Today’s action: Gold opened down by a few dollars and now has reversed itself and is cusrrently up $7-10 oz. Based off of chart formations it would appear that Gold is breaking out to the upside and getting ready to challenge the $900 level, If it can break that then we are set up for a test of the $950-$975 level. If it fails here, a pullback to the $800 level (support base) will probably occur. Today’s articles include one about a new 2yr gold price cycle that appears to be forming. Next some questions answered about the markets for 2009. Finally a special report from Gold World about Gold Backed Banking. Enjoy and good investing! – jschulmansr

Gold’s 2-year cycle – MineWeb

A Mineweb reader has noticed a recent two-year cycle for gold price behaviour which, if it continues will likely give some guidance to price movements this year and next.

By: Joseph Cafariello

EDMONTON, CANADA –

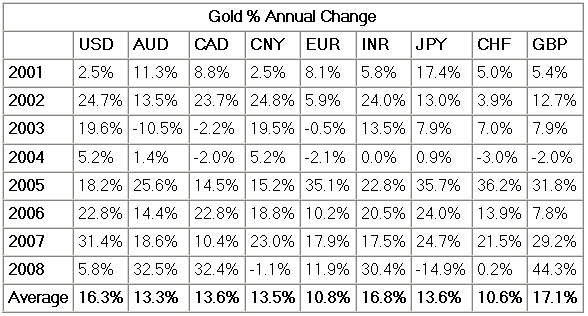

There seems to be a two-year cycle in the gold price which has been repeating itself since about 2004. The even years follow one pattern, while the odd years follow another pattern. The even years tend to reach exaggerated extremes to the upside and to the downside on a percentage basis, while the odd years tend to be a little calmer with less volatility.

For example, 2008 went very much like 2006, with exaggerated highs reached in the spring of each year, and a late start to the traditional autumn-winter-spring upswing, which began around October/November of 06 and 08. On the odd-number side, 2007 went much like 2005, with moderate highs reached in May of each year, and an early start to the traditional autumn-winter-spring upswing, which began around August/September of 05 and 07.

If this is indeed a reliable cycle, we can expect 2009 to be much like 2005 and 2007 all throughout the year. The first half of 2009 should see gold follow the same pattern as the first halves of 2005 and 2007. In the springs of 05 and 07, gold kept hitting its head against the previous year’s high all throughout the spring. More than once during the spring of 2007, gold topped out at about $690, coming to within about 5% of the 2006 high of $735. Similarly, the spring of 09 should see gold hitting its head against 2008’s high of $1,035, coming to within 5% of it, or up to about $985. That will be the high for the first half of 2009 at around the beginning of May, though this will not be the high for 2009 as a whole.

Given the odd-number year pattern, we might also expect the back half of 2009 to be much like the back halves of 2005 and 2007. In both 2005 and 2007, the summertime pull-backs were modest, and the autumn-winter-spring upswings started early, at around August/September of 05 and 07. The latter half of 2009, then, should see a modest summer-time pull-back of about 5% to 7% of its spring 09 high, taking gold down from $985 in May 09 to about $925 by August 09. However, the low for 2009 will still be the upcoming January low of $800, which is now only about a week or two away. The lows of January 2005 and January 2007 were also “the” or “close to the” annual lows for those years. So the low of 2009 will be at around $800 in January.

The high for 2009 will come in December. The traditional autumn-winter-spring upswing in 2009-10 will be much as it was in 2005-06 and 2007-08, with an early start. The year-end run for 09 will begin around August or the beginning of September, jumping from about $925 in Aug/Sep 09 and rising steadily until the end of December 09. The annual highs for 2005 and 2007 were hit in or near December of each year, and each high was about 20% higher than the average of their first halves. Thus, the annual high of 2009 will be hit in or near December, and will be 20% higher than the average of its first half, putting the 2009 high at about $1,150 in December.

The traditional autumn-winter-spring upswing, however, will certainly not end in 2009, but will spill over into the spring of 2010 much as it did in the springs of 2006 and 2008. The high in the spring of 2008 was about 40% higher than high in the spring of 2006. Hence, the high in the spring of 2010 will be about 40% higher than 2008’s high of $1,035, putting gold at about $1,450 in the spring of 2010. Then, the summertime pull back of 2010 will be just as stark as were the summertime pullbacks of 2006 and 2008.

And so the two-year cycle will continue, where even-number years follow a pattern of extremes, while the odd-number years are calmer, but with a nice upward kick at the end. This two-year cycle with even-number years on the extreme side and odd-number years on the moderate side will continue until the commodity boom is over (say around the year 2030, when the populations of China and India finally achieve a 75% middle-class), and until the US dollar recovers at around the same year (2030), when the rest of the world will be looking to the US as a nice place to shop given its then-to-be dirt-cheap dollar.

