Tags

agricultural commodities, alternate energy, Austrian school, banking crisis, banks, bear market, Bollinger Bands, bull market, capitalism, central banks, China, Comex, commodities, communism, Copper, Currencies, currency, deflation, depression, diamonds, dollar denominated, dollar denominated investments, economic, economic trends, economy, financial, Forex, futures, futures markets, gold, gold miners, hard assets, heating oil, India, inflation, investments, Keith Fitz-Gerald, market crash, Markets, mining companies, Moving Averages, natural gas, oil, palladium, Peter Schiff, physical gold, platinum, platinum miners, precious metals, price, price manipulation, prices, producers, production, protection, rare earth metals, recession, risk, run on banks, safety, Saudi Arabia, Sean Rakhimov, silver, silver miners, socialism, sovereign, spot, spot price, stagflation, Technical Analysis, timber, U.S. Dollar, volatility, warrants, Water

As I make this post Gold is up another $20/oz this morning. As mentioned in yesterdays post this does not bode well for the “short sellers” in the Gold market especially if traders start taking physical delivery off Comex. Is this the beginning of the Short Squeeze? Only time will tell, but I find it very interesting that Gold is continuing to rise as we approach the end of the Dec. contracts. In addition with the Fed’s latest round of intrest rate cuts which show its’ resolve to keep deflation from occuring and to free up the credit markets, Of course long term this will spell inflation even hyper-inflation, which in turn makes Gold in any form the obvious investment choice. Personally I am looking to increase my positions in many of the mid-tier and juniors in the gold mining sector, These companies even with the recent move in Gold are still trading at extremely low levels, and many are trading below book value! Here are some excellent articles for you today, ENJOY and Buy Precious Metals! Your children and grandchildren will thank you! – jschulmansr

Jeffrey Christian: Foreseeing Bright Days for Metals – Seeking Alpha

By: Jeffrey Christian of The Gold Report

A foremost authority on the precious metals markets and a leading expert on commodities markets, CPM Group founder and Managing Director Jeffrey Christian brings some holiday cheer to The Gold Report readers. In this exclusive interview, he debunks doomsayers who await the dollar’s demise, anticipates what may well be a more powerful recovery from recession than most pundits do and foresees bright days for gold, silver, PGMs and specialty metals.

The Gold Report: Perhaps you could begin by giving us your macro overview of the world economy and the outlook as you see it.

Jeffrey Christian: If you go back to 2006 or 2007, our view had been that we would see a relatively short and shallow recession in the first half of 2009. Beginning in late 2007, we said maybe the recession would start earlier, maybe in the fourth quarter of 2008. And then we said maybe the third quarter of 2008. Now we find from the National Bureau of Economic Research that the recession officially started in December of 2007.

We still see it ending around the middle of 2009. But it’s obviously going to be much longer and much deeper than we had expected a year or two ago. Economic problems are much worse. What we really have is a financial crisis, a freezing up of credit availability, which has led to a domino effect of reducing demand for products. We started with a bank panic and a freeze-up in the credit market that has now spilled over into final demand for goods and services across the real economy. It’s proving extremely difficult to treat. I happen to think that the U.S. government policies pursued in September, October and November have not necessarily been the best policies to resolve these issues. We’re looking to see what the new government does after January; a different approach may be more palliative to the economy.

But the bottom line for the overall economy is things are bad, they probably will get a little bit worse, and we’re probably looking at a pretty weak first half of 2009. Our view is that by the second half of 2009, maybe early 2010, you’ll see an economic recovery come along. That economic recovery may be a lot more powerful on the upside than a lot of people expect. One of the things that we’ve seen and have written extensively about over the last few years—and it’s become even more prominent with the government largesse—is an enormous amount of money sitting in cash and cash equivalents waiting for a signal that it’s safe to invest again. All of this money is standing by, ready to invest in precious metals, invest in commodities, invest in real estate, equities and corporate debt. So we think that in the second half of 2009, or whenever the recession ends, you could see a rather rapid recovery in overall economic activity globally.

So that’s our economic overview. I will say this. Everybody in the world is looking at the amount of money the governments have pumped into the market, saying it spells death and destruction for the U.S. dollar and inevitably will lead to hyperinflation. I’m not convinced that’s true and I think that’s a very important point. When you look at all of the monetary liquefaction that’s occurred, it’s definitely going to lead to a lower dollar and higher inflation than we’ve seen over the last 25 years. Still, we may well avoid a total collapse of the dollar and hyperinflation if the monetary authorities of the world effectively are able to sterilize the inflationary implications of this once the recovery starts. We won’t know that for a year or so.

TGR: What do you mean by “sterilize the inflationary implications”?

JC: It means suck the inflationary money creation out of the economy. I’ve spent a lot of time looking at what happened in the period of 1979 to 1983; the really critical point here is in the middle of 1982 we were two years into a double dip recession. At the time it was the deepest recession in the post-war experience. In the middle of 1982, Brazil, Argentina and Mexico were about to default on their government bonds. Paul Volcker called the central bankers of the world together and said, “We have to monetize ourselves out of this recession because it’s about to become something much deeper and harder to solve.”

The governments of the world opened the sluices and flooded the world with money. By December of 1982, the world was out of a recession, auto sales had rebound sharply, Geoffrey Moore’s leading index of inflation indicators, which was basically money supply, had gone off the chart. Gold had risen from $290 in July of 1982 to $500 by the end of the year because everybody was convinced that this was going to be inflationary and that the dollar was going to collapse. By the end of ’82, early ’83, it was clear that we were out of the recession.

Fortunately for Volcker, Reagan (Ronald) and an associate named Regan (Donald Regan, Reagan’s Treasury Secretary) had taken a $40 billion Carter (Jimmy) deficit and turned it into a $200 billion Reagan deficit and needed to finance it. So Volcker said, “That’s easy; Let’s sell $300 billion worth of T-bonds and suck $300 billion out of the economy.” And they did it. So they started selling a tremendous amount of bonds to monetize the debt that the government was racking up and thus sterilized the inflationary implications of their earlier monetary creation.

