Gold Report: Sean Rakhimov Stock Market Will Recover; Economic Crisis Far From Over

Souce: The Gold Report

By: Sean Rakhimov of Silver Strategies.Com

As SilverStrategies.com editor Sean Rakhimov tells us in this exclusive interview with The Gold Report, the economic crisis may go on for a generation but the market is a separate animal that will stir back to life sooner. He expects physical gold and silver to lead the parade, with base metals lagging 12-18 months behind, followed by share price recovery for the majors and on down the line. When picking stocks to buy now, he says investors have to decide for themselves whether a company will survive the washout; it may be tough going from here to there, but sticking with survivors should prove beneficial in the long run.The Gold Report: Let’s start with your take on where are we today, what has happened, and where we’re going from here.

Sean Rakhimov: Basically we’re in a situation that we’ve long expected. We all anticipated a big financial crisis, all sorts of problems, an end-of-the-world type of scenario—not literally, but the world as we know it. And I think we’re there. This is the big one and it’s for real. Where we go from here is largely a function of what the powers-that-be will do. We have some idea of what they will do; they will do all the things that will make it worse. I go by the theory that they will always do the right thing, but only after they exhaust all other options.

TGR: When you say the big one, how much further are you expecting both the markets and the international financials to erode?

SR: The markets are a separate story. Don’t confuse what the markets will do with the general crisis or economic situation. Markets are a different animal; they can do all kinds of things that do not fit into your thinking or should not have happened given the economy or the political situation, or what-have-you. I want to be clear on that so that people don’t assume that if I say, “Oh, this is going to last a while, that automatically means the market is going to not recover for a long time.” The economic crisis, I think, is going to last for a generation. I foresee a twofold crisis here, or maybe three stages. The first one is what we’re going through right now – a debt crisis.

At some point down the line we’re going to have a currency crisis, where the dollar will stop being the reserve currency of the world. I don’t know how long before that happens. It’s a matter of whoever runs first to the door, basically. I was just reading some articles. Iran is converting their foreign exchange reserves into gold. China is trying to do some of that. It only takes a few of these until there’s a domino effect and when that happens, things should play out quickly.

TGR: What do you mean “play out quickly”?

SR: This crisis, I think, has been a good example, where within three months we ended up in a completely different environment. If the dollar stops being the reserve currency of the world tomorrow, I expect things to happen quickly. It may take a decade until it gets started, but once it starts, I expect things to unravel quickly. The reason for that is we have maybe 20 to 30 major players in the world that can make a difference. I’m talking about countries and maybe some other entities such as sovereign funds. And I believe it’s going to be very difficult to bring everybody to the table and get them to agree on a plan that everybody would sign on to. Even if they did sign on, I think it’s going to be very difficult to make sure everybody sticks with it.

As soon as they break ranks, I think within six months the whole thing is going to break apart. Whatever accord they come up with, if it’s going to be Russia or China or somebody of that size, things are going to happen even quicker. If it’s going to be a smaller player like Iran or Venezuela, that may take a bit longer. The significance of it may be downplayed for a period of time. But ultimately I think most people understand the dire straits we’re in. At some point it’s going to be “everybody for themselves” and that’s when I think the current system is going to fall apart.

TGR: You’re suggesting the dollar will stop being the world currency and countries will make some attempt to come together to create the new world currency. Might that be gold or precious metals?

SR: I don’t think the adoption of gold or a derivative thereof as a reserve currency is going to come from governments, at least not voluntarily. Eventually, I think they will be forced to.

TGR: Wasn’t that the original part of the Bretton Woods agreement?

SR: Yes, it was, where the U.S. dollar was as good as gold and was convertible to gold, but we know how that ended.

TGR: You said this crisis could go on for a generation. That’s a long time.

SR: I foresee maybe several stages of this crisis unraveling and that’s why I say it’s going to take about a generation. As I said, the first one is the big debt crisis we have now. Maybe an extension of it will be some sort of a currency crisis. It’s not just a dollar that won’t be worth anything, but most other currencies as well. And then I believe what’s going to really, really change the environment and exacerbate the situation will be an oil crisis. I do expect oil to hit a new all-time high, say, by 2011. So within two to three years I would think that’s going to happen.