The above comment was contributed by Mineweb reader Joseph Cafariello who describes himself as “A raving gold bug and proud of it”

==========================================

2009 Market Q&A: Four Questions Answered – Seeking Alpha

Source: Eric Roseman of The Sovereign Society

By Eric Roseman

Over the last several weeks I’ve received numerous questions from Sovereign Society subscribers, including individuals who frequent our daily blog.

As we start 2009, I thought this would be an ideal forum to collect some of these important questions and attempt to give you my best conclusions. I can’t reprint all of these inquiries; but I’ve compiled several excellent questions from our members.

Overall, I don’t like forecasting. I generally believe it’s a total waste of time and most consensus estimates ahead of 2008 ended in the basement with the majority of analysts dead wrong about the economy, the market and just about everything else.

I have to admit that I never expected the markets to crash, the banking system to go bust or the dollar to skyrocket in the midst of the worst financial crisis in 75 years. To be fair, I think most pros failed to make accurate predictions.

Question: I’m a retired investor living on income. Prior to the big rally in Treasury bonds, I held most of my savings in short-term Treasury’s and bank term deposits. But with short-term rates under 1% and government bonds yielding a pittance, I’m nervous. What should I do to supplement my income?

Comment: This is perhaps the most challenging environment for retirees in more than a generation. With money-market funds yielding almost nothing, Treasury bonds yielding around 2% and bank CDs paying under 1%, retirees must supplement their income.

My advice is to take a small portion of your savings, say 20%, and scatter that sum across a dozen or more investment grade corporate bonds. I emphasize “investment grade” and not junk debt. Investment grade debt includes anything rated BBB or better in my book and, to make it easier, I would stick to issues rated A- or higher.

The Dow Jones Corporate Bond Index now yields 6.90% – down from its post-crash high yield of 8.87% in early  October. Still, investors can tap into non-financial bonds like IBM, Johnson & Johnson (JNJ), Wal-Mart (WMT) and Kraft Foods (KFT) – all paying 5.5% or more. Or, look at corporate bonds issued by America’s largest banks, including JPMorgan Chase (JPM), Goldman Sachs (GS), Wells Fargo (WFC) and US Bancorp (USB). These banks won’t default.

October. Still, investors can tap into non-financial bonds like IBM, Johnson & Johnson (JNJ), Wal-Mart (WMT) and Kraft Foods (KFT) – all paying 5.5% or more. Or, look at corporate bonds issued by America’s largest banks, including JPMorgan Chase (JPM), Goldman Sachs (GS), Wells Fargo (WFC) and US Bancorp (USB). These banks won’t default.

A good strategy to keep things simple is to buy a laddered portfolio of corporate bonds ranging from two years all the way to seven years. This should at least give your nest egg a boost and if you feel comfortable with this formula, then increase your position to say 35% of your portfolio. But remember, don’t go whole-hog; at some point over the next 12 months, perhaps later, Treasury bond prices will get smashed and long-term rates will head higher as the government expands credit to the moon. Keep your powder dry.

Question: Do you think we’ll avoid another Great Depression? Despite all the money thrown at the markets since late 2007 we’re still in the midst of a severe credit contraction and the global economy has literally fallen off a cliff since October.

Comment: I think we’ll avoid another Great Depression but only because government will nationalize or partially nationalize key industries. Without government intervention, the free market would have resulted in massive failures and a total collapse of the banking system and the broader global economy. There’s no doubt in my mind that the government made a big mistake not rescuing Lehman Brothers last September. Once you’re bailing out major banks, then do it right. But in all honesty, we don’t know what transpires behind the Fed’s walls or the Treasury’s. There’s some crazy buddy system in progress with special interests influencing government policy. The government doesn’t give a damn about you or me. What they care about is protecting their interests. That’s why we must protect our assets and, in the end, I believe gold will triumph above all paper money, especially against the dollar.

I don’t advocate government intervention; but these are not normal times and the consequences might have resulted in the death of capitalism and perhaps the emergence of a new social order, similar to what occurred in post-Weimar Germany in the 1920s. Harsh economic times usually result in a new socio-economic regime. If the Fed and Treasury fail to rescue the credit system, then we might face similar consequences. The world as we know it will come to an end.

It’s hard to know exactly what goes on behind the Federal Reserve’s closed doors and at the Treasury’s. Thus far, government efforts have been bold since the October crash, including major central banks worldwide. Major credit indicators have indeed improved since November but the housing market – the crux of the crisis – is still in a freefall. Housing must stabilize before this severe recession ends.