Then oil prices fell 15% in the first quarter of 1983, from $34 to $29 per barrel, gold prices fell $100, inflation went from about 7% to 3% and is only now getting back up there. We entered a 25-year period of the lowest inflation in a long, long time right when everybody was convinced that all of that money creation would lead to hyperinflation. The government has followed that model every time we’ve gone into a financial crisis since 1982. This time around everything is much bigger and the question is, “Can they do it again on an even grander scale?”

TGR: We didn’t have the fundamental problems back then that we have today. We didn’t have all these derivatives. So many things are so different, and we’ve seen nothing of this magnitude.

JC: Actually, the two biggest and most important differences are that we had extremely high U.S. interest rates then, and a very strong and persistently rising dollar. The dollar was rising then, as it is now, but it has been weak from 2003 until the middle of this year. You’re right—we didn’t have the derivatives and all of this enormous financial liquidity that we have now. And as I said, we’re playing a much higher-stakes game this time around and we’re doing it in a situation with low interest rates and a fundamentally weak dollar. People talk about how strong the dollar has been in the last few months, but it’s still very low compared to what it had been.

Funny, I just got an email from someone who attended a conference I spoke at in Zurich about a year ago. He said this is amazing, that a year ago everybody laughed at me because I said the dollar would be strengthening—but I didn’t say what kind of environment it would be strengthening in.

TGR: Isn’t another difference between the current situation and the one 30 years ago the fact that back in ’79 it was basically the U.S. and the Banana Republics that were having problems? It wasn’t Germany, France, Switzerland—it wasn’t everybody, was it?

JC: No. It was everybody. The U.S. was in a deep recession, Europe was in a deep recession. That’s when they coined the term “Eurosclerosis.” I was at J. Aron at the time and we were doing a lot of gold loans with Eastern European governments, because they needed the money. We found ourselves in workout situations with sovereign debt in Eastern Europe in 1981; whereas Latin America didn’t erupt until 1982. But it was pretty much universal. The U.S. was a bigger part of the world economy back then, too.

TGR: So a decoupling, when you look at the BRIC countries, will help carry us through or avoid an international recession this time around?

JC: I don’t think so. I think we’re in an international recession. The IMF seems to think so. When everybody started talking about how the economies of the world could decouple from the U.S., I said it’s just one of those pater nosters that makes no sense and doesn’t stand up to statistical scrutiny. You’re seeing that. You’re seeing India, China, and all of the other emerging countries really suffering from a decline in demand for their products, much of which are exported into the United States and Europe, and it’s having catastrophic consequences. Granted, there is a movement away from being dependent on the American consumer on a worldwide basis, but it’s a very slow movement and hasn’t progressed far enough to insulate the rest of the world from the problems in the U.S.

TGR: You were talking about Volcker, who issued something like $300 billion of debt—Treasuries— in the ’80s and sold them to cover it and continued to do more of that. At some point, don’t we have to pay that back? Isn’t there a Piper to be paid?

JC: In theory, yes. But there’s a problem with the doomsayers. Look at Jim Grant, who publishes the Interest Rate Observer. I think it was in 1980 that he said, “Oh, my God, look at this $37 billion debt that Carter’s ramping up. This is unsustainable; the Treasury market is going to collapse.” At some point, he probably will be right and the Treasury market will collapse. But in the meantime, we’ve had 28 years that make a $37 billion deficit pale. We wish we could have a $37 billion deficit.

In the meantime, several things mitigate against any imminent collapse. One is the fact that the world economy basically always has been and always will be a giant confidence game, in the sense that there has to be a certain level of confidence to keep things going. The other thing is that for the dollar to collapse, some other currency has to rise very sharply. The problem that the world’s in right now is that for the dollar to fall sharply, investors have to have greater confidence in some other currency. This is really great for gold. It makes you really bullish for gold. Another currency has to rise if the dollar’s going to fall. Ask people “Which one do you have more confidence in?” There’s silence in the room and then people buy gold. No one has any confidence in any of the other currencies or the governments behind them—the Euro, the Yen, the Swiss Franc or anything else.

In a speech a few weeks ago, I said, “The dollar is like your mother. You’ll sit around and complain about her and how she’s so mean and nasty and you’ve got to get away from her. But as soon as you cut your knee, you go running back to her crying.” That’s what’s happening right now in the world economy, in the financial markets. Everybody has been saying for five years that the dollar is toast and the dollar is no good and the U.S. debt is unsustainable. But as soon as you get into a banking panic, everybody converts their money into dollars and Treasuries and CDs held by banks that are guaranteed by the FDIC. Why? Because even though we’ve lost a tremendous amount of faith in the U.S. Treasury, we still have more faith in the U.S. Treasury than we do in, say, the European Central Bank or the Bank of Japan or the Bank of England.

TGR: So if the dollar devalues and some other currency has to rise, it bodes really well for gold. But considering the trillions of dollars of debt out there, is there enough gold for it to be a viable alternative currency? Or will the price for every ounce of gold become something cataclysmic like $3,000 or $4,000?

JC: Yes. If you tried to monetize the debt in gold, or if you tried to go back to a rigid gold standard, you would either have to have $3,000 or $4,000 or $5,000 or $6,000 gold, or you would have to severely contract the world economy back to where we were in, say, the 17th century. But I don’t think that’s what you’re looking at. Rather, you’re looking at some portion of the world’s assets moving into gold as an alternative to currencies. In that situation, you “only” see $1,000 or $2,000 gold.

TGR: Some of us might like $5,000 or $6,000 gold, but maybe not everything else that would be going on with gold prices at that level.

