Tags

agricultural commodities, alternate energy, Austrian school, Bailout News, banking crisis, banks, bear market, Bollinger Bands, bull market, capitalism, central banks, China, Comex, commodities, communism, Copper, Currencies, currency, deflation, Dennis Gartman, depression, diamonds, dollar denominated, dollar denominated investments, economic, economic trends, economy, Federal Deficit, financial, Forex, futures, futures markets, gold, gold miners, hard assets, heating oil, India, inflation, investments, Keith Fitz-Gerald, Marc Faber, Mark Hulbert, market crash, Markets, mining companies, Moving Averages, natural gas, oil, palladium, Peter Brimelow, Peter Schiff, physical gold, platinum, platinum miners, precious metals, price, price manipulation, prices, producers, production, protection, rare earth metals, recession, risk, run on banks, safety, Saudi Arabia, Sean Rakhimov, silver, silver miners, socialism, sovereign, spot, spot price, stagflation, Technical Analysis, timber, U.S. Dollar, volatility, warrants, Water

Currently Gold is down $14-$15 dollars per oz. around the $914 level. As I wrote in my last post if we hold this level then $950 will be our next target. If it fails here then we may have a test back to $885 – $890. Either way I’m taking the opportunity to buy on dips since long term inflation is certainly due to happen and Gold is where you want to be when that happens. Personally, I think $900 to $925 is the new base and we have avery real possibility of $1000+ Gold price before the summer truly begins.- Good Investing – Jschulmansr

==============================

==================================

Update on the Gold Trade – Seeking Alpha

By: Trader Mark of My Mutual Fund

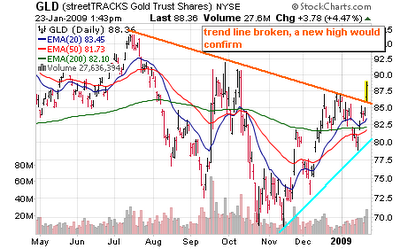

Last Friday we said gold might finally have it’s real breakout here [Jan 23: Could be the Real Breakout in Gold] I wrote:

Things to like:

1) a series of higher lows

2) the trendline of lower highs has been penetratedThings to see for confirmation:

1) any pullback is bought

2) price prints over October 2008’s highs, signaling the end of “lower highs”

This was what the chart looked like at the time:

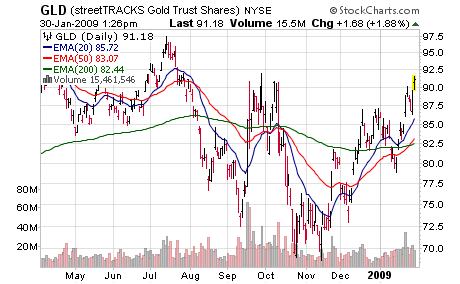

Now?

Without benefit of the orange line – you can see condition #1 has been fulfilled – we “backfilled”, tested the area we broke out of and people were eager to buy. On that, an aggressive trader would be buying. A reader mentioned this outcome last week.

For someone more conservative in orientation, you want to see #2 “a price point over October 2008’s highs” – then we end our half year of lower highs. We are withing spitting distance here with GLD at $91.40 and the October intraday high at $92.

It’s hard to get behind gold fully because there is no “earnings” behind it; it’s all about sentiment. But the theory is that as all the world’s troubled countries race to devalue their currencies (print, print,print) to “save the system,” a hard asset should retain its value. Silver is likewise breakout out, although silver has a lot of industrial uses as well.

I hate to chase a move, but from a technical set up, a lot of institutional money could be set to finally jump in here….

Now the question of what instrument to use – keep it simple or go with a miner? etc.

Disclosure: No position

=================================

My Note- Great call by Trader Makr but I have to ask, why no position Trader Mark? – jschulmansr

=================================

=================================

Fed Monetizes Debt Leading Investors to Embrac Gold – Seeking Alpha

By: Boris Sobolev of Resource StockGuide.com

In January gold rose significantly against all major world currencies. In most currencies except in the US dollar and the Japanese yen, gold actually made an all-time-high.

