Gold Report: investment coverage of gold and other precious metals (free newsletter emailed semi-weekly)

Jon Nadler: Where Might Gold Go?

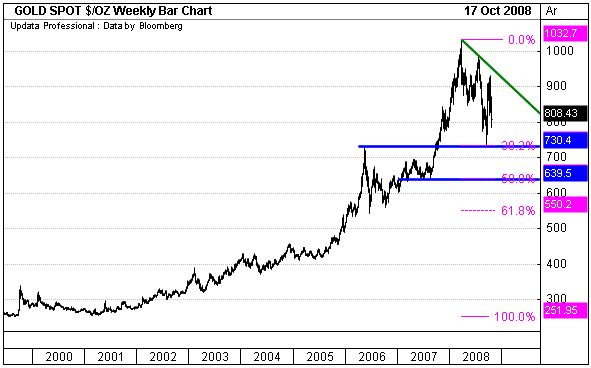

Source: The Gold Report 10/24/2008

Jon Nadler, Kitco’s well-known senior investment products analyst, elicits both criticism and acclaim for opinions that some characterize as contrarian. In this installment of an exclusive interview with The Gold Report, he brings his three decades of experience to bear (no pun intended) on the outlook for gold, promoting the precious metal as a key asset in a balanced portfolio, as well as for its intrinsic value and “insurance” attributes.

The Gold Report: Economic theory tells us gold should be taking off, given all the uncertainty in the marketplace. But we haven’t seen that happen. What is going on?

Jon Nadler: Well, as you may have heard, even Alan Greenspan found a glitch in his formerly “reliable” economic models during this crisis. Gold certainly will continue to have its volatile days, but the bigger trend is probably more important overall. To a certain extent, the metal got ahead of itself as a legacy of the huge infusion of speculative fund money that came into the commodities complex as a whole, and of course gold is part of that, aside from its role as money. This phenomenon goes back at least two years.

It accelerated last September when the Fed first started to cut rates, and then we got into a position between March and July where the ever-weakening U.S. dollar started things looking like a bubble of major proportion—not just in gold, but in most industrial metals and in oil. It got to the point where oil became so visible that regulators started making all sorts of unpleasant noises toward speculators.

So we saw the exodus from the commodities complex of a good part of that hot money from hedge funds. Of maybe $300 billion that had come in, we don’t quite know how much got up and left. We certainly know that some $50 billion left oil, which had close to $60 billion in it. That’s a significant proportion just sucked out of those markets. Of course, prices collapsed in the wake of that, along with the credit crisis unfolding on the front burner. That piece of the puzzle really didn’t become visible untila few weeks ago, whereas the exit of hedge funds from commodities was well underway back in late June.

TGR: Are we now out of that exit phase?

JN: I think it is continuing because some of the funds simply failed, like Ospraie just last month. Ospraie had a lot of bad bets in oil and gas contracts. We see others with stock positions being wiped out in this debacle. If you have profitable positions in gold or oil, you’re going to be forced to sell them to raise cash to meet your equity margin call. To some degree, that continues. It has wiped some $200 off the gold price in the last 30 days alone.

TGR: If hedge funds and speculators are still exiting, when do you see that flushing itself through and gold reacting more as one would expect, given the financial turmoil?

JN: We may not see that for some time. If deflationary pressures really take hold, we may have a case of “reverse hedge” developing, whereby gold might still fall to the mid-$600s or even as low as the low $500s, but still fall less in percentage terms than other assets might. In that case, investors would still be better off holding some gold and lots of cash rather than equities or real estate and such. Hopefully we don’t head into that deflationary spiral because that could hurt a lot of higher-priced producers of gold. Certainly a lot of the mining companies would have to reconsider what projects to mothball if that happens.

If we don’t go into that vortex and confidence returns by whatever means, things could stabilize. Stability in gold would imply a trading range between $650 and $850. It’s definitely a blow to the doomsday newsletter writers, who thought the circumstances we are seeing now were the ideal scenarios they’d dreamt of as far back as we can recall. They know, however, that the world of $2,000 gold is not one they would want to live in.