JC: Right. You definitely wouldn’t like everything else going on. It’s interesting. It depends on how a gold standard would be created. The last time we had a “serious” discussion of a gold standard in the United States was during 1980 election campaign. The Republicans actually had a platform plank written by Arthur Laffer to return to a gold standard. What Laffer said was that for the U.S. Treasury notes in circulation, you would have to have 40% of the value of the Treasury notes in gold held by the U.S. Treasury, or a 40% cover. It sounded really stringent, but then you realized that since the 1960s almost all of the bills printed actually had been Federal Reserve notes—not Treasury notes. When asked about that, Laffer said that’s right. What you need from a gold standard is the public’s sense of confidence in it. If you tell them Treasury notes are backed by gold, they’ll be more confident in the value of the dollar. They won’t bother looking at the fact that we’re printing Federal Reserve notes ’til the cows come home. It was a very disingenuous and cynical approach to the American voters.

TGR: So we may see some rush to gold, which may lift it up to $1,000 or $2,000. What about other precious metals like silver? Will that tail along with gold?

JC: I’m actually now in a situation where I like silver, platinum, palladium and the other platinum group metals as well as gold. I like silver for a couple of reasons. One is it’s a financial asset like gold, it is benefiting from the move of investors into silver and gold, and it will continue to benefit from that. But you’ll also see several other things. First off, there is not a lot of metal in the silver market, half a billion ounces in bullion and maybe a half a billion ounces in bullion coins. In gold you have a billion-plus ounces that investors own and another 980 million ounces that central banks own. There aren’t those large enormous stockpiles of silver if you’re looking at it on a dollar value basis. In addition, silver is an industrial metal with some very interesting new uses coming up. It’s losing some of its traditional uses such as photography; but in other uses, such as batteries and electronics, it’s actually growing very sharply and could grow more sharply over the next few years. So I think silver’s got a lot of good things going for it. It’s an alternative financial asset like gold. It’s a smaller, less liquid, more volatile market than gold. And it has the industrial base that gold doesn’t have. So I like silver for those three reasons.

TGR: What brought silver down so much? It got up to $21; now we’re at $9 and change.

JC: The massive amount of leveraged investment in these things has brought all of these metals down. Everybody keeps talking about de-leveraging, but if you ask them to explain it, they can’t. But let me try to explain what I mean when I say leveraged investment. You had hundreds of billions of dollars of institutional money invested in gold and silver forwards, gold and silver over-the-counter options, and gold and silver indexed notes—all written by banks and all with major leverage factors. Some were 10:1; some of them were actually 30:1 or 40:1. As the financial crisis occurred, institutional investors had their credit lines pulled back. Consequently, they had to reduce the amount of investments that they’d borrowed money to make. So a hedge fund that has $10 billion under management and a leverage factor of 20 might have $200 billion of leveraged trades. Then suddenly you don’t have the money to support $200 billion worth of leveraged trades. You have to liquidate most of them because you really only have $10 billion—which is going down in value fast. So there’s been this massive sale of leveraged products. It’s like running for the exit in a theater when somebody yells fire. It’s a very small door, a very illiquid market, and all of a sudden there’s no provision of credit. Everybody’s trying to get rid of their leveraged exposure all at once and these prices have just plunged down. That’s really what it’s been.

TGR: But silver has lost nearly half, while gold is down less.

JC: Silver prices are always more volatile than gold prices. That’s just a fact of life. It has to do with the fact that the silver market is about one-twelfth the size in dollar terms. The other thing is that gold is money and silver is like money. Silver has this schizophrenic personality. It is an industrial commodity, but it’s also a financial asset and you do see more people investing in gold than in silver worldwide right now. As the prices plunged, you have seen an unprecedented volume of physical gold and silver being purchased by investors around the world. So you have this dichotomy, where the price is being hammered down by de-leveraging in the paper market, while people—in some cases the same people—are taking what’s left of their chips and putting them into physical gold. One of the things I think you will see going forward over the next many years is a lot of institutional investors, including sovereign wealth funds and government funds, wanting exposure to gold and silver but not on a leveraged basis where they’re really owning IOUs issued by major banks. They are wanting the physical material.

TGR: Does that hold true for retail investors too? So rather than buying ETFs or Central Fund of Canada (AMEX:CEF), should they be buying actual physical?

JC: It really depends on the investor and their perspective. The high net worth individuals we deal with own some physical gold and silver and maybe platinum group metals that they actually store in their own vaults. They own other material that’s being held for them in depositories in various parts of the world. They also own some ETFs, some options, some mining companies and some exploration companies. So it’s really a diversified portfolio.

Except for these high net worth individuals, we don’t deal with retail investors directly as customers at CPM Group. We talk to them, though, and we do deal with people who supply the retail market. A lot of people are moving into the physical material. Demand in the ETFs also has been strong over the last few months and some of that demand comes from people who can’t get their orders filled for one-ounce coins or 100-ounce silver bars. They’re buying ETF shares instead because they’re the next best thing.

TGR: Does that carry implied leverage?

JC: The ETFs do not. The ETFs are ounce-for-ounce and it’s held in an allocated account. If I’m an investor and want to own a 100-ounce bar, I can’t find one in silver. Northwest Territorial Mint will sell me one if I want to wait 16 weeks for delivery. Silver Recycling Company [TSX.V:TSR] is also selling them and they have it for relatively prompt delivery, but that’s a very new development just in the last few weeks, in response to this market. If I’m an investor and I want to buy 100 ounces of silver and can’t find Maple Leafs or Eagles and I can’t find a 100-ounce silver bar, I can buy a share of an ETF and have it stored for me on an allocated basis through the ETF mechanism.

TGR: Suppose the economy actually does start to turn around, as you’re projecting maybe in the second half of 2009, and you have all this money on the sidelines, which you indicated might flow back into the marketplace rapidly. Does that mean gold will rise through the recovery and then go back down?