January Performance

GOLD / USD 5.3%

GOLD / EUR 16.7%

GOLD / AUD 16.5%

GOLD / JPY 4.4%

GOLD / GBP 5.8%

GOLD / CHF 16.3%

10-Yr Yield 13.0%

click to enlarge

At the same time, most capital markets have been falling.

January performance

DOW -11.5%

S&P -11.4%

NASDAQ -9.0%

FTSE -6.4%

DAX -9.8%

Nikkei -9.8%

Shanghai -9.3%

The governments around the world are trying to take initiative while private capital is sitting on the sidelines, preferring the safety of government bonds and precious metals.

Investors typically do not trust the governments to implement any effective economic solutions. Moreover, this lack of faith in central planning continues to grow since the US government has no other plan of action than to save the old, compromised and untrustworthy financial system.

What the Federal Reserve together with the Department of Treasury has shown is that they will inject a vast amount of newly created money into a hugely ineffective financial system.

While in the fall of last year, in fear of devastating deflation, analysts were competing in downward projections for the price of gold, now the competition is to estimate the amount of losses incurred by the financial institutions around the world. The maximum assessment is now at $4 trillion, with Nouriel Roubini coming in close second at $3.6 trillion.

But the main problem is not so much in the amount of credit losses or the amount needed for recapitalization efforts but in that the new government is committed to continue to transfer huge capital into the hands of the same group of people who were largely responsible for the world financial crash in the first place. Wall Street, though transformed, will remain in control.

The lack of trust in the ability of insolvent financial institutions to run the modern financial system is moving investors into gold.

An even more important gold catalyst was the Federal Reserve. In comparing the two latest Fed statements, two things stand out. Here is the evolution in wording:

December Statement: “In light of the declines in the prices of energy and other commodities and the weaker prospects for economic activity, the Committee expects inflation to moderate further in coming quarters.”

January Statement: “In light of the declines in the prices of energy and other commodities in recent months and the prospects for considerable economic slack, the Committee expects that inflation pressures will remain subdued in coming quarters. Moreover, the Committee sees some risk that inflation could persist for a time below rates that best foster economic growth and price stability in the longer term.”

December Statement: “The Committee is also evaluating the potential benefits of purchasing longer-term Treasury securities.”

January Statement: “The Committee also is prepared to purchase longer-term Treasury securities if evolving circumstances indicate that such transactions would be particularly effective in improving conditions in private credit markets.”

First, the FOMC sees a threat of deflation and second it is prepared to counter this threat by purchasing longer-term treasuries.

Purchases of long term bonds is the most inflationary move that a central bank can undertake because it represents direct monetization of the government debt and hence an unconcealed debasement of national currency. (This is happening at the same time as the new Secretary of Treasury is chastising China – the main US creditor – for currency manipulation.)

Why did the Fed make such a determined statement, with one member even voting to begin long term treasury purchases immediately? First and foremost, the real estate market is not showing any signs of life. House prices are falling, time required to sell new homes is rising and most importantly, after a steep fall in December, average mortgage rates began to rise again, reaching 5.34% as of last Friday.

Since mortgage rates are closely tied to the 10-year treasury yield, the Fed stands ready to buy government debt and help make housing more affordable via low mortgage rates. The hope is that such action would help put an end to a decline in asset prices and stop the deflationary spiral.

In fact, the latest Fed balance sheet showed that long term treasury purchases have already started, with around $1 billion in notes (5-10-year maturity) purchased for the week ended January 21st. This is a modest amount, but it is a statement that the Fed is ready to do more than just talk. Traders have indeed sensed this development and Treasury Inflation-Protected Securities (TIPS) (TIP) are also beginning to reflect greater inflation expectations.