TGR: How low will we see oil go this time around?

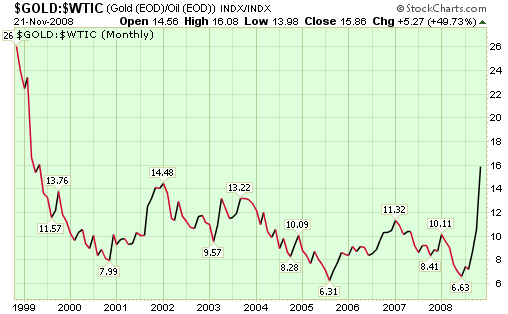

SR: I don’t have a number on that because I don’t “buy these prices” on anything. These prices are largely a function of paper transactions, and yes, some transactions are taking place at these prices. Look at your Blackberry; a pound of copper is a brick that size. How much work, how much effort, how much energy goes into that and you can buy it for $1.50 or something in that range. Think to yourself, what else can you buy for $1.50? I was in Europe a few weeks ago. You can buy a bottle of water for €3, which is about $4. A cup of coffee costs that or more. I don’t know what you can get for $1.50 anymore; whereas you can get a piece of copper the size of your Blackberry for $1.61 today. The prices today are completely, absolutely bogus. Companies have to mine and sell their products at these prices. But if you recall our conversation in the last go-round, I said at some point I expect a complete reevaluation of most things, but commodities in particular. (Go to http://seekingalpha.com/article/84220-sean-rakhimov-3-digit-silver-ahead)

TGR: When you say commodities, are you doing base metals, precious metals?

SR: Everything. Everything that has an intrinsic value. Here’s the situation. Suppose three of us represent countries. One has oil, the other has wheat, and I have copper. If I want to buy your oil, I go back to my printer and print up as much money as I can and buy your oil. Well, the one with the wheat will do the same thing, print up as much money as possible and try to buy your oil. At some point people will stop accepting these currencies, whatever they are, because there’s no limit to them. Money is printed like leaflets. There’s no backing to it. When we get to the stage where there isn’t enough to go around—like you go to a gas station and you can’t get all the gas you need—the reevaluation will be forced on the market and will be forced on all the players. So, unless you have something else to offer, something of substance other than your paper money, I don’t think you’re going to get any of whatever it is you’re looking for.

So I do expect some time in the next decade that the oil market will fall apart. Whenever the deficit between production and consumption reaches a level where it’s going to start to have severe impact on availability and price, I think countries will go to direct contracts. That would be nothing new; such markets exist today, say, in uranium, where direct contracts are the main market and the futures market is basically an addendum. It’s more of a financial management tool for participants, rather than the market that determines anything significant.

TGR: At what level might the supply deficit trigger direct contract transactions in oil?

SR: Right now the supply and demand is about 85 million barrels a day supply against 87 million roughly in consumption. Suppose those numbers get to 90 and 95 (million barrels a day of consumption). At some point the shortage will become so severe that it’s going to wreak havoc in the marketplace. Those who have the oil will start to choose who they sell it to and in exchange for what. And I don’t think it’s going to be paper. That’s my longer term outlook.

TGR: What should investors be doing?

SR: It depends on the timeframe. If you’re talking about stocks, investors should take a hard look at their portfolios and ask themselves one question. Go through each stock and say, “Is this company going to be around on the other side of this financial crisis?” It may take six months; it may take three years for all I know. But if the company survives this current situation, I believe the benefits are going to be tremendous. Unfortunately, getting from here to there will be tough. It is already very, very difficult to get any kind of financing. And as we know, the mining (exploration) sector lives by it for the most part. A lot of these projects require large capital expenditure, either for exploration or development. Otherwise, they can’t do it.

TGR: Have you gone through your grid and come up with a list of companies that make the grade?