JC: Because gold is money and an alternative asset, gold and silver probably will rise in the first half of 2009 in response to the economic distress that we expect at that time. And then as the economy recovers—let’s be hopeful and say it starts in the second half of 2009—you actually might see gold and silver come off some. Platinum group metals, which we’ve only mentioned in passing, are the other way around. They’re really industrial metals, heavily tied to auto sales and so probably will remain weak until auto sales recover. But when that happens, expect platinum group metal prices to rise sharply.

TGR: You mentioned Silver Recycling starting to sell physical silver. What else can you tell us about this company?

JC: For purposes of full disclosure, I personally own some stock in Silver Recycling and they are a CPM Group client. We are financial advisers to them. I can talk about who they are and what their ideas are, what their plans are. I like the company a lot because they’re basically a consolidation play to create a publicly traded company in refining silver from scrap. They’ve identified three initial targets of small privately owned silver recyclers in the United States and are working with them. They have agreements with all three to acquire them and bundle them together, consolidate them and benefit from the economies of scale. And then there are other companies they can target later. It’s a very interesting operation. If you compare them to a silver mining company, they have the capacity to produce silver from scrap without any of the capital costs, country risks and operational risks that are common with a mine. So lower costs, less capital, fewer risks, still producing silver.

TGR: What sort of volume are we talking about?

JC: The first company they have an agreement with has 5 million ounces of production a year. The others have somewhat less. I don’t know the numbers off the top of my head, but I believe that the three companies combined would be producing something in excess of 10 million ounces a year.

TGR: Using that as rough estimate, what publicly traded silver producers come up with 10 million ounces a year?

JC: I think Coeur d’Alene Mines Corp.(NYSE:CDE) is slightly less than that this year, but maybe more than that next year. Apex Silver Mines (AMEX:SIL) and Pan American Silver Mines (Nasdaq: PAAS) probably produce more than that. Silver Standard Resources (Nasdaq: SSRI), which is moving toward opening its Pirquitas mine, will produce more than that when they’re up. There are probably a few other companies—Hecla Mining Company (NYSE:HL), maybe—that I’m going to anger people for forgetting. And then there are some larger diversified mining companies that produce much more than that. Penoles [MX:PE&OLES] is a good example. A lot of people think of Peñoles as a silver mining company and it does produce an enormous amount of silver, but it also produces lead, zinc, copper and gold. Also KGHM and BHP, but they’re not silver companies per say, either.

TGR: What other companies, either in silver or gold, would you recommend our readers take a look at?

JC: Well, we’re really commodities analysts. I’m proud to say I am not an equity analyst. I don’t sit there and tell people which equities to buy on any given day. I won’t tell anybody what to do with their equity investments, but I’ll tell you what I do with mine. I have a diversified portfolio.

Let’s look at the gold market. I have physical gold. I sometimes have futures and options in gold. In the equity side, I have AngloGold Ashanti Ltd (NYSE:AU) shares. I have Goldcorp (NYSE:GG) right now. I don’t have Barrick Gold Corp (NYSE:ABX) right now. I have in the past. I like Barrick a lot. And I have some smaller exploration and development companies in my portfolio. I tend to look for really well managed large companies that are cash flow generators, like Goldcorp, and I also look for exploration and development companies that have the capacity to bring production on stream within a couple of years, they have attractive mines, and management that I find good. So that’s it in gold.

TGR: What are some of these other companies?

JC: It’s not an exploration company along the lines of that, but one name I’ll throw out is Tanzanian Royalty (AMEX:TRE), Jim Sinclair’s company. It’s been hammered down along with everything else lately, but I still like it a lot.

TGR: And switching to silver?

JC: I like Silver Standard. I like Silver Standard’s management a lot. I think this Pirquitas mine that’s coming on stream will be a company maker. I also like Apex Silver Mines; I’ve been involved with Apex since before it actually was officially organized as a company. I think that’s good. Pan American is a very interesting growth story. Coeur d’Alene has been hammered in this market, but it has some very interesting properties, so it could do well. And Hecla is probably a tremendous turnaround story. Management over the last several years has done a remarkably good job in rebuilding Hecla Mining.

TGR: Gosh, they’ve been beaten up, too.

JC: Yeah, everybody’s beaten up. I spend a lot of time these days talking to clients about the difference between value and price. Six months ago we were talking about the fact that the price was over the value of a lot of mining assets and now we’re talking about the fact that the prices are woefully under the value of a lot of these companies. A company like Great Panther Resources [TSX.V:GPR] is a pretty interesting story. Fortuna Silver Mines [TSX.V:FVI] I like a lot. Endeavour Silver Corp (AMEX:EXK) is a good company, an emerging company. I’m afraid to leave out people. I own some Silvercorp Metals [TSX:SVM], a very interesting company with lead and silver mines in China. What I do is I look at companies from a management perspective and a property perspective. First thing is I’ve got to be comfortable with management.

TGR: What about platinum group metals?

JC: I thought platinum was overvalued years ago and it just kept rising and rising, but now it’s clearly undervalued. The cost of producing platinum or palladium at most mines in the world is higher than the current prices. About 50% of platinum in the world goes into auto catalysts, 60% of palladium and 80% of rhodium. With the auto industry and the auto market on their back in North America and Europe, these markets have spiraled down. A lot of investors who poured into the platinum markets partly based on the auto story are now pouring out. I think platinum group metals prices will rise sharply once the auto industry turns around.

And, the auto industry will turn around. Not necessarily because of the situation in the United States, but if you look at the BRICs, for example, you have a tremendous growth in auto sales and it’s fallen. In China it’s gone from 15% per year down to about 8% per year, but that’s a cyclical thing. It will turn itself around and people will start buying more. An interesting thing about platinum is that you don’t have the share market similar to what you have in gold and silver. In North America you have North American Palladium Mines (AMEX:PAL) and you have Stillwater Mining Company (NYSE:SWC). Both are having problems right now.