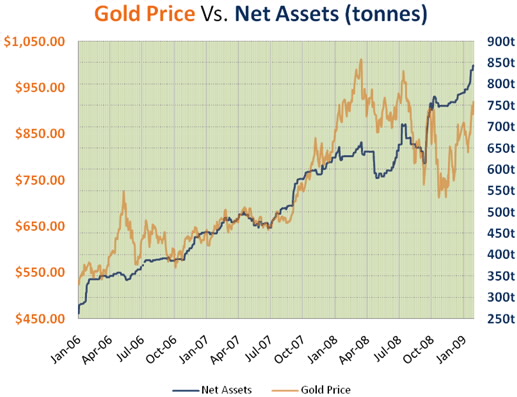

Gold investors are also sniffing out the coming price reflation as they piled into the SPDR Gold Shares (GLD) at an increasing rate.

For the month of January, GLD gold holdings rose 8.2% or close to a record setting 63 tonnes. At this rate, GLD will soon surpass Switzerland in its gold holdings, thus becoming the world’s sixth largest gold owner after the US, Germany, the IMF, France and Italy.

If the Fed continues to purchase long term treasuries, it is clear that there is only one way for gold and gold stocks and it is up.

================================

================================

Gold as Part of a Portfolio – Seeking Alpha

By: San Olesky of Olesky Capital Management

Many investors have been thinking about gold recently. Some have considered it because it has been a relatively strong performer with the iShares COMEX Gold Trust (IAU) closing up 5.4% in 2008. It’s up 2% year-to-date as of Wednesday’s close. The iShares S&P 500 Index ETF (IVV) was down 36.94% in 2008 and is down 6.17% year-to-date as of Wednesday’s close. Other investors or traders have bought or considered gold as a classic safe haven.

My inclination is to refute the efficacy of buying or holding gold for security either in the form of an ETF or, more so, in the case of gold bullion bars or gold coins. However, as the financial crisis became more severe last year, a couple of clients approached me about adding gold to their portfolios. Rather than diplomatically rejecting the proposal, I told them that I would investigate the historic effects of holding gold in a portfolio. Long story short, I found that adding a small, reasonable allocation to gold reduced portfolio volatility substantially and increased return slightly.

A simple diversified portfolio consisting of 1/3 S&P 500, 1/3 Real Estate Investment Trusts (REITs), and 1/3 10 year U.S. Treasuries would have produced a compound annual growth rate (CAGR) of 8.47% with 11.15% volatility (standard deviation – SD) from 1993 to 2008. For comparison, the S&P 500 produced a 6.67% CAGR with a 20.16% SD. Although few investors would implement this 1/3 – 1/3 – 1/3 allocation, diversification is proving its strengths here. All of these statistics incorporate rebalancing annually.

Let’s take the same 1/3 – 1/3 – 1/3 portfolio and alter it to include a relatively small allocation to gold. That allocation will be 30% S&P 500, 30% REITs, 30% Treasuries, and 10% gold. Over the same timeframe the portfolio with gold produced an 8.49% CAGR with a 9.86% SD. The portfolio with gold produced a slightly better CAGR with volatility that was 11.6% lower than the 1/3 – 1/3 – 1/3 portfolio. The diversified portfolio with gold produced a CAGR that was 27.3% higher than the S&P 500 and 51.1% less volatile than the S&P 500. The S&P 500 had 4 losing years with the worst being a loss of 37% last year. The 1/3 – 1/3 – 1/3 portfolio had 3 losing years with the worst being a loss of 18.15% last year. The portfolio with gold had only 2 losing years with the worst being 15.74% last year.

In constructing sound and productive portfolios we would like to include assets that have high returns, low volatility, and low correlation to the other assets in the portfolio. Looking at gold’s average annual returns, relative volatility, and relevant correlations, one should expect that gold would be a constructive addition to many portfolio allocations. In fact, gold even has a relatively low correlation with commodities in general (S&P Goldman Sachs Commodity Index). However, we should learn from the past but not expect it to repeat itself exactly. There is much to be learned from historic returns, volatilities, and correlations of asset classes. With all due respect to history and math, we must use reason when constructing portfolios. I view gold as a very narrow and idiosyncratic asset. So, I do not feel that it is wise to strategically allocate as much as 10% to the asset although the historic, mathematically optimal amount would be higher in the context of some portfolios.