SR: I would be reluctant to discuss specific companies, particularly because investing is about the investor. If you want a simple version, stick with the major blue chips—but even then, survival is not a given. For instance, a company like Teck Cominco Ltd. (TSX:TCK.A) (TSX:TCK.B) (NYSE:TCK) is in a serious situation and the stock has plunged dramatically; it’s been one of the blue chips for the longest time and they’re a very conservative company.

TGR: Any other suggestions?

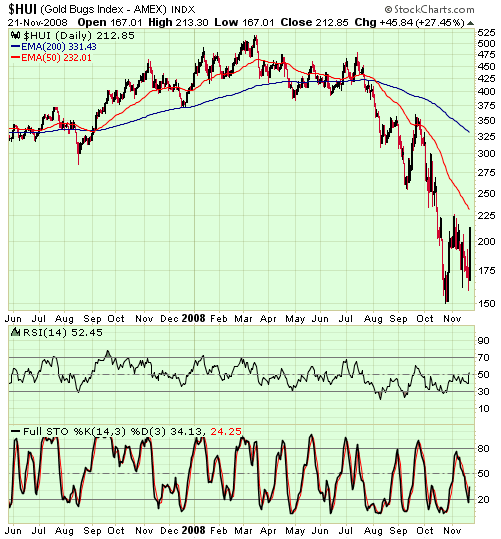

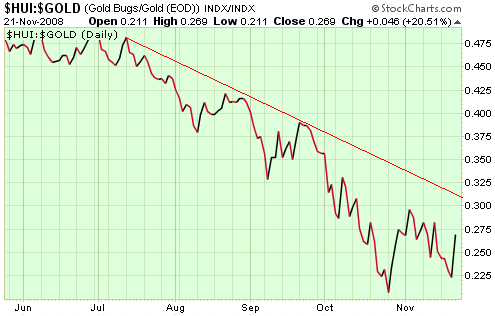

SR: If you need a guideline, the way I expect the market to play out going forward is for gold and silver to come back first. Base metals will probably lag behind by about a year to 18 months. When I say “come back,” I mean this downtrend in their price in the marketplace will reverse. Within two or three quarters after that, majors such as Newmont Mining Corp. (NYSE:NEM) and Barrick Gold Corp. (NYSE:ABX) will start making profits, good profits, large profits. Through that, I think their share price will come back and then they will turn around and buy juniors that survive this crisis on the cheap to justify those share prices. That’s the basic scenario I’m going by.

TGR: So you say first the bullion itself.

SR: First the bullion itself. You can never go wrong with that.

TGR: Despite the pullback we’ve encountered? Both gold and silver suffered during this asset devaluation.

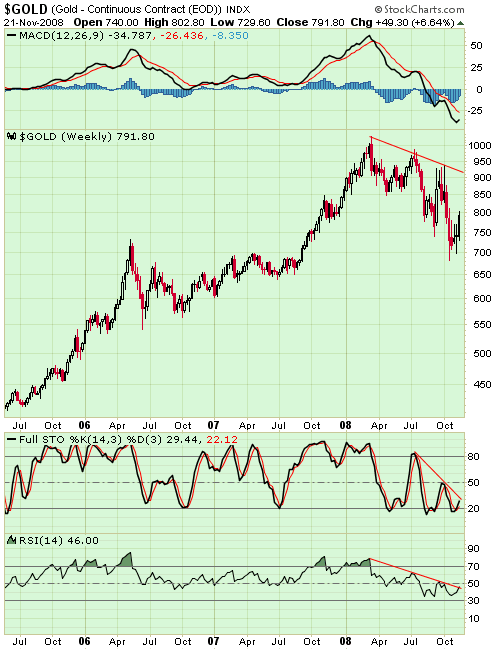

SR: Well, yes and no. In retrospect in a perfect world it would have been wise to sell our gold and silver and their stocks and go into cash and try to buy them later on the cheap. In the real world, it doesn’t work like that. One thing to remember is gold and silver are the only markets that are driven by fear. We saw a good manifestation of that a couple of months ago, when gold shot up $90 in one day. We’ll see more days like that. In fact, it could be tomorrow for all I know, or the day after.

TGR: Do you see a specific catalyst for this?