TGR: With costs exceeding current prices, the issue on the production side is clear, but what’s the problem on the exploration side?

JC: They can’t get financing. And insofar as some of these companies are exploring in South Africa, problems related to electricity and electricity allocations predate the bank panic. South Africa basically has not really invested in electricity-generating capacity for a decade. Those power shortages and outages are going to take many years to solve. They’re saying they’ll pay attention to existing mining companies, existing corporations, existing consumers of electricity. When you’re building a mine, you have to go to Eskom, the state electrical utility. Unless you’re already in the construction phase and have your electricity allocation, they’re just going to say they don’t know when they will be able to supply you electricity. That’s going to delay exploration and development. On top of that, the financial freeze will delay a lot of new capacity coming on stream. That will make the platinum group metals that much tighter.

TGR: As we come out of this recession, many people say certain sectors will emerge faster than others. You talked about how gold’s going to have a nice run up while we’re in recession. What commodities should we expect to come out of the recession first?

JC: I think gold and silver come out first. We’re looking at some specialty metals like ferroalloys—vanadium and molybdenum—because those markets are much tighter. The prices have been beaten up, as have the prices of larger metals like aluminum and copper. But if you look at molybdenum, for example, a lot of its uses are in transmission pipelines for gas and oil, offshore platforms for gas and oil production, and drilling pipe and production pipe for oil and gas. Even with lower oil and gas prices, these areas are going to be very strong over the next five, 10, 20 years. So we think you’ll see a relatively fast turnaround for a lot of these specialty metals, things that are harder to come by, but generally speaking are indispensable in critical economic applications. I think steel will also do very well because I expect the new government in the United States to undertake a major new program to rebuild all of these bridges that are about to fall down. I think you’ll see steel do very well from that perspective.

A graduate of the Missouri School of Journalism (University of Missouri, BJ, 1977), Jeffrey M. Christian chose his course of study because he was interested in chronicling developments in places such as Africa, Asia, Latin America and Central and Eastern Europe (well before they emerged as significant world economies). In 1980, Jeff left his job as an editor at Metals Week, an industry publication—having decided that metals markets he wrote about appealed to him more than journalism did. A year before Goldman Sachs acquired it, J. Aron and Company brought him on board and he soon managed the Commodities Research Group’s precious metals and statistical work there. In 1986, he engineered a leveraged buyout of this group—of which he was then VP—to create CPM Group, which he has led to become a world-class research, consulting, investment banking and asset management company that focuses on the fundamental analysis of global commodities markets. Jeff continues to write extensively.

Since the late 1970s, he has authored many pieces on precious metals markets, commodities and world financial and economic conditions. In 1980, he wrote World Guide to Battery-Powered Road Transportation: Comparative Technical and Performance Specifications. Now out of print, it remains a great index of many of the earliest electric cars. In 1981 he wrote one of the first market reports on the platinum metals group. Fast-forward to the 21st century, he and his staff of analysts write six major reports per year for publication and 12 monthly reports plus several more weekly reports and special reports. He published Commodities Rising in 2006. Jeff has pioneered application of economic analysis and econometric studies to gold, silver, copper, and platinum group metals markets, as well as efforts to improve and extend the quality of precious metals and commodities market statistics and research overall. As passionate about his work today as he was 22 years ago, he loves the fact that it gives him a tremendous network of contacts at high levels and a tremendous amount of discretion as to the work CPM Group undertakes. CPM counts among its clients many of the world’s largest mining companies, industrial users of precious metals, central banks, government agencies and financial institutions.

===========================================

The Safest Ways To Invest in Gold and Silver

By: Jason Hamlin of Gold Stock Bull

I am often asked what is the best or safest way to get exposure to precious metals. To be sure, there is a dizzying array of options from owning and storing the physical metal yourself to buying junior mining stocks. But the current crisis of confidence, brought on by the collapse of institutions that nobody thought could fail and the most recent $50 billion Ponzi scheme, has investors looking at safety and wealth preservation more than ever.

Buying physical gold and silver gives the owner definite possession, but comes with high premiums and the necessity to store and protect the metal. This can be done via a bank safe deposit box, but adds to the cost of owning the metal and doesn’t provide total peace of mind for many investors that have lost trust in the banking system. Others might prefer to store the gold on their property, hiding it in the floorboards or purchasing a safe. But this potentially puts you and your family members in harm’s way and again does not offer 100% security.

For investors that prefer not to hold the physical gold, yet place a high value on the safety of their investment vehicle not to default, I recommend the Central Trust of Canada (CEF) or its all-gold counterpart, the Central Gold Trust (GTU). Unlike the popular ETFs such as GLD and SLV, these funds do not lease out your gold and they always maintain 90% or more of assets in unencumbered, segregated and insured, passive long-term holdings of gold and silver bullion. Trace Mayer of Runtogold.com, recently published an article detailing the risk of investing in GLD and SLV. James Turk and others have also covered the unanswered questions about these ETFs in earlier articles.

Setting itself apart from the competition, the stated investment policy of the Board of Directors requires Central Fund to maintain a minimum of 90% of its net assets in gold and silver bullion of which at least 85% must be in physical form. On July 31, 2008, 97.6% of Central Fund’s net assets were invested in gold and silver bullion. Of this bullion, 99.3% was in physical form and 0.7% was in certificate form.

Central Fund’s bullion is stored on an allocated and fully segregated basis in the underground vaults of the Canadian Imperial Bank of Commerce (CM), one of the major Canadian banks, which insures its safekeeping. Bullion holdings and bank vault security are inspected twice annually by directors and/or officers of Central Fund. On every occasion, inspections are required to be performed in the presence of both Central Fund’s external auditors and bank personnel. Central Fund’s chief executive comments:

Our bullion is stored in separate cages, with the name of the owner printed on the cage, and on top of each pallet of bullion it states Central Fund or Central Gold-Trust. This disables the bank from using the asset from any of their purposes. We also pay Lloyds of London for coverage of any possible loss.