The fact that in July gold had trouble surpassing $930, (not even matching the March highs when Bear Stearns failed), was definitely a big wake-up call as to what was going on. And of course what’s going on is that a lot of people had already bought gold starting at $252 and all the way up to $400 and $600. When this big crisis hit, if they spotted their 401(k) accounts off by 38% and their gold holdings ahead by 50% or 60% or much more, it wasn’t a hard decision to make. They liquidated that which was profitable in order to mitigate their losses. That’s why they’d bought their gold to begin with.

So the latecomers, those who were rushing in, having put off their gold purchases until it became a burning issue, basically got caught trying to buy into this “runaway train” scenario. The few people who tried cost-averaging higher-level purchases of $900 to $1,000-plus were the freshest of buyers during these past couple of weeks. The difference we spotted in retail transaction patterns is that this particular cycle in the gold market brought out quite a few sellers, along with new buyers. So there’s very good two-way activity going on in the physical market.

TGR: The gold bullion coins appear to have a very high premium over the gold spot price, so there still seems to be some fear out there, or is it shortages?

JN: Some issues in the physical market are really grossly misinterpreted. Observers are not doing anyone any favors. My perception is that we have a contingent of pundits who are extremely panicked that this is a very poor reaction by gold to the crisis, and it will make them look bad. It already has. Now they’re trying to manufacture this global stampede into gold by panicking investors and by scaring them with stories of supplies running out. No one will argue that there are higher levels of individual investor interest, but it’s nothing “unprecedented.” They’re trying to make it out as unprecedented, and that’s simply not the case. Perhaps it says more about how short a time such pundits have spent in these markets.

TGR: Just how real is the shortage in coins, then?

JN: Specifically, what’s going on with the coins is that most of the mints of the world do not operate on a “produce-then-wait-and-see” basis. They don’t pre-mint hundreds of thousands of coins and put them on the shelf waiting for buyers to materialize. They basically operate on a mint-to-demand policy.

Because of the prolonged bear market in the ’80s and ’90s, most of them had slimmed down to bare essentials and, in fact, a lot farm out some components of the coin manufacturing process, such as blanking. The U.S. Mint is one of them. They ran into some blank coin quality problems in silver back in March, with about half a million silver blank rejects. That put them behind the production schedules, and when demand indeed kicked in for physical small coins, they were unable to fulfill commitments on a timely basis. This does not mean they ceased production. In fact, most of these mints consider small-item production quite profitable, which implies that they have added shifts, are finding new suppliers of blanks and new refiners for material, and augmenting production to meet the demand. Inventory build-up is one of their top current priorities.

Look back in recent history at the classical gold rushes, if you will. During the first one, in that inflationary period in the late ’70s and early ’80s, some 16 million Krugerrands were sold globally. The market events of 1987 brought on the next wave of buying, and that is when the U.S. Mint sold more than 1.25 million ounces of gold. Nor should we lose sight of the fact that in the ’91 recession, just a few short years later, they only sold a quarter million ounces. And then we go to about 1999 before Y2K. Again, they suspended sales of certain products like silver rounds, which were being hoarded by people expecting the end of the world. Next would be May of 2006, with the North Korean and Iranian political tensions. Again, very good robust sales, but nothing of the magnitude of ’80 or ’87, and similar to what we’ve had since last year. But at best, I think this year the U.S. Mint will sell about 750,000 or 800,000 ounces. It’s not the level of 1987’s stampede or panic, so I don’t see why they’re trying to make it out to be something bigger than it is.

TGR: Why is there such a premium, though? Just because they’re undersupplied?

JN: Yes, once the retail shops saw the Mint selling coins on an allocation basis, with some restrictions to build up inventories, the retailers started raising premiums on coins that they couldn’t basically get to fulfill previously sold orders. They raised their bids; they also raised their offer. It’s really limited to items like the silver rounds and some of the smaller fractional coins.