SR: Not specific. It can be anything—war with Iran; some big banks going under; another country defaulting on its obligations. It can be a major investor like a sovereign wealth fund going to 50% gold or something. It can be absolutely anything. Now the trick here is gold and silver markets are not based on large amounts of buying. Let’s say tomorrow Warren Buffet says he’s going to buy $10 billion worth of gold. Immediately the supply is going to dry up. People who have gold will say, “Wait a minute, we’re not selling. The price is going up.” So the effect of a single event like that in the gold and silver space can reach far beyond what it would in any other market.

It is important to remember you don’t want to be in and out of assets of this type on a whim. Even if it takes a year, even if you have corrections like this, for my investment strategy I do not believe that gold and silver are amenable to buying and selling as are assets in other markets. Better to treat them like insurance, where you have it in good times and bad times. It won’t take a lot of buying to push these metals back up. And even though the metal prices have come down, if anything, demand for gold and silver has increased.

TGR: Evidenced by trying to find some coins.

SR: Absolutely and on any level. A week or two ago I was talking to a gentleman in London who runs a business that basically allows people to invest in gold. He told me that the gold he has in storage for his investors has reached some 11.5 tons in about 2.5 years. This is just one market participant out of who-knows-how-many and he deals mostly with retail investors. I believe the demand is there now and is only going to increase. Our current situation is going to add to that, not subtract from it.

Today’s metals prices are absolutely bogus, as is the price for oil. Yes, you can buy it at that price, but that is not what it’s worth. Right now oil is trading much, much cheaper than water, maybe one-third of the price of water. It should not be possible. I don’t believe in the rational market theory. I think the market is always wrong in the short term.

TGR: If people are looking at rolling money back into investments once the craziness stops, you say a logical sequence is to put some in bullion first and wait a little bit, buy some majors and wait a little bit, and then look at the juniors?

SR: That’s always been the theory. My views have not changed. If you asked me a year ago, I would have told you the exact same thing, so this is not trying to adjust my position based on current developments in the market. But in my opinion, that progression is how the market is going to move forward.

TGR: Doug Casey’s current philosophy is one-third cash, one-third bullion, one-third stocks. Would you agree, or are you saying to get it all in bullion for right now? Let’s say you have a high tolerance for speculation, risk taking. Where would you be?

SR: If you can get bullion at anything close to spot prices, you should buy as much as you plan to buy. I don’t endorse investors paying 50% premium, but I do believe in percentage terms the premiums will shrink at some point.

TGR: So would you buy Central Fund of Canada (AMEX:CEF)? Maybe half physical and half stock?

SR: Yes, I would, absolutely. And as far as stocks are concerned, it goes back to asking yourself that one question: “Is this company going to be around on the other side of this financial crisis?” If it is, by all means, buy some. I would recommend—as always, this is nothing new for me—dollar cost averaging. Whether you want to buy 1,000 shares or 10,000 shares, split it into five or six segments and buy one part every month or so.

The other thing is to reexamine your outlook or your investment horizon. You have to be prepared to not make any money for maybe about three years at least. I’m not saying that’s what’s going to happen, but you have to be prepared for that. Going in, you have to believe in this. I often use marriage as an example. You marry for the rest of your life, even if you end up getting divorced next year.

TGR: Things can change.

SR: Things can change. You can learn things you didn’t know. You may have other factors to deal with that don’t have to do with your position. But ultimately you have to believe in the company or the investment you’re making, and you have to give yourself at least three years to sit on it and maybe take some severe losses.

TGR: Speaking of severe losses, seeing billions evaporate this year has been a humbling experience.

SR: It is and it isn’t.

TGR: Tell us about the “isn’t.” We know about the “is.”

SR: The “isn’t” part is we all knew big problems would be coming down the line. And we knew why. Some of us discussed doomsday scenarios. I think where we went wrong is we did not prepare accordingly. A couple of months ago I wrote an article to that effect. It was called The Trouble with Forecasting. Basically the argument I was making is we knew that things would get bad, really bad. We should have believed our own predictions. There would have been no downside if we had been more conservative, more careful.

TGR: Can you give us any names based on various categories—senior producers, junior producers, exploration?