Adding to investor peace of mind, CEF has been around since 1961, is based outside of the U.S. (Calgary, Canada) and is run by a board that is respected in the precious metals community, not a bunch of corrupt Wall Street cronies. Demonstrating transparency that is much needed in today’s investment climate, Central Fund makes regular trips to visit the assets and takes their auditors with them. And you get the sense that you are dealing with honest gold investors and not slick marketing or public relations specialists by taking a quick perusal of the CEF website. While they aren’t going to win any design awards, the website is packed with all of the investor information necessary for due diligence.

On the downside, CEF does come with a hefty premium (currently at 16% to NAV). But this premium is less than the premium you are likely to pay on physical bullion, so it is a non-issue for me. And while it is a greater premium than GLD or SLV, I am willing to pay it since I have about as much faith in those ETFs as I do in the Comex.

Tax implications are another deciding factor. Ian McAvity, founding director and advisor to CEF, said there are definite tax advantages to CEF as opposed to an open-ended ETF. Long term gains in the gold ETFs (and presumably Barclays’ silver ETF) would be taxed as collectibles at 28%, according to the Gold ETF prospectus. As a passive foreign investment company with shares not convertible into bullion, CEF is believed to qualify as a passive foreign investment company [PFIC] to enable the 15% capital gains tax treatment, which can be an important factor for investors with long-term ambitions and taxable accounts, said McAvity.

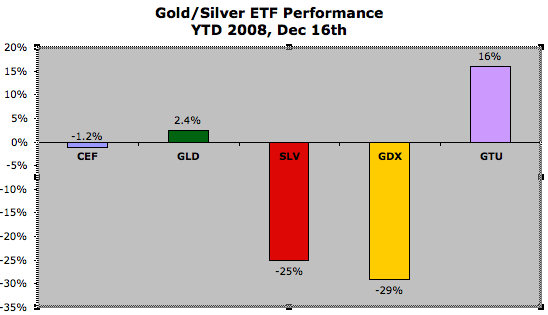

Lastly, we should consider the performance of the various investment options. Year-to-date CEF underperformed by 3 points versus GLD, but this is largely due to the silver exposure. A more fair comparison would be to use Central Gold Trust. GTU significantly outperformed GLD (14 point gap), which should ease any concerns investors have about a higher premium. CEF and GTU offer not only more peace of mind, but better returns compared to the “trust us, the gold/silver is there” approach from iShares or SPDR. It is also interesting to note that the Gold Miners ETF (GDX) is the worst performer year-to-date. This could change as precious metals prices take off in 2009, but I am inclined to park at least half of my gold/silver investments in a safer place than stocks or funds that can’t prove that they actually have physical gold to back my investment dollars. Year-to-date returns are as follows:

click to enlarge

While GTU has outperformed CEF during 2008, I expect silver to outperform gold during the next upleg and thus I own and favor CEF for 2009. Regardless, both of these funds represent sound investment choices during a time when there are fewer and fewer safe places to park your assets. Peace and prosperity to all.

============================================

Mickey Fulp, “Mercenary Geologist”: Look for the Right Share

Structure, People, and Projects

Sourcee: The Gold Report

“Mercenary Geologist” Michael S. (Mickey) Fulp’s 29 years of field experience as an economic geologist evaluating exploration and mining projects throughout the Americas and China make him uniquely qualified to give The Gold Report an intriguing overview of what’s happening now in gold, precious metals and rare earths, and uranium. Mickey, always on the lookout for companies with the right share structure, people, and projects, is a proponent of the “Boot Leather and Drilling” style of exploration. He gives us a quick tour of his take (and favorite stocks) in the sector.

The Gold Report: On your website, it says you look for stocks that can double share price in 12 months or less. Is that still true in this bear environment?

Mickey Fulp: Most definitely. It’s not so easy to pick those doubles now, but I certainly think that should always be the goal in speculative resource stocks. I’ll pick stocks that I think will double in 12 months or less and stick to the way I’ve always traded; that is, when those stocks double, I sell half of my position plus enough to cover my brokerage fee; then I’m playing with the house money with a zero cost basis and half my original position. Then I take that money and do it again on another stock.

TGR: I know that you wear several hats, and I want to start with your global economy hat. What are you seeing in terms of precious metals, and how they’ll be reacting in the bear environment? Can you give me an overview of what you see happening in gold?

MF: I’m looking here on my KCAST (Kitco) gold, and it’s $753 an ounce as we speak. I think $750 is a viable price for legitimate gold producers. It’s unknown how gold will react in a deflationary environment. We’ve never really experienced a deflationary environment in modern times when the price of gold was floating because, when the Great Depression started, gold was $20.67 an ounce. Roosevelt raised that to $35 an ounce in 1933, made it illegal to own privately, and the price of gold was fixed throughout the Depression and until Nixon’s debacle in 1971.

Arguably, we are in a deflationary environment right now. I personally think we’re in a depression. At some point, with the Fed creating money willy-nilly and the U.S. government bailing out all the failed financial institutions, we’re going to look at a hyper- inflationary environment; and we all know that bodes well for the price of gold.

TGR: We’ve talked about the bailout here in the U.S., but there are also forms of bailouts happening in Europe and China. If every government is inflating its currency …

MF: That’s very true.

TGR: Worldwide, doesn’t that kind of equalize?

MF: Well, you can make that argument, but it’s hard to know which currency is going to come out on top on this. Probably none because they are all fiat with no hard asset basis. Certainly, fiat currencies in nearly every country are in a world of hurt right now. We just saw the Chinese devalue its currency—what was it—6% this week? Yes, it does even out, and the price of gold will rise with hyper inflation.

