Tags

agricultural commodities, alternate energy, Austrian school, banking crisis, banks, bear market, Bollinger Bands, bull market, capitalism, central banks, China, Comex, commodities, communism, Copper, Currencies, currency, deflation, depression, diamonds, dollar denominated, dollar denominated investments, economic, economic trends, economy, financial, Forex, futures, futures markets, gold, gold miners, hard assets, heating oil, India, inflation, investments, Keith Fitz-Gerald, market crash, Markets, mining companies, Moving Averages, natural gas, oil, palladium, Peter Schiff, physical gold, platinum, platinum miners, precious metals, price, price manipulation, prices, producers, production, protection, rare earth metals, recession, risk, run on banks, safety, Saudi Arabia, silver, silver miners, socialism, sovereign, spot, spot price, stagflation, Technical Analysis, timber, U.S. Dollar, volatility, warrants, Water

My Note- Today I present an interesting article about the Geo-Political ramifications of the Battle for the Caspian Seas, plus some of the latest Gold News. Gold today is making a much needed correction in prices, if Gold can hold here and/or we have any increase in tensions of the Middle East; I think the next leg will take prices into the $900-$950 range.- jschulmansr

Geopolitical Energy Centered on the Caspian Sea – Seeking Alpha

By: Michael Fitzsimmons of Musings From the Fitzman

I’ve just finished reading a fascinating book authored by Lutz Kleveman entitled The New Great Game. The book is about Kleveman’s visits to all countries surrounding the Caspian Sea and to the countries involved in actual and proposed oil and gas pipeline routes required to bring Caspian Sea energy assets to the world market. He interviews an amazing cast of intriguing characters along the way.

The investigative journalist delves deeply into the geopolitical implications of world powers struggling to control Caspian Sea energy reserves – some of the largest remaining oil and gas fields in the world. It is fitting the game of chess was invented by the Persians. It is worth purchasing The New Great Game just to gaze at the maps on the inside and backside covers…each central Asian country being ruled by a government or dictator who one minute moves diagonally like a bishop, only years later to morph into a rook and move horizontally and vertically like a knight, and every once in awhile going hay-wire and imitating the unorthodox movement of a knight. Who will win the great game? What will OPEC’s response be to non-OPEC oil production in the Caspian Sea region? How will China and Russia respond to American military might in the region? Only time will tell.

The map below shows the countries surrounding the Caspian Sea which are Russia, Kazakhstan, Turkmenistan, Iran, and Azerbaijan.

Most people are fairly familiar with the oil history of Baku, Azerbaijan dating back to Russian oil discovery and production in the early 1870s. Kleveman relates an interesting story of Swede Robert Nobel who was the older brother of factory owners Ludwig and Alfred Nobel who had become very wealthy producing arms and dynamite. Robert had been sent to Baku with 25,000 rubles to purchase Russian walnut to make rifle butts. Instead, he caught Baku oil fever and bought a small refinery. After only a few years, the Nobel Brothers Petroleum Producing Company vaulted over Rockefeller’s Standard Oil as the largest oil producer in the world. Later, the Nobel’s invented the first oil tanker in a story well told in Daniel Yergin’s The Prize, for which, ironically, Yergin won the Nobel Prize for non-fiction literature in 1992. And yes, the prize is named after the same Nobel family as those men seeking walnut wood for rifle butts in Azerbaijan.

Fast forward to today: Baku Azeri oil is being shipped to the Mediterranean Sea and world markets via the so-called BTC (Baku-Tbilisi-Ceyhan) pipeline. The picture below shows the pipeline’s route from Baku, Azerbaijan through Tbilisi Georgia, and finally to the Mediterranean Turkish port of Ceyhan.

This pipeline was hailed as the “Contract of the Century” by Azeri officials very much interested in getting their oil to market independent of Iranian and Russian involvement. Of course, the US was more than mildly interested in this solution as well. The pipeline is owned by a consortium of energy companies, among them:

- British Petroleum (BP): 30.1%

- State Oil Company of Azerbaijan (SOCAR): 25%

- Chevron (CVX): 8.9%

- StatOil (STO): 8.71%

- ConocoPhillips (COP): 2.5%

BP is the BTC pipeline operator.