SR: I can flip that and tell you which companies I own. I own a good position in Pan American Silver Corp. (Nasdaq:PAAS) (TSX:PAA). I own a position in Silver Wheaton Corp. (NYSE:SLW), Hecla Mining. Those three I am comfortable will survive this crisis. One step down in terms of size and presence in the market, I own shares of First Majestic, IMPACT Silver and Minera Andes. Then if you go one step down below from that, companies with no production, I own shares of Esperanza and Silvercrest. I’ll leave it at that. Obviously, I own a lot of other different stocks, but I am trying to protect potential investors so I’m trying to be conservative here.

TGR: Tell us first about the one you mentioned last. What do you like about Silvercrest Mines Inc. (TSX.V:SVL)?

SR: The best thing about Silvercrest is management. And they do have a sizeable deposit, something on the order of 100 million ounces in Mexico. They have advanced studies, including, I believe, a feasibility study. They do need to build a mine. I don’t think it’s going to be an overly expensive mine and they don’t need too much lead time. They probably can be in production sometime in 2010, or maybe even sooner. But management is the key. I did buy that stock at well over $1. It’s probably half that today, maybe lower. But this is the type of company I believe will survive this crisis, come out on the other side and be one of the beneficiaries of whatever turnaround we see.

TGR: Esperanza Silver Corp. (TSX.V:EPZ)?

SR: Esperanza is a similar story. I like the management, very conservative. This is a pure exploration company. They do not plan to be in production, not that I know of. They have discovered two deposits: one in Peru and one in Mexico. I think the deposit in Mexico is about a million ounces of gold. In Peru, which should be roughly three quarters of a million ounces of gold, they have a JV with Silver Standard. That one is a higher grade. This is a grassroots exploration company, they like finding deposits. They found two in the recent past, so I expect more good things from them.

TGR: Minera Andes Inc. (TSX:MAI) (OTCBB:MNEAF)?

SR: Minera Andes is one of the companies that doesn’t have a high profile, but one of my favorites. It’s been my favorite for about five years now. Again, very good management, very low key. They focus on getting things done and not talking big, not too promotional. They have a mine in production that’s joint-ventured with Hochschild Mining (LSE:HOC) (which is a large silver producer) in Argentina. They have another project that they recently put out a resource calculation for—a copper project, which is a joint venture with Xstrata. Xstrata is a very large company, so this is another team that knows how to come up with good assets. I think they’ll also survive this crisis and will benefit from whatever upside in the future.

TGR: What about Minera Andes makes it one of your favorites?

SR: The management. Again, the management is very conservative, very low key, very non-promotional, very down to business. You just get a feeling for people; you see them so many times, talk to them, see how they go about their business and how they deliver. If they get where they plan to get and what they do to get there, it gives you a level of comfort. Minera Andes is one of those that has been through thick and thin and I think they’re definitely out of the woods in terms of whether they’re going to survive.

TGR: IMPACT Silver (TSX.V: IPT). What’s the story there?

SR: I should mention that I am somewhat biased, in that I am a consultant to the company. But on the flip side, I like them for reasons other than that. It’s one of my largest silver holdings. They’re in production in Mexico, very conservative management. They have a good cash position, one of the lowest costs of production. It’s a small producer, at this time. They produce about a million ounces of silver equivalent. But management is seasoned, been around for quite some time and they know how to operate a mine. Their motto is: “a business has to make money, otherwise it’s a hobby”. They bought an old mine in Mexico, and been profitable from day one. They’re still profitable, even in this environment, and I also believe they are going to be one of the ones that will come through this.

TGR: I’ve been hearing a lot about First Majestic (TSX:FR) (PK SHEET:FRMSF).

SR: First Majestic, I think, is one that has the highest chances of surviving this crash or this downturn, however you want to call it. I also think this is one that will get bigger, either through acquisitions or organic growth. I know the gentleman who started this company, Keith Neumeyer, very well, known him for years. Very ambitious and aggressive in executing his business plan. This company should produce on the order of about 5 million ounces of silver equivalent this year, maybe just under that. This has been accomplished in about four years. It’s no small task to get from zero to 5 million ounces in about four years. I also like First Majestic’s other principal, Ramon Davila, who is the most dynamic mining executive I’ve seen by far. He is the one who oversees the operations in Mexico, and is the one who built up Mexican operations for Pan American Silver in the past.