TGR: Let’s switch over to silver and other precious metals. Are you focusing just on gold or do you think there’s also a play for silver, palladium, platinum?

MF: I don’t have a strong opinion on platinum and palladium because they are so driven, no pun intended, by the auto catalyst market and with the downturn in automakers worldwide, that does not bode well for those two metals. On the other hand, they certainly have value as precious metals. Silver is also a bit of both. It’s both an industrial metal and has some value as a store of wealth. One thing I’ve looked at lately (and I’ve actually been a buyer of physical silver for the last couple of months or so), is the gold-silver ratio. Whenever it gets high, as it is right now, I consider that a buying opportunity in silver.

There’s been a lot of press about silver not being available, but silver is available in large bars. You can buy a 1,000 ounce bar through COMEX and take delivery on a January contract now—for somewhere around 25 cents over the spot price, if you pick the right broker. When I see the gold-to-silver ratio go above 80, I consider that a buying opportunity for physical silver.

TGR: We always hear that silver has more swings than gold and it will lag gold when gold starts to go up.

MF: It does have wider swings and that gives it some more volatility on both the upside and the downside. I look at that as a way to make money. Because of its volatility, it could lag gold on the way up; if it does, then the ratio gets out of whack. Historically, the ratio was 16:1. When gold and silver were both floated on the open market that ratio grew. Over the past 10-15 years it has been somewhere between about 40 and 70. As we speak right now, it’s 80.

So you can play sort of an arbitrage; the increased volatility of silver compared to gold gives you some leverage, much the same as playing junior resource stocks gives leverage on both the upside and the downside vs. the price of gold. Junior resource stocks will go up and down with much more volatility than the price of gold, so that’s how we end up with the proverbial five or ten baggers. In this environment, those five and ten baggers can be negative five and ten baggers. But at some point, resource stock valuations get so low that good companies—especially those with current gold production or near-term production, positive cash flow, and in particular, takeover targets—are ridiculously undervalued.

TGR: In your newsletter, Mercenary Musings, do you talk about buying physical gold and silver or do you focus on equity investments?

MF: I focus on many things, including stocks, educating investors, markets and macroeconomics, commodities, libertarian ideals, my field adventures, etc. I’m not a certified financial analyst. I’m a geologist with nearly 30 years experience. I basically tell people what I have done, or am doing, in the market. For instance, when I find a stock I like, I may say I’m accumulating this right now; I like this about that, etc. So my newsletter is quite varied.

TGR: We were talking earlier about palladium and platinum and I noticed that one of the companies you have in your technical analysis is Avalon Ventures Ltd. (AVL: TSX-V). I believe that’s a rare metals company.

MF: Yes, it is.

TGR: Would you talk a little bit about your viewpoint of rare earth elements, kind of global economics, and the importance it will play or the downside it will face given the recession that we’re all going through?

MF: That’s a very good question. Rare earth elements are increasingly used for high-tech applications, specifically super magnets and batteries. They are in short supply because in the late ’80s and early ’90s, the Chinese developed a very robust deposit in Northern China and, basically, they cut out all the established world producers by drastically lowering prices. They now supply over 90% of the world’s rare earth elements. These metals are critical for hybrid cars and large commercial air conditioning systems; they’re also used extensively in high-definition LCD TVs and electronics technology. For example, cerium provides the red color for your little LCD headlamp. So there’s a bunch of varied high-tech uses for these metals. Certainly demand for those things is dependent on a viable world economy.

Avalon’s in an interesting position, as it has a unique deposit in the Northwest Territories about hundred kilometers East-Southeast of Yellowknife. The Thor Lake deposit is concentrated in the heavy rare earth elements. Rare earth elements are kind of a mixed bag of 16 elements (15 plus yttrium), and they always occur together. Avalon’s deposit is unique in the fact that, in this series of 15 elements on the periodic chart from atomic number 57 to 71, the heavy rare earth elements are much more rare than the light rare earths.

As a result, they are in greatly increased demand and they trade at very high values, hundreds of dollars per kilogram in some instances. So I’m bullish on the long-term prospects for Avalon. It’s really been beaten up lately with a year high of $1.97, a year low of about 35 cents; currently it’s at 40 cents. It made a rally a couple of months ago and has gone south since then. The key to Avalon is they have a deposit that is potentially economic outside the Chinese supply monopoly. They are being courted as we speak by Japanese auto makers because the Japanese cannot depend on the Chinese for a supply of rare earth elements. The Chinese have put on export quotas and taxes because, as much as possible, they want to keep all their production in China and develop processing facilities there. They consume about 60% of the world’s rare earths.

TGR: You said earlier the key to the deposit of Avalon is to make it viable outside the Chinese monopoly. It sounds to me that, given the two facts you stated immediately afterward, it’s going to be clear imminently.

MF: It’s going to be clear soon because Avalon is working on a resource estimate as we speak that will include drilling through last winter. They drilled this summer with great success, and they will come back with a second resource estimate and a process metallurgical report, probably by the end of the first quarter of next year, and then move on to a pre-feasibility study. So, assuming we have a viable world economy—and, arguably, that’s questionable right now—I would look at Avalon as in play, if you will, or looking to secure an off-take agreement for its production with a Japanese company sometime in 2009.

TGR: When will it start producing?

MF: I think they’re still about four years away from actually constructing a mine and getting it into production. The climate up there is northern boreal forest and water or ice, so for the construction phase, it’ll be a seasonal operation.

TGR: Are there other potential prime geological territories that might produce these rare earth metals?

MF: The area that comes to mind, of course, is Mountain Pass, which is in southeast California. It dominated world production until it was cut out by the Chinese. It’s just sitting there, held by Unocal with something like 20 million tons of nearly 8% to 9% in dominantly light rare earths, so this is a bit of a different market than what Avalon would be courting because Thor Lake is a heavy rare earth element deposit. There’s also a deposit in Australia, Lynas Mining’s Mt. Weld, concentrated in neodymium and it could dominate the supply of neodymium.