The big question in today’s energy riddle is how to route the large energy assets of the Caspian Sea to the world market and thereby offer America an alternative to OPEC supplies. Take the giant Tengiz oil field, discovered of the coast of Kazakhstan, as an example. Estimated at up to 24 billion barrels of oil Tengiz is the sixth largest oil field in the world. It is one of the largest oil discoveries in recent history. The Tengizchevroil (TCO) joint venture has developed the field since the early 1990’s. The partners are:

- Chevron: 50%

- ExxonMobil (XOM): 25%

- KazMunayGas (Kazakhstan): 20%

- LukArco (Russia): 5%

Chevron has predicted that Tengiz could potentially produce up to 700,000 barrels of oil per day by 2010. The field also contains large reserves of natural gas. On the downside, the oil is very high in sulfur content, once reason western technology was so desperately required. Currently the oil from the Tengiz field is piped from Kazakhstan through Russia to the Russian Black Sea port of Novorossiysk via the CPC (Caspian Pipeline Consortium). The BTC pipeline is a competing option, preferred by the US to bypass Russia, but is expensive: the oil must first be tanked across the Caspian Sea from Tengiz to Baku, and then offloaded into the BTC pipeline infrastructure. French energy giant Total is interested in developing a common sense alternative pipeline through Iran which everyone knows is obviously the most economically viable solution, withstanding the geopolitical climate in Iran. Of course the US does not favor this route at all.

The US’s long favored route for Caspian Sea energy was first suggested and studied by Unocal (now part of Chevron). This countries involved in this route are highlighted in color in the picture below.

This so-called Central Asian pipeline was to begin with a natural gas pipeline from huge Turkmenistan gas fields through western Afghanistan to the Pakistani deep water port of Gwadar on the Gulf of Oman (Indian Ocean). The natural gas pipeline was to be followed by an oil pipeline along the same route, serving not only the energy starved countries of Pakistan and India, but the world energy markets as well. The US believes this route, bypassing Russia and Iran, as well as the congested Straits of Hormuz, is in the strategic interest of the US as a secure non-OPEC source of oil.

But the key word in the last sentence was “secure”. Unilateral policy decisions by the US in Iraq and elsewhere have instigated a tide of central Asian anti-American resentment. The Taliban, once supported and funded by the US, are now in control of the pipeline’s route. The pipeline project has been delayed until “control” and “security” has been established. Anti-American opposition in Pakistan is also a problem, regardless of that countries dire need for the energy and potential income the pipeline could deliver.

The US’s oil centric foreign policy agenda is apparently to irritate the two major powers in the Caspian Sea region: Russia and Iran. With the USSR’s disintegration in 1991, all the former Soviet states in the region were being eyed for their energy reserves. At the same time, Russia still considers these former states as within their “sphere of influence”.

Instead of joining with the Russians in mutually beneficial energy projects, technology transfers, and contracts, the US instead decided to take the opposite approach: it first propped up a government in Georgia irritating the Russians. Then the US supported NATO membership for former USSR countries Ukraine and Georgia. The US also proposed missile defense systems on Russia’s western borders, further infuriating the Russians. Russia finally had enough and acted in Georgia as George Bush was attending the Olympics in China. Russian actions put exclamation points on the obvious – it can take out the BTC pipeline any time it wants, and is resentful of American military meddling in its backyard.

The prior secret agreements between Putin and Bush to fight the mutual “terrorists” foes appear to be in the distant past. Recent activities involving Russian natural gas transports through Ukraine underscore the vulnerability of Europe’s energy supplies. Europe currently imports some 40% of its natural gas from Russia, and this amount is bound to increase in the future. This further complicates the puzzle by placing US actions at odds with supposed allies in Europe.

With respect to Iran, the US has military forces in Iraq, Afghanistan, Uzbekistan, Kyrgyzstan and elsewhere in the region – completely surrounding Iran. The US has further tried to isolate Iran (to the dismay of the Europeans who vitally need Iranian energy) by imposing economic sanctions on the country. Iran was one of three countries with distinguished membership in George Bush’s “Axis of Evil”. These US actions have left the Iranians no choice but to develop nuclear weapons in order to protect themselves against the same kind of American aggression they have witnessed elsewhere in the region.

Meantime, flawed US/Israeli policy, combined with Israel’s recent activities in the Gaza strip and the powerful Jewish lobbying efforts in the US for military action in Iran, seem to increase the odds for more conflict in the region.

Have US foreign policy moves in Central Asia been successful? Yes and no.

One bright spot is Iraq. Iraq was always the priority in “the war on terror”, not because the terrorists were there (they are now…) but because Iraq holds the world’s second largest oil reserves after Saudi Arabia. Many of Iraq’s oil fields also have the important advantages of being sweet crude (high quality), are shallow, and are under pressure, making Iraqi production costs very low – in the neighborhood of $10/barrel. For those who actually believe the US government’s marketing job of WMDs, “freedom”, etc. as a pretext for invading Iraq, please note the recent announced that Iraq’s oil resources are now “open for business” and up for bidding. Western oil companies such as BP, ExxonMobil, Chevron, and Royal Dutch Shell (RDS.A) stand to benefit handsomely in Iraq while at the same time boosting the country’s oil production by some 2-3 million barrels over the new few year. So, Iraq can be considered a US success story assuming security is maintained and the oil can reach the market. A big if, but time will tell.