What did I do? Based on my tests and observations, I bought a little gold last year for some of my clients. I have incorporated a small allocation to gold into their continuing strategic allocations.

====================================

My Note: This is great news even the Non Gold Bugs are become cautiously bullish!-jschulmansr

====================================

====================================

Finally and extremely interesting article you want to read! Be sure to click on the chart links too…- jschulmansr

Economy Watch: What if Stocks Were Priced in Gold?- Seeking Alpha

By: Paco Ahlgren of Ahlgren Multiverse

“Everything has its limit — iron ore cannot be educated into gold.”

— Mark Twain

Several charts have been floating around the Internet for some time, showing the historical Dow Jones Industrial Average, priced in terms of gold. The simplest explanation entails thinking of the Dow divided by one ounce of gold; if the Dow is at 5000, and gold is at 500, then Dow-to-gold is 10. But it’s important to remember as you’re considering this ratio that the Dow is calculated in terms of dollars. So essentially, when we determine the Dow-to-gold ratio, it’s not just a simple ratio of gold to shares in the Dow, but rather it is a three-part ratio — Dow, expressed in dollars, to an ounce of gold.

Wouldn’t it just be easier to express gold in terms of dollars, or the Dow in terms of dollars? Well, those are certainly useful ratios — and we use them all the time — but what we’re really going after when we look at a historical Dow-to-gold chart is how well the Dow has performed, relative to the dollar, and relative to gold. What have inflationary pressures done to the Dow, in terms of gold and the dollar, over the past century? How have the three components moved in the various historical boom-bust scenarios? The results are interesting.

Let’s shift gears for a moment. Just off the top of your head, what would you expect stocks to do in periods of inflation? The dollar loses value rapidly, right? And that means prices of goods and services move higher, presumably with wages. So wouldn’t it stand to reason, intuitively, if corporations were making more money as prices increased, profits would increase too? And if profits increase, shouldn’t share prices go higher in response?

It turns out that inflationary price increases are bad for the stock market, and no period in history establishes this more concretely than the late 1970s and the early 1980s. Interest rates and prices soared, along with the price of gold, but stocks were flat. I want you to think about what I’m saying here: prices in general were going up, and yet the stock market was not. What this means is while stocks, in nominal terms, looked to be relatively stagnant, in real terms they were getting crushed. This is why the Dow-to-gold ratio is so significant as an indicator of relative value.

There is an elegant, simple truism that comprises every single transaction between buyers and sellers, and yet most people don’t even think about it: whenever you buy something, you are selling something else. When you buy corn, you are selling dollars. When you buy a Ford, you are selling dollars. If you are in Mexico and you buy a chicken, you are selling pesos. Of course, if you came from the U.S., you first sold dollars, bought pesos, and then sold pesos to buy the chicken. I know most of you already understand this concept, but I’m trying to emphasize that even when currency is used, every transaction is merely a trade; that is to say, the transaction is nothing more than negotiation that results in the exchange of two things — whether goods, services, or currency.

With that in mind, consider this: when prices rise because of inflation (printing of money), it isn’t so much that goods and services are getting more valuable — rather it’s much more accurate to say the currency is simply getting less valuable relative to everything else. If the dollar collapses, for instance, and the cost of a loaf of bread goes from $1 to $20 at the same time a share of Microsoft (MSFT) goes from $20 to $30, then Microsoft is severely under-performing — in inflation-adjusted dollars. A loaf of bread will cost you 20 times what it used to — not because it is more valuable, but because the dollar is less valuable. Meanwhile Microsoft is worth only 50% more. Relative to the dollar, shares of Microsoft are actually losing money — in a big way.