TGR: Is that in production?

MF: No, but it is in development and pending completion of concentrating and materials plant facilities. The rare earth elements themselves are not particularly rare, but the deposits that concentrate them in minable quantities are extremely rare worldwide.

TGR: I also see, when looking at your Mercenary Musings online, that you had a recent Musing regarding Animas Resources (TSX.V:ANI). What caused you to write about that specific company?

MF: Well, as with most of the things I cover, I put my Mercenary money where my mouth is. I was an IPO investor of Animas Resources. I still hold the warrants. It’s a story I have followed since inception. I have a bit of a mantra about a good company; it’s got to have the right share structure, people, and projects. And, in my view, Animas has all three of those.

It’s a Carlin-type system in Northern Mexico, having produced 650,000 ounces of gold in the 1990s, and then shut down in 2000, because of a depressed gold price of $300 an ounce. It shut down with an historic resource, not 43-101 qualified and I need to make that clear, of 718,000 ounces. It has the geologic characteristics of Carlin-type systems in northeast Nevada and, in my Musing, I list 10 of those.

It’s never been drilled deep, and it’s never been drilled systematically under gravel cover adjacent to the 12 small deposits that were mined in 22 separate pits. So it’s historically been a district—and Animas controls the entire district—that has produced from small deposits. Management at Animas includes a “who’s who” of senior-level geologists who have worked for major mining companies. One of its consultants is Odin Christensen. Odie was Chief Geologist for Newmont Mining Corp. (NYSE:NEM) in the Carlin Trend when it first was drilled deep. And huge, deep high grade gold deposits were found, which really made the Carlin Trend. I see the same geological characteristics at Santa Gertrudis. The management is good; low number of shares outstanding—less than 27 million shares; very tightly held. It hit an all-time low at 29 cents today; it’s very encouraging that the entire management and controlling group of this company has never sold shares or exercised options. They obviously like the project and intend to play it out.

It’s strictly an exploration play. I don’t like very many exploration plays right now; but, with working capital at $4.5 million, they can go at least to early 2010 and give Santa Gertrudis their best shot. If they find big, deep, high-grade Carlin-style deposits, they will be in play as a takeover candidate. If they don’t, they have other options. There are lots of small miners in Mexico, small junior companies mining less than 100,000 ounces a year in that region. Animas has six different projects in the district and it could JV some of them out to people that want to mine on a smaller scale.

TGR: We covered gold, precious metals and rare earths, and uranium. It’s been quite a tour around the world here very quickly.

MF: I have one other gold company that I like—PDX Resources Inc (TSX:PLG), formerly called Pelangio Exploration.

TGR: What’s caused you to focus on this one?

MF: I followed the story for quite some time, did my detailed due diligence, and became a shareholder. PDX owns 19 million shares of Detour Gold (TSX:DGC); the Detour Lake gold property in Northern Ontario. Detour Gold, at a $700 gold engineered pit, has 10.75 million ounces of gold resource. That’s measured and indicated resource. That’s always important—measured and indicated. It has some additional inferred, but I don’t pay much attention to inferred resources.

If you do the math, Detour Gold is now being valued at over $15 per ounce of contained gold. PDX Resources owns 42.4% of Detour Gold shares and their valuation now is $10.50 an ounce. Detour Gold is in the final throes of a feasibility study. It was scheduled to be out by the end of this year; I do not know if they’re presently on schedule for that, but they become a takeover candidate with a positive feasibility. You have leverage there for PDX shares vs. Detour Gold shares, at a 30% discount per ounce of gold in the ground.

TGR: But you’re saying Detour is the potential takeout candidate?

MF: Yes, it is.

TGR: Isn’t this what you mentioned earlier, where the only potential company that would take them out because of their share structure is PDX?

MF: No, PDX Resources originally spun out 50% of the deposit to a new entity, Detour Gold, a Hunter-Dickinson company and now exists only as a shareholder of Detour Gold. It is the minority shareholder, and is comprised of expert explorationists. So recently in September, it spun out all its other properties into a new exploration company, which is Pelangio Exploration; thus PDX holds its Detour Gold shares solely for investment purposes. With 10.75 million ounces, this is a huge deposit; it was a past producer of Placer Dome. It failed because of a low gold price in the previous downturn in the gold business. I think you’re probably looking at a bidding war for Detour Gold.

Goldcorp (TSX:G) (NYSE:GG) is the obvious candidate and we saw what Goldcorp did with its acquisition of Gold Eagle in the Red Lake District. Kinross Gold Corp (K.To) (NYSE:KGC) is a possible suitor. With this size of deposit, you’ve got to throw in the big boys—Barrick Gold Corp (NYSE:ABX), Newmont, Anglo, Gold Fields Ltd. (NYSE:GFI)—and some of the mid-tier gold companies looking to become major producers. It’ll get taken out at the Detour Gold share price, which is now trading at $15 per ounce of gold in the ground, while PDX is currently trading at $10.50. That’s 30% discount, so you have leverage to the upside with PDX Resources. Make sense?

TGR: That’s a great and very interesting play. Mickey, thank you for your time.

Michael S. “Mickey” Fulp, who launched MercenaryGeologist.com in late April 2008, brings more than 29 years of experience to his role as an exploration geologist. Specializing in geological mapping and property evaluation, Mickey has worked as a consulting economic geologist and analyst for junior explorers, major mining companies, private companies and investors. Check out his website for free access to the Mercenary Musings newsletter, as well as technical reports. Future offerings will include a premium paid subscription service that provides early and special access to subscribers. You may contact him at mailto:Mickey@MercenaryGeologist.com.

=============================================

Now Gold is currently up over $35/oz. What are you waiting for? Time to get on board- Good Trading! – jschulmansr

")

")