The BTC can also be considered a success. It has operated fairly reliably, and has shown to be a fairly secure source of Caspian Sea oil. This was a huge project, and many people in the oil business doubted its success and completion. But it’s up and running today and survived Russia’s recent invasion of Georgia. That said, the BTC’s continued success is extremely dependent on maintaining security in the area.

Now it’s time to head to Afghanistan and take care of business over there. Boy-oh-boy is that going to be one tough nut to crack. The Afghan/Pakistani issue is so deep I can’t even begin to cover it in enough detail to do the subject justice. Those who believe the US motives in Afghanistan are simply “terrorism” or “freedom” should take note that the US fully supported and funded the Taliban when it was decided they were the best option with respect to getting the Central Asian pipeline built. Unocal sponsored the Taliban on trips to Houston to stay at 5-star hotels and visits to NASA. It was only later when the Taliban wouldn’t “play ball” that the US stopped their support and labeled the Taliban terrorists. Even the US installed Afghani President Hamid Karzai worked as an advisor and consultant to Unocal during the initial Central Asian pipeline feasibility studies.

So, US policies have had some successes in the region as far as oil is concerned. From a humanitarian aspect, well, I’ll leave that up to the reader to figure out on his or her own. From an economic standpoint, one would have to make a detailed analysis of military spending versus the economic benefits in order to come to any conclusions. Perhaps I will write an article on this some day, but for now, I’ll sidestep that question as well.

For the US, I am not such an idealist to think for one minute the symbiotic “Pentagon-Petroleum” relationship will change anytime soon. Further, as a realist, I also understand how important the game being played in Central Asia is. I am aware of the actions the US and other world powers are taking in Central Asia in order to acquire the energy reserves they need to power their economies. My eyes are wide open.

What I continue to struggle with is why the US directs so many resources and dollars toward these overseas strategies while at the same time almost completely ignoring what steps could be taken to reduce our foreign oil requirements by adopting some fairly simple and obvious policy changes. It, quite simply baffles me. Even a cock-sure trader hedges his bets now and again. The most amateur investor knows some diversification is prudent. So, why does the US continue oil centric policies which are certain to lead to more conflict, more debt, more trade deficits, and a weaker economy and currency?

Most readers are very familiar with my proposed energy policy, but I will add the link yet again in the hopes that someday, someone out there with a bit of power and influence will read it and make it happen.

So what does all this have to do with investing you ask? In a word: everything. Where can US investors put their money these days? Financials? Consumer cyclicals? Auto makers? I think not. Despite current low oil prices, the recent strength in the US dollar, and the subject matter of this article, I continue to believe the best opportunity for US investors is to participate in energy companies and to buy gold. Now, I know that some of you who read my articles earlier in the year and went out and bought my recommended stocks got a hurt, and hurt bad, right along with me and everyone else. I’m truly sorry, and feel bad if my advice caused you any pain (at least realize I felt the pain as well!). That said, let’s look at the 2008 returns for some of my picks:

- British Petroleum (BP): -36.1%

- Chevron (CVX): -20.7%

- ConocoPhillips (COP): -41.3%

- ExxonMobil (XOM): -14.8%

- Schlumberger (SLB): -57%

Not awfully bad, considering these returns (from this weekend’s WSJ) do not include the nice dividends some of these companies’ payout and the S&P500 was down 38.5% in 2008, its worst year since 1931. At the same time gold held up rather well, gaining 7% in the course of the year.

The bad news was some of my theme picks didn’t do well at all. Energy services, which at one point in 2008 were my “number one investment pick”, simply got hammered. Likewise, my advice to get into strategic metals via Vanguard Precious Metals (VGPMX) was a disaster as the stocks in this fund were sold off big time during the great leverage unwinding.

Making matters worse was the huge distribution VGPMX made at the end of the year which just infuriated me. I actually called Vanguard and asked them how a fund which lost over 60% for the year could possibly justify making a year end taxable distribution that equaled roughly 12% of the fund’s entire NAV?! I mean, if you sold enough to make such huge gains, why the hell is the fund down 60%? If you didn’t sell, and watched the stocks go down, why not sell the losers so that the losers and gainers cancel each other out so that no taxable distribution takes place? I was told I simply “didn’t understand”. They were right, I don’t! Seems to me even a moron could manage a fund better than that. The loss in the fund’s NAV I can understand. The huge year end distribution is simply inexcusable.