If you look at a chart of inflation from 1978 to 1982, you’ll notice a huge spike. If you look at a chart of the Dow Jones Industrial average during the same period, you’ll see that stocks traded sideways in a fairly well-defined range over the same period. But that doesn’t tell the whole story; if you adjust for the meteoric rise in prices during that five-year period, the stock market actually performed much worse than the nominal dollar fluctuations presented in the historical chart. In other words, the price of just about everything was going up dramatically, but stocks were not. So if you adjust prices back to “normal” levels, and adjust stocks accordingly, the picture for equities would have been horrible.

Now for the pièce de résistance…

Here is a series of charts of historical nominal gold prices (not adjusted for inflation), in several different currencies — the first of which is U.S. dollars. Take a look at the spike in the price of gold from 1977 to 1981. Now, if we go back to our original chart above, showing the Dow Jones Industrial Average, in direct relation to an ounce of gold (Dow-to-gold), you can see that the ratio went roughly 1:1 in 1980 — at the peak of the inflationary price surges. To clarify, the Dow was at about 750, as was gold.

But didn’t we say that, relative to rising prices, the Dow actually underperformed dramatically? So if you bought gold in the mid-1970s, not only was your investment skyrocketing, but the stock market — which was flat in nominal dollars — was actually doing very poorly relative to rising prices. Bear in mind that both the Dow and gold were priced in terms of nominal dollars at the time; they essentially “cancel out” — that is to say, relative to rising prices, gold also failed to perform as well as the nominal dollar-price. Still, it did offer an excellent hedge against rising prices, and even outperformed during the period.

What does all this mean? Well, for starters the average Dow-to-gold ratio over the last century has been about 9.5, and we are currently at about 8.5. So you’re probably thinking we’re oversold and due for a correction. In other words, the Dow-to-gold ratio is probably going higher, right? Well that was my first conclusion too, but actually on closer examination it turns out that’s probably not right at all.

For much of the last century the dollar was tied to gold, and while the relationship was never perfect — and the U.S. government betrayed the union many times, in many different ways — there was at least some relationship, which helped pull the ratio down. Eventually, excessive inflationary printing caught up with the government in the 1960s, and it became clear it wouldn’t be able to honor redemptions against the dollar at the price it had fixed. Nixon essentially defaulted on the U.S. promise to redeem dollars for gold by taking the U.S. off the standard in the 1970s — and this, more than anything else, allowed inflationary pressure to drive general prices into the stratosphere. This was the moment the Dow-to-gold ratio approached 1:1. To fight rising prices, Paul Volcker, the Fed Chairman at the time, pushed the Fed’s target interest rate past 20% and barely saved the U.S. economy from collapse.

For most of the next 20 years, gold fell and stock prices rose. Meanwhile, the U.S. government capitalized on the lie it had created and printed more and more money. Who really cared? Everyone was making money in the stock market, and prices remained relatively stable. In fact, every time prices failed to act “correctly,” the Fed simply changed the rate at which it would lend to banks. But the illusion of the monetary policy game couldn’t last forever; people used easy money printed by the government to buy assets they couldn’t afford throughout the economy — especially houses. Finally the pressure was just too much, and everything started unraveling in 2007. But the gold market seemed to understand the game couldn’t last, and around 2000 it started a slow, steady rise.

Relative to everything, the number of dollars in the system in early 2009 is almost incomprehensible. Once de-leveraging reaches its nadir — and it’s coming soon — those dollars are going to hit the economy and drive prices much higher.

What have we learned about stocks in such periods of rising prices? Not only do they fail to perform, but adjusted for inflationary price pressures, they actually under perform. General prices and unemployment will continue to rise. The consumer will continue to be unable to consume. Corporate earnings and dividends will continue to collapse as a result. Stocks are going lower — probably much lower.