But in terms of Kitco getting supplies, basically we took the attitude that if we could not get a commitment from our distributors and suppliers as to a firm premium and/or a delivery date or both, we simply removed the items from the order pages in the online store. Those order pages are limited to items we are confident we can deliver at a decent price within a decent number of days. I know that the list is looking pretty slim, but we do have product to sell, and our pool accounts have never had any shortage of underlying material to secure; namely, 1,000-ounce bars of silver and 400-ounce bars of gold. We continue to offset 100% of all pool account purchases for the peace of mind of our clients.

And we’re adding back a lot of the items that had been removed. For instance, we just got several tens of thousands in gold coins and about a quarter million in silver coins from the Royal Canadian Mint. We’re getting Austrian gold and silver coins in very soon, and I’m sure that the U.S. will restart its sales to distributors once they switch dates on the coins to 2009. This is, coincidentally, the period when mints cease producing old (current year) dating and start with the new ones, and the switchover generally creates a bit of a glitch, too. At any rate, there will be product. We have eggs, thus we will have the omelet as well.

TGR: So it would be prudent to wait a bit.

JN: Absolutely. People are not good consumers if they go out and pay $5 over spot on $10.50 silver just to secure something that they think they’re going to have to barter at the grocery store. First of all, that likelihood is not there. Second, the liquidity of such items for such a situation would be questionable. When the supplies do come out, they will be priced at the previous norm. The Mint is not selling the New Olympic Silver Maple Leaf at more than the $1.50 they normally charge. That means they shouldn’t retail for more than $2.50 anyway. If people want to go on eBay and pay $5—well, as I said, try to be a good consumer.

Another thing some of our clients have done is that if they like a particular price that gold or silver reaches on a given day, they simply lock in that price and buy ounces of gold or silver in the Kitco or Royal Canadian Mint pool accounts, and then plan to take advantage of a conversion to physical coins or bars when their supplies and premiums return to earth. It could be just a matter of a few weeks overall.

TGR: Earlier you suggested that in a deflationary period or one just slightly inflationary, gold might be somewhere in the $500-$600 range. But over the longer term, you think it is more likely to stabilize somewhere between $650 and $850?

JN: I think that’s what we’re looking at in order to reflect current levels of supply and demand, basically make the mining community reasonably happy and keep India buying, which it’s currently not. Anything over $850 is just too much as far as they’re concerned, and they’ve demonstrated that stance for most of this year.

We’re in Indian Festival season and they’re lamenting about very poor sales. We just learned in mid-October, for instance, that the World Gold Council is apprehensive about sales levels of bullion in India, the largest consuming nation of the metal. Not only did they change their gold promotion campaign roughly in June or July, the campaign was switched to something very emotional, with raw appeal to long-standing cultural concepts. They really came down to the nitty-gritty to remind Indians that this is part of their cultural and spiritual life. The previous campaign had a happy, luxurious, light-hearted approach.

But more than that, they launched a program whereby people can actually buy gold coins through India’s post offices. It’s a huge distribution network, particularly well-suited to sales in very small increments, such as one‑gram or five‑gram coins. They recognize that urban buyers are not very gold-friendly anymore and that rural buyers continue to be the ones looking at gold as an alternate form of savings.

So your little one‑gram coin for $30 or so provides direct access to a lot of people. It’s a brilliant marketing scheme in terms of convincing the refiners to make small material. I think in part that’s one of the things that delayed supplies from Valcambi, one of the refiners in Switzerland, which is probably trying to focus on ramping up to send a gazillion one‑gram coins throughout India. Let’s see how it’s received; hopefully all these little grams will add up to something real in terms of overall tonnage. So far, the 800 or 900 or 1,000 tons that experts estimated for India to take from the market this year is definitely not there. It wasn’t there last year; it’s not there this year.

TGR: Any other significant factors at play in that scenario?

JN: Investment demand, robust as it may have been, has really been competing with a fairly healthy supply of scrap metal from secondary sources. In fact, last year it ended up almost a wash, where scrap suddenly had amounted to 1,000 tons in the market and investment was about 1,200 tons. So again, at high prices, gold finds its way into the market and we haven’t seen this sort of global man-in-the-street stampede to gold. It’s still competing with cash at this point, where people are really nervous about what they do with the money they take out of the bank.