What I learned during the year is this: if a person wants to invest in precious metals, buy gold, take personal delivery of it, and bury it in the backyard and forget about it. Sure, people flock to the US dollar in times of crisis, but did anyone see the action in US treasuries last Thursday and Friday, as well as the headline in Barron’s this weekend? The financial mismanagement by the US government, Treasury, and Federal Reserve combined with the lack of a strategic long-term comprehensive energy policy must lead to a long-term weakening of the US currency. So, buy oil, buy gold. When inflation comes back, it will come back very quickly and these hard assets will once again take off like a rocket. I mean, how can the economy not re-inflate with the Federal Reserve printing US dollars as fast as the presses will print them?

My picks for 2009 are as follows: XOM, BP, CVX, COP, SLB and gold bullion, in particular American Eagles and Canadian Maple Leafs.

Goodbye 2008! Indeed, very soon we will be saying goodbye to George W. Bush as well. Let’s all hope that 2009 will be better than 2008. It won’t take much! Let’s also hope that the new administration hedges its foreign policies bets with a bet on the American people and what we can do at home by enacting a strategic long-term comprehensive energy policy. In the meantime, buy Kleveman’s book The New Great Game, enjoy, and learn. The last paragraph of the book sums up my feelings perfectly.

========================================

Get The Book: The New Great Game – by: Lutz Kleveman

========================================

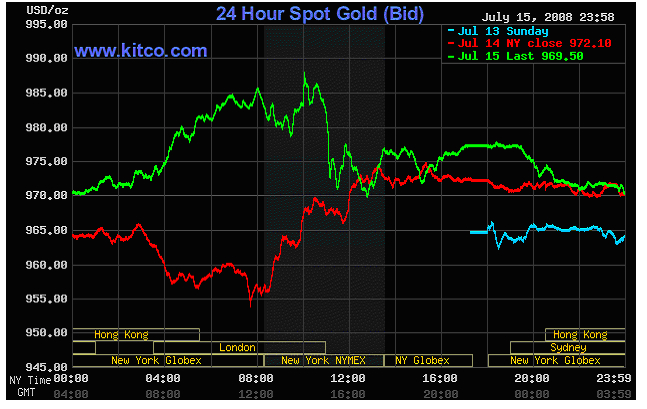

Gold Due for a Pullback; Silver Approaching Resistance- Seeking Alpha

I like gold here as an investment going forward- I just liked it a whole lot better a few weeks ago. I think we at the top of this wedge formation and due for a pullback and the RSI could come back to the previous high around 50. That would be very constructive and bullish allowing this metal to bust through 900 on its next run. While I don’t have a specific price target for where I think it will correct to, the 20-day moving average seems like a reasonable guess.

Obviously if tensions heat up in the Middle East this could fuel another rise in gold and all bets are off. However I’ve learned in the past not to underestimate gold’s ability to correct quickly so I took my profits on Friday and will enter on a pullback. I wanted to be flat going into next week as anything can happen when all the fund managers get back from vacation.

Silver has been up 6 straight days and is fast approaching resistance. I would rather it pause here and gather some strength to possibly break through the 11.75 area instead of shooting straight up using up all it’s firepower. Use any further strength to unload positions and wait for a pullback to add or establish new positions.

=============================================

Profiting From Bernanke’s Super-Fed and Obama’s Newer Deal – Seeking Alpha

By: Naufal Sanaullah of The Gotham Fund and Dorm Room Derivatives

The historic wealth destruction of 2008 was obviously deflationary. Defaults strip away wealth. Institutions respond by selling assets to raise capital. Widespread deleveraging leads to supply expansion in assets and contraction in money and credit (i.e. deflation).

Nevertheless, the response has been unprecedented in its own merit. Government debt held by the public was $5.51 trillion when September began; by the end of 2008, it had risen to $6.37 trillion. The more than $1 trillion expansion in Treasury borrowing surely partially serves to offset the $438 billion budget deficit. But what about the additional half a trillion dollars?

On September 17, the Treasury announced the creation of the the “Supplementary Financing Account” in the Federal Reserve. This is a capital reserve in Fed financed by the Treasury selling new debt and it greatly expands the Federal Reserve’s balance sheet, albeit stealthily. The excess capital is trapped in this Fed account and does not reach currency in circulation. As of January 2, $259 billion is in this Treasury-financed cash pool and counting the Treasury’s “General Account” with the Fed, there is a total of $365 billion sitting at the Fed. The capital itself is money borrowed by the public, so its immediate net effect is deflationary.

