sound silly at first, but try to play along, as I want to make the central point of the day. I want you to imagine that in this room, right there, in the space between you and me, is a giant elephant. Not a regular elephant, mind you, but the biggest elephant ever documented. A 26,000 lbs African Bush Elephant, 14 feet tall in the shoulders, with absolutely massive tusks. I looked this up, so I‘m not misstating the dimensions. Not only is this the biggest elephant ever recorded, it’s loud, agitated and it stinks to high heaven, flapping its ears and swinging its giant trunk. And it’s right there and has been right there the whole time. I want you to imagine that you’ve been sitting there, listening to me talk about silver with this 13 ton elephant right there, interrupting my speech all along and scaring the dickens out of you. And the kicker is that we’re all trying our best to ignore the elephant. Pretending it’s not there, speaking around it. We’re all trying to act like it’s perfectly normal to be in a room speaking about silver with this giant elephant and trying to act like it’s not there, when it clearly is there.

The African Bush Elephant in the room is the silver manipulation. But whereas the elephant is imaginary, the silver manipulation is as real as rain. But like the imaginary elephant, most are doing their best to pretend that the silver manipulation doesn’t exist. Not me, of course, as the manipulation is the most important pricing factor in silver, and I write on it continuously. I sense I have convinced many thousands of readers that silver is manipulated and maybe many in this room. But it is absolutely amazing to me how so few analysts and industry people publicly speak out on the manipulation.

I’m talking of people working for the financial firms and banks whose job it is to follow and write about silver. I’m speaking of those in the mining industry and in particular the Silver Institute. I’m not complaining about this lack of manipulation talk. Maybe at one time it upset me to be so alone, but not anymore. Now it’s just amusing. I read everything there is to read on silver and 95% of what I read never refers to the manipulation in any way. I find that bizarre. I find that to be the real life equivalent to my previous imaginary exercise of the elephant and pretending it’s not in the room.

I’m not demanding that anyone agree with me about silver being manipulated. I’m human and I reserve the right to be wrong. Besides, it’s better for me to be the only making this the main issue. In the past, many did challenge and attempt to refute my allegations of manipulation, especially those in the mining industry, which never made much sense. But as the issue has become so specific as to the documented facts about the concentration, I’m not even hearing lately anyone explaining why I am wrong or answering simple questions, even on the Internet. If there is one thing I have learned about the Internet, because of its shield of anonymity, many love to tell you why you are wrong and they are right, and in generally a rude manner to boot. But I’ve asked the question for 6 months for how can one or two U.S. banks being short 25% of the world silver production not be manipulative, with no response. I was seriously considering running a contest with a reward for every legitimate answer.

Stranger still in the collective avoidance of even talking about a potential market manipulation is that the prime regulator, the CFTC, has initiated a formal investigation into my allegations of manipulation in silver. This is the third silver investigation in less than five years, and the first by their Enforcement Division. This has never occurred in any other commodity. Regardless of the outcome of the investigation, the fact that there is another investigation is extraordinary, in and of itself. Nothing could be a more important issue than whether any market is manipulated or free. You would think that there would be wide discussion on the potential outcome or the merits, pro and con, on the investigation itself. Instead, mum’s the word. That so many establishment analysts and mining and industry people can pretend that everything has been completely aboveboard in silver is more bizarre than my elephant in the room example. Especially now that the CFTC has stated that they are investigating.

Like all manipulations, the silver manipulation has resulted in an artificial price level. Unlike most manipulations, the one in silver is a downward price manipulation. Admittedly, that does make it harder for folks to grasp the issue. But the saving grace to this manipulation is that those not involved in the manipulation can take advantage of the artificially depressed price. The special essence of this manipulation is that outsiders can profit from it in a simple and easy manner. All you have to do is buy and wait.

Like all manipulations, the silver manipulation will end suddenly and the price must move sharply in the opposite direction of the manipulation. In this case, the price of silver will explode upwards, once the manipulation is terminated. Those holding silver when that occurs will be rewarded. This is not complicated.

But what happens if the CFTC’s investigation ends with them, once again, finding that no manipulation exists in silver? It doesn’t matter. The silver manipulation must end, suddenly and violently, to the upside, no matter what the CFTC says or does. I wouldn’t be no naïve as to depend on the CFTC for doing the right thing. The price, having been depressed so low and for so long, must result in a shortage. The shortage has been clearly evident in the retail market for more than a year. Not as clearly, but present nevertheless, are strong signs of a wholesale shortage in the unreported shorting of SLV shares and other wholesale indications. When this shortage hits in earnest, no one will be able to stop the sudden demise of the silver manipulation.

You might further ask, “If the manipulation in silver will end regardless of what the CFTC may or may not do, why do you (meaning me) persist in focusing on this issue? Why not just sit back and let it happen? Well, I have no choice in waiting to let it happen, so I guess the question is whether to keep quiet about it. The answer to that is while the manipulation presents the strongest reason for buying silver, it is a market crime of the highest order. There is no more serious market crime than manipulation. It is the equivalent to Murder One, Treason or kidnapping.