TGR: Given that, if we’re looking at gold as insurance against the financial markets and cash, why wouldn’t gold go up? Why would it stabilize around $650 to $850?

JN: By and large it has already proven its insurance attributes by virtue of the fact that it outperformed the S&P just sitting around stable. It basically functions that way. If it stays in the $845 and $945 range, as it has this year—the overshoot was a blip—maintenance of these levels has already enabled those who hold some percentage of gold to mitigate the under-performance of the S&P and the Dow and everything else in their mutual funds. In that sense, it’s certainly done its job.

Gold doesn’t need to go to $1,200 or $2,200, as all of the doomsayers were saying, to prove itself. That would be more like proof that something has gone extraordinarily wrong in the global system and it’s a scenario you really don’t want to wish for. Should it come to that, you can pretty much be assured that other assets have totally vanished—not just a major damage hit, but you can write them off. That’s not desirable and the G7 and G12 seem prepared to do anything at their disposal to prevent a scenario where you would see both the Dow and gold at $4,000. That’s not what people are gearing up for, obviously, considering the social disruption and violence and all that it might engender. So stability is preferable.

Yes, I think some things are not going to go smoothly. There will be more pain, and more banks will still fail, and you will have occasional runs and blips where gold takes off out of the gate, but the bigger picture really says that this is about it. There’s no valid reason for it to really go up much, much, higher because a lot of the pressure now is on the deflationary side. With all the money that’s been thrown into the system, there are many people expecting a Weimar Republic-style hyper-inflation to become the necessary result. However, as in many previous instances, a lot of this excess liquidity is expected to be mopped up out of the system on an orderly basis when things stabilize.

Among the unknowns, of course, are the effects of de facto partial bank nationalization by the U.S., and issues such as which types of participants will be able to play in the commodity markets, and to what extent. Reading between the lines of what Bernanke said in mid-October, it’s pretty clear that they don’t intend to have asset bubbles going forward because of the pain involved in deflating these bubbles. So I think values will not be allowed to get out of hand once again. I’m not talking about gold price suppression here. Far from it. I’m just saying that asset bubbles in general that make for these kind of outcomes probably will be regulated away, or at least in large part.

TGR: So do you see anything pleasant on the horizon?

JN: Not exactly. We can expect another two years of real turmoil in terms of difficulties in GDP and retail sales, and consumer spending. It’s going to be a difficult proposition for the industrial metals to make a good go of it—silver, platinum, palladium—because their primary users are: a) unable to get credit or b) scaling back production on lower expectations of demand or c) like the automakers, who are at best, willing to buy only a little bit for inventory because they still have unsold inventory to address first. We’ve seen copper take a big hit, just based on global demand destruction expectations. Same with oil, which is definitely reflecting the same demand versus supply situation.

TGR: Gold is something that can react on fear. Do you anticipate fear to drive it up?

JN: The way to avoid that is probably to not be focused so much on price performance, because most people ought to be buying gold as the allocation device that it really is, and then mobilize it only when absolutely needed, rather than buying because they think they’ll “make money.” That’s not in the cards, really. If you try to trade these markets, you get chopped up. We’ve seen that clearly. Anybody who has tried to trade these gold markets recently was just chewed up and spat out. It was impossible. When you have to stand in the way of these runaway trains that fund liquidations present, or one-off stampedes that some other funds might present on a given day when they set their mind to buying, that’s just not going to work for the smaller trader. The long-term 10% life-insurance type of allocation is the key here for many.

TGR: What’s your thinking about the U.S. dollar these days?

JN: The dollar still has surprises left in it, obviously, because everybody had called for its demise about a year ago. By March they had also buried it and sang its last rites. And sure enough, after July when push came to shove, a lot of people said, “You know what, okay, I’ll sit on dollars.” And there you had your shortage of dollars.