On top of that, the Fed in an unprecedented gesture has started incentivizing excess bank reserve deposits by issuing interest on these holdings. Rather than being lent out, liquidity provided to banks by the Fed is thus trapped as it earns interest deposited at the Fed. The Fed is essentially issuing debt, and banks are engaging in what amounts to be a dollar-based Fed vs. interbank carry trade. Banks borrow money from the Fed, deposit them back into the Fed (use borrowed dollars to purchase Fed debt), and profit from the differential between the fed funds and overnight rates (profit off of the difference between the interest rates offered by Federal Reserve and other banks).

Less than $40 billion a year ago, the excess reserve deposits held by the Federal Reserve has ballooned to $860 billion. The banks can also deposit printed money into a Fed category called “Deposits with Federal Reserve Banks, other than reserve balances,” which is what the Supplementary Financing and General Accounts also fall under.

The “Other” subsection of these deposit accounts, which can be construed to represent bank deposits, has increased from $281 million in September to $15 billion today. Both the reserve and non-reserve deposits comprise another huge pool of excess liquidity on the Fed’s balance sheet that doesn’t immediately affect circulated currency.

Another Fed-induced cash trap has been in the form of increased reverse repurchase agreements, which are up to $88 billion. Reverse repurchase agreements are the offering of collateral in exchange for a cash loan. The Fed has utilized reverse repurchase agreements in its liquification of banks. It buys off toxic defaulting assets in exchange for cash and immediately reclaims the cash by selling the banks T-bills. The Fed printed money to pay for these T-bills, so there is excess liquidity that is trapped in time-sensitive debt. But why would the Fed be taking liquidity away from the system?

The Fed’s balance sheet suggests it has been cranking the printing presses like mad. Fed liabilities have expanded to $2.26 trillion, up over 140% since September. However, currency in circulation is up only 7% in that same time period. Where is this “trapped” $1.37 trillion? The answer is the Fed has confined it into temporary cash pools, whether in the Supplementary Financing Account or excess reserve deposits or in time-sensitive T-bills. The Federal Reserve seems to be sequestering all of this cash to buy time for the Treasury to finish its funding activities. What is scary is this wave of future bailout funding is probably not even close to what will be needed for Obama’s infrastructure and stimulus spending, which will be comparable only to FDR’s and will be liquidity injected directly into the economy.

But who is going to keep funding this expansion Treasury debt issuance? The American public is broke and cannot offer its capital in return for terrible yields. Foreign nations don’t have the means or will to continue financing our debt. Commodity prices have collapsed, cutting deeply into foreigners’ export revenues. Oil is down from highs around $150/barrel this past summer to around $40/barrel now.

According to the CIA World Factbook, China has a $6 billion budget surplus. However, it announced a $585 billion economic stimulus package in early November to be invested by the end of 2010. The Chinese government agreed to provide only $170 billion of the the funds, in an effort to prevent an unreconcilable deficit. How will China raise the other $415 billion for continuous use until the end of 2010? Surely, local governments and private banks and businesses can’t finance such a large package in the midst of a historic recession.

The only reserve China can tap into to finance its stimulus package is its $1.9 trillion foreign exchange reserves, $585 billion of which is in US Treasury securities. Also, according to the Guangzhou Daily, in mid November, the People’s Bank of China began an effort to increase its gold reserves from 600 tons to 4500 tons to diversify risk held by its huge dollar debt reserves. Financing its stimulus package and gold purchases would require selling Treasury securities, but becoming a net seller of US debt could have disastrous economic, political, and even militaristic consequences for China, so it will be interesting to see how events unfold. What seems for certain, however, is that China can no longer purchase more American debt to finance the US Treasury (and consequently the Fed).

This is a problem echoed by the rest of the big creditor nations. After China, the biggest holders of American debt securities are Japan, the UK, Caribbean banking centers, and OPEC nations. Japan is facing enormous headwinds as its quality-focused exports are suffering massive demand destruction as its consumers abroad lose wealth at epic proportions in the economic crisis. Japan was a net seller of US Treasuries in 2008 and with the current wealth destruction, it is highly unlikely it will switch to a net buyer of American debt. The British demand for American debt represented Middle Eastern oil-financed investment, but with oil prices collapsing, it will be next to impossible for this proxy demand from the UK to rise and finance additional debt.

The demand for US debt by Caribbean banking centers is because of their tax laws and because of the dollar’s status as the international reserve currency. As the credit crunch leads to liquidity destruction in Caribbean banks and the dollar slowly loses its reserve status, these tax haven banking centers will no longer be able to buy additional US debt. OPEC nations’ US debt demand, similar to the UK’s, is tied to Middle Eastern oil revenues financing American consumption (of their oil exports). As oil prices tank, as will OPEC nations’ economies and they too will have no wealth to buy up more American debt.