And what about the price of gold? It will almost certainly continue to increase — not only because people will flock to its long historical stability and consistency, but also because there are simply so many more dollars (and yen, and rubles, and euros) in the world. Remember, the U.S. isn’t the only country printing innumerable sheets of currency. And in that context, remember also that inflationary price increases have almost nothing to do with increased demand, but rather they are the result of currency devaluation and destruction — through printing.

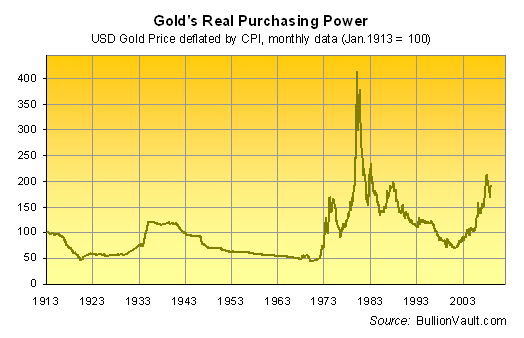

I just want to share two more charts with you. The first should give you a little perspective — it is a historical chart of gold, in both nominal and real dollars. Notice the real price of gold in 1980 (in 2007 dollars) was $2272 per ounce. If I’m correct about inflation and the fate of the dollar — and I’m confident I am — then we are nowhere near the historical high in gold. But I don’t think we’re merely going to re-test that high — I think we’re going to blow through it as the dollar loses value.

In the 1930s, as corporate earnings and dividends disintegrated, the Dow lost nearly 90% of its value from peak to trough. The U.S. was a creditor nation with a huge manufacturing base. The dollar was tied closely to gold. Since its peak in October 2007, the Dow has lost less than 50% of its value. The U.S. is a debtor nation with a relatively small manufacturing base. I can’t say it enough: we borrow profusely, we manufacture very little, and we consume gluttonously. Nonetheless, the consumer has now lost almost all his purchasing power, and corporate earnings and dividends are going to suffer massively as a result.

In 2007, the Dow peaked at about 14,150. To give you some perspective, an 85% drop in the Dow from peak to trough would put it at about 2100.

I know it’s easy to imagine the Fed has magical powers. I’ve fantasized about such things myself at times of extreme weakness — that maybe the Fed will “somehow” figure out a way to fight and defeat the unprecedented evil specter of inflation it is foisting on its unsuspecting children. Sometimes I do believe that our Lord and Savior Barack Obama will wave his charmed “unicorn horn of change” and all will be well again. Likewise, at times I feel like I could let Uncle Ben Bernanke take me just about anywhere in his helicopter of prosperity. My faith in the reverend John Maynard Keynes runs deep, as I hope, and hope, and hope. I find myself gleefully clicking my heels together and repeating, “the dollar is almighty, and the Stars and Stripes will prevail.” And when I am in this wonderful place, I have confidence that someday soon, we’ll all be buying houses with no money down, and with no jobs. Our driveways and backyards will once again overflow with boats, motorcycles, and sports cars.

Then I think about the 1930s. And suddenly I am wide-awake.

Let me ask you a simple question, and I want you to actually think about it. Do you really think we can’t get to the 1930s again? Do you really think that we’re going to return to the exuberant excess of the past few decades? If so, let me disabuse you of the notion: the United States was in much better shape, economically, going into the Great Depression than it is now. Prosperity is not coming back to the U.S. as we know it. We are in a lot of trouble.

Is a Dow-to-gold ratio of 1:1 so incomprehensible? Again, it has happened before — several times. But I’ll even take it a step further: what about a Dow-to-gold ratio of .5? Or less? I promise you, if the Fed fails to soak up all the dollars it’s putting in the system, that’s exactly where we’re going. And what, you may ask, does the Fed use to “soak up dollars?”