Not everything is fathomable today. We have elections in the U.S. in November, which could mean some interesting change in the national psyche as to which way we go forward, what programs get put into place, who’s the new Fed chairman or Treasury boss. A lot of questions are still unanswered. One of the fundamentals—one that readers shouldn’t ignore—is that whatever the government has put into motion in recent weeks may take upwards of 14 months to really show up. People expect instant gratification, and part of the wild swings is just frustration. “Where is the immediate result? How come we’re not roaring ahead?” These are not easy-going, fast-result types of processes.

TGR: You offer a logical, level-headed perspective that should be of some comfort to our readers in these highly emotional times.

JN: If I tried to convince you that it’s a one-way street and it can only go that way and buy now, beat the rush, two years from now you might not want to talk to me. I would have lost credibility. It’s not about being right on price forecasts, although I don’t think I’m too far off on those either. It’s not about making hype out of it; at the end of the day that’s really going to smell like you have an agenda. It’s more about seeing what’s going on in the underlying market and gauging the consumers’ pulse.

Jon Nadler, an oft-quoted industry spokesman in financial media worldwide, is Senior Investment Products Analyst for Kitco Bullion Dealers. Jon has devoted some 30 years to the precious metals market and on its related investment products. A graduate of UCLA, he established and ran precious metals operations at major financial institutions (Deak-Perera, Republic National Bank, and Bank of America) and has consulted on marketing and product development issues to government mints, precious metals retailers, and trade and membership organizations such as the World Gold Council.

Who knew you could auction real diamonds much like you could sell your stamp collection on eBay?

Who knew you could auction real diamonds much like you could sell your stamp collection on eBay?

this is interesting… really cool idea, but in order to work the power houses have to buy in….

I wonder if I can by a CDO on this badboy — collateralized deadpool obligation

jk, actually right now diamonds are priced per the rappaport report or some bs like that.

the only problem is that a lot of jewelers base the pricing that they can acquire a diamond for a customer off that report and the cost is known when the customer is there. If there is an auction, the price is up in the air for two days.

Can they be easily traded like stocks? Also who would verify the quality?

Yup, traded just like stocks, or more like gold actually (try the demo).

“All diamonds published on the DODAQ platform have first been graded by a recognised gemological grading laboratory and are received with their original certificates into the DODAQ vault.”

Riiiight.

Either the people behind this idea don’t really understand how diamonds are graded and traded in the real world, or they are hoping you don’t really understand how diamonds are graded and traded in the real world.

I’m betting the latter.

Haven’t you seen the blood diamonds movie dude? …diamonds suck

en.wikipedia.org/wiki/Blood_diamonds

its unlikely anyone’s going to overthrow debeers, but they can try

rankmaniac

What a nice video

As developers of the promo, I can tell you this is an incredible application. I’ve seen it in clear cut action, so to speak and it’s going to cut a swathe through the diamond trade.

Congrats to Simon & team at Dodaq.

Next: put/call options on diamonds

I hope the guys at DODAQ have bullet-proof cars and 24/7 secuirty escorts for their families. The cartel does not like upstarts like this.

At first I was apprehensive that such a thing could even be done but on closer inspection, having used the site, this looks like it could really change things – ultimately for the better. Fascinating stuff. I look forward to reading more.

This will certainly be interesting. The diamond world isn’t used to startups of any kind. Not in the least, something like this.

As a financial instrument, why not trade diamonds like any other commodity? But, if you are choosing just ONE diamond for your fiancee, I highly recommend seeing a stone in person. Any gemologist will tell you that no two stones are ever the same, and that each has its own “fingerprint” and will handle light refraction differently. There are 57 angles to a diamond, and each stone is cut slightly differently, according to the natural growth of its crystals.

Two stones of the same 4 C’s can produce very different effects of light and sparkle. This is a subtlety that is often times lost when people compare diamonds, site unseen, and assume the 4 C’s tell the whole story. But when you put the two stones next to each other, you might be surprised at how obvious of a difference there could be.

It’s very helpful to categorize diamonds with the 4 C’s, but as you can imagine, a 10 minute crash course in the 4 C’s can’t replace a lifetime of experience in diamonds. It’s the same in any industry, where reading a wikipedia article on something doesn’t make you a real expert. You’ll have solid footing, though, and that’s a good start.