Bernie Madoff is well-recognized as the biggest Ponzi scheme in history, at $50 billion. I beg to differ with that claim. The United States has financed debt with debt since the late 80s, when its external debt/GDP broke the 0 mark. Since then, it has risen to over 100% of its GDP (which in itself is quite artificially inflated because of manipulated hedonics-adjusted inflation figures), and now stands at $13 trillion. That is what’s called a debt bubble. Bernie who?

But the debt bubble appears ready to collapse. The literal pyramid scheme is finally running out of investors, and many Treasury ETFs (like SHY, TLT, IEF, and IEI) are showing classic parabolic topping patterns and the next few weeks should confirm or deny my suspicions. Interest rates are at an obvious floor at zero, so there is nowhere to go but up. That means bond prices have nowhere to go but down, and the way bubbles burst, the falling prices will cascade into more selling until the debt bubble deflates and all the spending is financed by quantitative easing. The minute the Treasury finishes its current funding activity, the debt bubble will begin its collapse. Judging by gold backwardation (discussed later) and the bearish charts on the bubbly debt ETFs, I think the debt monetization and dollar devaluation will begin within the next six weeks.

With an insolvent public and no foreign demand for Treasuries, the Federal Reserve will monetize debt to finance its continued bailouts and economic stimulus. This is purely created capital pumped right into the system. This is not anything new for the Fed– for the past two decades, it has kept interest rates artificially low and created massive artificial wealth in the form of malinvestment and debt-financing. In the past, the Fed has been able to funnel the inflationary effects of its expansionary monetary policy into equity values with its low rates, which discourage saving, causing bubble after bubble, in the form of techs, real estate, and commodities. The excess liquidity (the artificial capital lent and spent because of low interest rates and debt financing) was soaked up by the stock market, which gave the appearance of economic growth and production. With inflation being funneled into equity and real estate over the last two decades, illusionary wealth was created and the public remained oblivious to the inflationary risk and the much lower real returns than nominal.

Now that the “artificial wealth bubble” being inflated for the past two decades is finally collapsing, one of two scenarios can occur: capital destruction or purchasing power destruction. Capital destruction occurs when the monetary supply decreases as individuals and institutions sell assets to pay off debts and defaults and savings starts growing at the expense of consumption. This is deflation and the public immediately sees and feels its effect, as checking accounts, equity funds, and wages start declining. Deflation serves no benefit to the Federal Reserve, as declining prices spur positive-feedback panic selling and bank runs, and debt repayments in nominal terms under deflation cause real losses.

Purchasing power destruction is much more desirable by the Fed. Its effects are “hidden” to a certain extent, as the public doesn’t see any nominal losses and only feels wealth destruction in unmanageable price inflation. It breeds perceptions of illusionary strength rather than deflation’s exaggerated weakness. The typical taxpayer will panic when his or her mutual fund goes down 20% but will probably not react to an expansion of monetary supply unless it reaches 1970s price inflationary levels. In addition, the government can pay back its public debt with devalued nominal dollars, which transfers wealth from the taxpayers to the government to pay its debt. Inflation is essentially a regressive consumption tax, which the government wants and the Fed attempts to “hide”. Not only is the Treasury’s debt burden reduced, but the government’s tax revenues inherently increase.

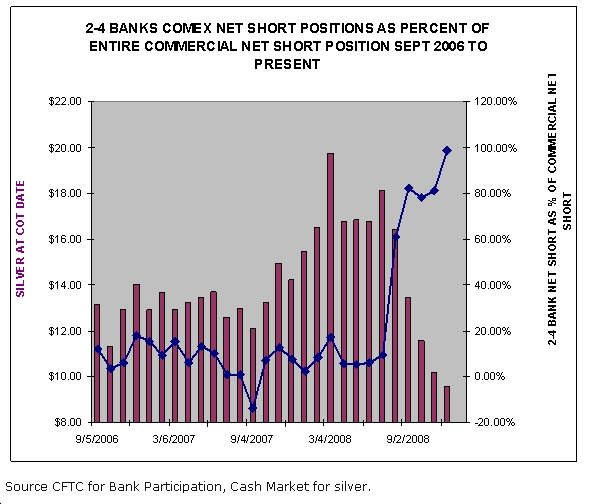

The Fed, in an effort to minimize inflationary perception, has for the last two decades supported naked COMEX gold shorts to keep gold prices artificially low. The Fed, as well as European central banks, unconditionally supported these naked shorts to deflate prices and stave off inflationary perception, as gold prices stay artificially low. This caused gold shorts to be “guaranteed” eventual profit, by Western central banks offering huge artificial supply whenever necessary, causing long positions in gold to be wiped out by margin calls and losses.