I’ll be glad to tell you that too. When the Fed needs to take dollars out of the system, it sells Treasuries (which means it buys dollars). The problem is, the U.S. debt-load is astronomical. Who, exactly, is going to buy that debt from the Fed? And at what interest rate? Remember, if the Fed is desperately trying to take dollars out of the system, there can be only one reason: it is scared of rising prices caused by inflation. But if the Fed floods the market with Treasuries, it will achieve exactly the opposite effect it’s looking for — it will cause rates to rise, probably dramatically. Do you really think the Chinese and the Japanese are going to buy Treasuries at a 2% yield if the Fed is panicking and trying to buy dollars to stop an inflationary price explosion? If so, you’re delusional. Chinese and Japanese people are smart. They’re not going to fund an inflationary dollar at 2%. Ever.

In the past it might have worked. Of course, in the past, the U.S. money supply was much smaller, and our ability to borrow was much stronger. But those days are gone.

As if I haven’t terrified you enough, the last thing I’m going to leave you with is really scary. It is a link to an excellent article by Mark J. Lundeen, whose insight into this economic catastrophe has been stupefying since long before all of this even started. Embedded in the article is a chart that shows historical dollars-in-circulation, relative to U.S. gold.

With that, I think I’ll let you do the rest of the math. Sleep well.

Disclosures: Paco is long gold.

Copyright 2009, Paco Ahlgren. All Rights Reserved.

==================================

If you have done the math…

=================================

That’ it for now – Good Investing – Jschulmansr

Nothing in today’s post should be considered as an offer to buy or sell any securities or other investments, it is presented for informational purposes only. As a good investor, consult your Investment Advisor, Do Your Due Diligence, Read All Prospectus/s and related information carefully before you make any investments. – jschulmansr

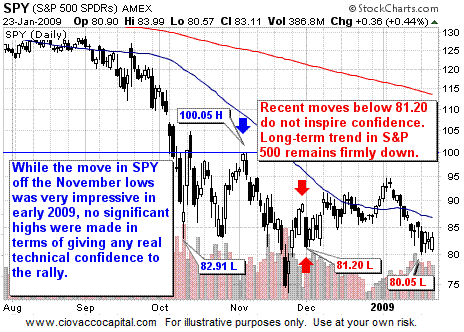

U.S. Stocks: Downtrend Remains In Place

U.S. Stocks: Downtrend Remains In Place Recent weakness in the S&P 500 Index leaves open the possibility that we will revisit the November 2008 lows around 740 (intraday). If those lows do not hold, a move back toward 600 becomes quite possible. On Friday (1/23/09) the S&P 500 closed at 832. A drop back to 740 is a loss of 11%. A move back to 600 would be a drop of 28%. These figures along with the current downtrend highlight the importance of principal protection and hedging strategies.

Recent weakness in the S&P 500 Index leaves open the possibility that we will revisit the November 2008 lows around 740 (intraday). If those lows do not hold, a move back toward 600 becomes quite possible. On Friday (1/23/09) the S&P 500 closed at 832. A drop back to 740 is a loss of 11%. A move back to 600 would be a drop of 28%. These figures along with the current downtrend highlight the importance of principal protection and hedging strategies.  Gold & Gold Stocks Still Face Hurdles

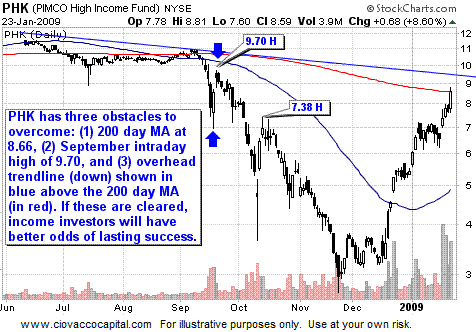

Gold & Gold Stocks Still Face Hurdles

Run In Treasuries Is Long In The Tooth

Run In Treasuries Is Long In The Tooth

Strength In Bonds Shows Little Fear of Price Inflation

Strength In Bonds Shows Little Fear of Price Inflation

U.S. Dollar Remains Firm

U.S. Dollar Remains Firm