In addition to providing the most compelling reason for buying silver, the manipulation is a crime in progress. As such it offends my sense of what is right and wrong. Being the best reason for buying silver and being a crime in progress are not mutually exclusive. Just like recommending that people buy silver and write to the regulators and lawmakers complaining about the manipulation is mutually exclusive. And I am gratified that so many have taken the time to contact the regulators, as it has really made all the difference in the world.

In conclusion, the supply/demand set up in silver, which has evolved over an incredibly long period of time, has been one continuous process promising to culminate in an explosion in price at some point. Quite simply, we are rapidly approaching that defining moment when there just won’t be enough physical material to go around at anything but rapidly escalating prices. Those escalating prices will encourage and drive others, including industrial consumers, to enter what should become a buying frenzy. Superimpose upon that the sudden destruction of a decades-old downward price manipulation and you have all the necessary ingredients for price event that will be referred to forever.

Thank you and I’d be happy to take any questions you might have.

================================================

“Nothing will unnerve the paper gold shorts more quickly and do more to undercut their confidence than to strip them of the real metal and force them to come up with more hard gold bullion to make good on deliveries. “Stand and Deliver or Go Home” should be the rallying cry of the gold longs to the paper gold shorts.” –Trader Dan Norcini

=====================================

My Final Note for today: How long are we going to continue to let 1 or a few Banks disctate the prices of Gold and Silver. If you read their short position is 22% MORE than world’s production in Silver! Everyone needs to be contacting Comex, CFTC, FTC, SEC,and the Federal Justice Dept and screaming their outrage at this! Plus it being allowed to continue! The other action step is to take physical delivery! Sooner or later by bringing all these pressures to bear, (no pun intended), we will see the “Short Squeeze of the Century” as these traders/manipulators will be forced to cover their Short Positions. Just how long are we going to let them do this to us? Good Investing – Jschulmansr now you can also follow me on twitter just click here and be notified every time I make a post and the best part it is absolutely free!

===================================

“As we saw the gold price attack the $1,000 level for the second time, but with far more force, institutional investment demand continued to drive the gold price, forcing the closure of ‘short’ positions [selling when the seller doesn’t have the gold] on COMEX and stunting both jewelry and Indian demand, where higher prices have at least temporarily sidelined these buyers.

“As we saw the gold price attack the $1,000 level for the second time, but with far more force, institutional investment demand continued to drive the gold price, forcing the closure of ‘short’ positions [selling when the seller doesn’t have the gold] on COMEX and stunting both jewelry and Indian demand, where higher prices have at least temporarily sidelined these buyers.

Gold’s recent move above $900 has analysts scrambling to increase their price targets.

Gold’s recent move above $900 has analysts scrambling to increase their price targets.

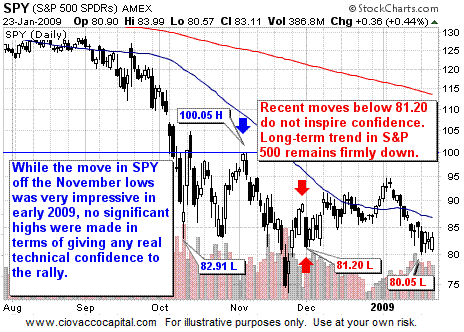

U.S. Stocks: Downtrend Remains In Place

U.S. Stocks: Downtrend Remains In Place Recent weakness in the S&P 500 Index leaves open the possibility that we will revisit the November 2008 lows around 740 (intraday). If those lows do not hold, a move back toward 600 becomes quite possible. On Friday (1/23/09) the S&P 500 closed at 832. A drop back to 740 is a loss of 11%. A move back to 600 would be a drop of 28%. These figures along with the current downtrend highlight the importance of principal protection and hedging strategies.

Recent weakness in the S&P 500 Index leaves open the possibility that we will revisit the November 2008 lows around 740 (intraday). If those lows do not hold, a move back toward 600 becomes quite possible. On Friday (1/23/09) the S&P 500 closed at 832. A drop back to 740 is a loss of 11%. A move back to 600 would be a drop of 28%. These figures along with the current downtrend highlight the importance of principal protection and hedging strategies.  Gold & Gold Stocks Still Face Hurdles

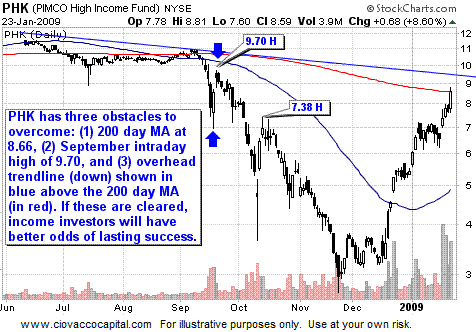

Gold & Gold Stocks Still Face Hurdles

Run In Treasuries Is Long In The Tooth

Run In Treasuries Is Long In The Tooth

Strength In Bonds Shows Little Fear of Price Inflation

Strength In Bonds Shows Little Fear of Price Inflation

U.S. Dollar Remains Firm

U.S. Dollar Remains Firm

follow the Democrat into the Oval Office, with a U.S. Supreme Court conference on the dispute set after the Jan. 20 inauguration.

follow the Democrat into the Oval Office, with a U.S. Supreme Court conference on the dispute set after the Jan. 20 inauguration.