Now that the economy is contracting, the Fed won’t be able to funnel the excess liquidity into equities or other similar assets. It also can’t allow the excess liquidity of today, which is different in both its size (already $1.37 trillion) and nature (it is printed “counterfeit” money and not malinvested leveraged and debt-financed capital), to be directly injected into the economy. That would prove to be immediately very inflationary, as more than three times the money is chasing the same amount of goods, technically leading to 300% price inflation. These figures are strictly based on monetization of the Fed’s current liabilities, not including any future deficit spending (which is sure to dramatically increase, especially with Barack Obama’s policies), the American external debt, or unfunded social programs that need payment as Baby Boomers retire.

In order to funnel the excess liquidity into a less harmful asset, the Fed appears to be abandoning its support for gold naked shorts, causing shorts to suffer their own margin calls and cause rapid price expansion in gold. On December 2, for the first time in history, gold reached backwardation. Gold is not an asset that is consumed but rather it is stored, so it is traditionally in what is called a contango market. Contango means the price for future delivery is higher than the spot price (which is for immediate settlement). This is sensible because gold has a carrying cost, in the form of storage, insurance, and financing, which is reflected in the time premium for its futures. Backwardation is the opposite of contango, representing a situation in which the spot price is higher than the price for future delivery.

On December 2, COMEX spot prices for gold were 1.99% higher than December gold futures, which are for December 31 delivery. This is highly unusual and it provides strong evidence to the theory that the Fed is abandoning its support for gold shorts. Backwardation represents a perceived lack of supply (in this case, the artificial supply the Fed would always issue at strategic times no longer existed), causing investors to pay a premium for guaranteed delivery. On May 21, when crude oil futures reached contango, I started waiting patiently for the charts to offer a short sell trigger because the contango represented a supply glut relative to perception and current pricing. Oil was priced at $133/barrel at that time and six weeks later, on July 11, oil topped at $147, and six days later crude broke its 50DMA on volume and triggered a large bearish position against commodities that resulted in some of my most profitable trades last year.

I consider gold’s backwardation as a similar leading indicator to the opposite effect—a dramatic increase in prices. Crude began its most recent backwardation in August 2007 at around $75/barrel and increased dramatically over the next nine months to $133/barrel at contango levels. Backwardation, especially in the case of gold prices, reflects a lack of supply at current prices and is very bullish.

But why would the Fed abandon its support for naked COMEX shorts? What makes gold such a desirable asset to attempt to direct excess liquidity into? The unique nature of gold and precious metals provides its desirability in this Fed operation. Gold has little utility outside of store of value, unlike most commodities (like oil, which is consumed as quickly as it’s extracted and refined), so its supply/demand schedule has unusual traits. Most commodities and assets go down in price as the public loses capital, because the public has less to consume with and that is reflected in demand destruction that leads to price deflation. Gold is not directly consumed and its industrial use and consumer demand (jewelry) is at a lower ratio to its financial/investment demand than almost any other asset in the world.

As a result, gold is relatively “recession-proof,” as evidenced by its relative strength in 2008. Gold prices rose 1.7% last year, which is quite spectacular considering equity values went down 39.3%, real estate values went down 21.8%, and commodity prices went down 45.0% in the same period (as determined by the S&P 500, Case-Shiller Composite, and S&P Goldman Sachs Commodity Indices, respectively). Because gold is not easily influenced by consumer spending, highly inflationary gold prices don’t do any direct damage to the public and are a good way to funnel excess liquidity without economic destruction.

Federal Reserve Chairman Ben Bernanke is a staunch proponent of dollar devaluation against gold and is very supportive of President Franklin D. Roosevelt’s decision to do so in 1934. In the past, manipulating gold prices to artificially low levels was beneficial because it prevented capital flight into a non-productive asset like gold and kept production, investment, and consumption high (even if it were malinvestment and unfunded consumption).

Bernanke’s continued active support of gold price suppression would lead to widespread deflation that would collapse equity values and cause pervasive insolvencies and bankruptcies. Insolvency in insurers removes all emergency “backups” to irresponsible lending and spending, which would surely ruin the economy. Bernanke’s plan seems to be to devalue the dollar against gold with huge monetary expansion, causing equity values to rise and economic stabilization. I’ve heard estimates of 7500 and 8000 in the Dow Jones Industrial Average as being minimum support levels that would cause insurers and banks to realize massive losses, causing widespread insolvencies in them and other weak sectors like commercial real estate that would irreversibly collapse the economy.