TGR: He’s got experience.

SR: Experience, knowledge and contacts; a very, very successful mining executive. First Majestic is going to be around for quite some time unless, of course, it’s going to be taken over by a major, which would be a compliment to get to a point where you are an attractive target to a major. For juniors that’s often of the ultimate goal. I’m not saying that’s the goal for First Majestic, but it’s like Rick Rule says, you build a company to keep and somebody else will want it. So I think First Majestic is going places.

TGR: And they’ve got the capital to weather the storm.

SR: I believe they have about $26 million in the bank. It’s a well established company in terms of production and operations. They have about 300 million ounces in resources. They’ve done their drilling, they’ve got four mines in production right now. They’re undertaking a major expansion at one of the projects in Northern Mexico. They’re basically going about their business according to plan. Maybe they’re making some minor adjustments to cut costs here and there, but ultimately this company is going to grow.

TGR: What’s going on with Hecla Mining Company (NYSE:HL)? Is it just silver and the industrial metal and, therefore, demand is off and prices are off?

SR: All of the above, but I think one of the reasons that is not well understood is that Hecla is one of the very few companies in this space that’s listed on the New York Stock Exchange. So it’s one of the more visible ones and I think they take it on the chin harder than the rest, particularly because of that listing. The way mainstream investors work is, “Everything is going down, so let’s short commodities. What do we have to play with?” And Hecla inevitably pops up on that list. I think that’s part of the reason it’s been beaten down so badly. Hecla is one of the best underground mine operators, so I think they will survive. The company’s been around for 100 years, so I’m sure they can weather this one—at least that’s the way I’m betting. If I’m wrong, then so be it.

This is why I am reluctant to discuss specific companies. If you’re investing in the mining sector, you have to be prepared to make mistakes and you will definitely make mistakes in many of them. The question is, of course, in the grand scheme of things, are you making progress or not, are you making money or not. So long as your portfolio is growing, you could do much, much worse than Hecla.

TGR: Wouldn’t you think the darling of the sector would hold up better?

SR: It works both ways. It would have been darling in good times and I think it will be again. At some point they will benefit from that New York Stock Exchange listing. But in bad times, they take it on the chin harder than the rest.

TGR: Another company that’s getting some conversation is Silver Recycling Company(TSX.V:TSR), which is a different play than mining. What do you know about them?

SR: Silver Recycling has been another favorite of mine. The businesses they currently control are profitable and they’re still doing okay. This has been one of the attractions when we first looked at it. Unfortunately, they’ve been one of the victims of the current credit environment. While they do have self-sustaining operations, they need to raise capital to make acquisitions. If they are successful in that task, and I have to believe they will be, it’s going to be a very, very pleasant surprise. It’s beaten down with the rest of the sector right now, but the business plan is sound. I am still optimistic about this company. In fact, I’m trying to help them get through this. By the way, chances are you can buy some silver from them because they’ve responded to the market demand and produce 100-ounce silver bars and silver rounds, which they sell to investors.

TGR: Right. At a premium to spot, right?

SR: Yes, at a premium to spot, I bought some myself, so I don’t think the premiums are outrageous at all or out of line with the market.

Not all of Sean Rakhimov’s dot-com dabblings paid off, with at least one important exception. He traces his interested in financial markets to that era, when he joined a software development company in 1996. In the years that followed, he designed financial systems to support different areas of the investment banking business. He seized the opportunity to learn about options trading, securities lending, payments processing, clearing and settlement, fixed income securities and margin transactions. He’s not only been putting those learnings to work ever since, but also sharing them with others, with writings published on such internet portals as Le Metropole Café, 321Gold.com, SilverMiners.com and—of course—The Gold Report. Sean, who has been involved in a number of research projects for renowned silver guru and newsletter writer David Morgan, now publishes and edits his own website, SilverStrategies.com.

")

")