This gold price expansion, set off by the massive short squeeze, will continue until gold prices reflect gold supply and Federal Reserve liabilities in circulation. The “intrinsic” value of gold today (called the Shadow Gold Price), calculated dividing total Fed liabilities by official gold holdings, is about $9600/oz, compared to around $865/oz today. This gold price calculation essentially assumes dollar-gold convertibility, as is mandated by the US Constitution and was utilized at various periods of American history. The near-term price expansion in gold, mainly led by abandonment of gold shorts and the first traces of inflationary risk, should show $2000/oz by the end of this year. As the leveraged deals from the pre-crash credit craze mature, with the majority of them maturing in 2011-2014, there will be more monetary expansion for debt repayment, which will structurally weaken the US Dollar (which is inherently bullish for gold) and will also provide new excess liquidity to be funneled into precious metals. This leads me to believe gold will be worth $10,000/oz by 2012.

The US Dollar’s strength as the equity and commodity markets collapsed was due to deleveraging and an effect of the Fed’s temporary sequestration of dollars, taking dollars out of supply. That is over. Oil seems to be putting in a bottom on strong volume, no one is left to buy any more negative real yield securities the Treasury is issuing, and gold has started looking very bullish.

But a good speculator always considers all situations. Even if deflation is to occur, which I see as next to impossible, gold prices should still rise to $1500/oz levels next year, because it has shown relative strength as one of the most viable assets left to invest in. In addition, the short squeeze occurring in gold will provide substantial technical price expansion, even in the absence of dollar devaluation. Because of this, I suggest gold as an investment cornerstone for the foreseeable future.

I see the market breaking down from these levels to about the November lows, starting on Monday. Commercial real estate stocks like Simon Property Group (SPG), Vornado Realty Trust (VNO), and Boston Property Group (BXP) should lead the down move, as well as insurers like Allstate (ALL), Prudential (PRU), and Hartford (HIG), banks like Goldman Sachs (GS) and Morgan Stanley (MS), and retailers like Sears Holdings (SHLD). I recommend short positions (including leveraged bearish ETFs like SRS and FAZ) and buying puts against these stocks for the very near term. If the market indeed breaks down but shows bouncing/strength around 7500-8000 in the Dow Jones, that would confirm to me that the Fed is able and willing to inflate its way out of this crisis and I will sell my bearish positions and buy into bullish gold positions.

Because in inflation the dollar is devalued, I am a proponent of owning bullion and avoiding gold ETFs, but I do believe gold and gold miner stocks will provide great returns over the next few years. Royal Gold (RGLD), Iamgold (IAG), Jaguar Mining (JAG), Anglogold Ashanti (AU), Newmont Mining (NEM), Randgold (GOLD), Goldcorp (GG), and Barricks (ABX) are among my favorite gold equities at this early stage in the process. Their charts are all quite bullish and look to see much more upside. I believe gold will pullback for a few weeks as the market continues lower and deleveraging occurs, but like I said, I don’t believe the Fed will allow the markets to breach its November lows. If indeed deflation wins out and the Fed can’t prevent equity value collapse, I will just hold on to my aforementioned bearish positions and trade in particularly those securities for the foreseeable future, and I suggest you to do the same.

Literally the only thing that I find suspicious in all of this is the fact that I see so many inflationists out there and I even see commercials on TV about precious metals. I usually like to stay contrarian to the public, which I consider irrational and wholly incompetent. But this enormous debt and monetary expansion is a structural problem that common sense may provide better insight for than the most complex of models and theories.

I leave you with this, a quote from Fed Chairman Ben Bernanke about President Franklin D. Roosevelt’s 1934 Gold Reserve Act, which was the greatest theft of wealth I’ve aware of in American history:

“The finding that leaving the gold standard was the key to recovery from the Great Depression was certainly confirmed by the U.S. experience. One of the first actions of President Roosevelt was to eliminate the constraint on U.S. monetary policy created by the gold standard, first by allowing the dollar to float and then by resetting its value at a significantly lower level … With the gold standard constraint removed and the banking system stabilized, the money supply and the price level began to rise. Between Roosevelt’s coming to power in 1933 and the recession of 1937-38, the economy grew strongly.”

My predictions: gold at $2000/oz by the end of the year and $10,000/oz by 2012 and silver at $30/oz by the end of the year and $130/oz by 2012.

Disclosure: Long SRS, SRS calls, TBT, TBT calls, gold bullion.

===============================================

Please Feel Free To Comment on any of these articles! – jschulmansr