In my eyes, it seems that bailouts and backstops are not addressing the real problem; most TARP money is ending up in bank coffers again and, in most cases, these institutions aren’t lending. The core of this credit crisis lies with the consumer and with housing. If you’re going to fork out several trillion dollars to fix or remedy this crisis then give the money to the consumer – not the banks. The consumer is in a severe bear market with personal assets plummeting over the last 18 months, including real estate, stocks, most bonds and now, possibly his or her job might be next on the chopping block.

Give consumer households $50,000 or more and allow them to clean-up their busted balance sheets, keep their homes (service mortgages) and pay off installment debt. You might not agree with me and, in all fairness, it’s against the tenets of the Sovereign Individual; but what good will all this money do if it’s basically squandered by government and ending up in the pockets of reckless bankers again? I have serious doubts about how the government is dealing with this crisis and I don’t think Obama’s spending package will help much at all despite perhaps growing the economy for a few quarters.

Question: What about the banks? With governments now standing behind their biggest financial institutions, is the worst over?

Comment: The global banking system, for all intents and purposes, is effectively bust or bankrupt. This is especially the case in the United States, Europe and, to a lesser extent, in Japan. More than a dozen emerging market banks are totally bust, including Iceland, the Baltics, Hungary, Romania, Bolivia, Ukraine, Ecuador, Argentina, etc. Not a pretty picture.

I think we’re more than 75% through the worst at this juncture. Governments now stand behind the largest banks in each country and, in some cases, even guarantee entire deposits until 2010 (e.g. European Union). I wouldn’t worry about the largest banks failing at this point. The worst is now behind us.

Question: I know you’re a big gold bug, but isn’t the euro a strong currency and do you think it’s a better hedge against the dollar than gold? Is it too late to purchase gold coins and, if not, where would you suggest I buy coins?

Comment: I have absolutely zero faith in the U.S. dollar and other currencies, including the euro or yen. In the end, all currencies will decline vis-à-vis gold and, in fact, since 2005 the world’s currencies have been losing their relative value to gold bullion. Despite big moves by the yen and euro over the last several years, they pale against gold.

Increasingly, the average man in the street will realize that paper money is not protecting his purchasing power and will revolt against fiat money. At The Sovereign Society, we’ve driven home this message since our first year of publication in 1997. Gold is the only asset in this world that isn’t someone else’s liability; with U.S. interest rates effectively at 0%, paper money now competes with gold, which also pays 0% interest. In a zero percent world, which asset would you rather own? I think the answer is obvious.

The government’s enormous spending plans to rescue the financial system and bailout almost every ailing industry  assures dollar destruction because the Fed is now on course to print money like never before to quash deflation. We all better hope and prey that the Fed can drain excess bank liquidity very quickly when this credit crisis ends. If not, we’ll have some serious inflation – much worse than what we saw prior to July 2008.

assures dollar destruction because the Fed is now on course to print money like never before to quash deflation. We all better hope and prey that the Fed can drain excess bank liquidity very quickly when this credit crisis ends. If not, we’ll have some serious inflation – much worse than what we saw prior to July 2008.

I think every investor should hold at least 10% of his assets in physical gold. This means coins, wafers or bars. Getting gold coins today is difficult because the U.S. Mint has stopped selling Eagles since last summer while other dealers are complaining about tight supplies amid booming investor demand. I suggest KITCO or First Federal Coin Corporation.

Also, I would not hold or store all of my physical gold at my home domicile. I strongly suggest parking some of your gold in Switzerland, too. Remember, you must report assets outside of the United States and Canada.

I’m convinced we’ll see some sort of government confiscation of gold again just like we did in the 1930s. Back then, FDR did allow Americans to hold a maximum of 100 ounces. I’m not so sure the next confiscation will be so generous.

I hope you found this helpful.

===============================================

2009 Gold Outlook – Gold World

How To Invest in Gold in 2009

By Luke Burgess

The investment markets are yielding to the fact that the global economy will remain weak for the better part of 2009.

As a result, investors will continue to seek safe havens.

Under normal conditions, these safe haven investments would include land and real estate. These assets have intrinsic value; or in other words, their value will never fall to zero. But with falling prices, investing in real estate is out of the question for most people right now. And there’s little doubt that investors will look elsewhere for safety against financial crisis.

The best safe haven asset in the world right now is still gold because it is never considered to be a liability.

And we believe that safe haven investment demand will drive gold prices during 2009. With this in mind, we would like to present a broad overview of Gold World‘s 2009 gold outlook. But before we get into that, let’s review what happened to gold prices in 2008.

Gold Was One of the Best Investments of 2008

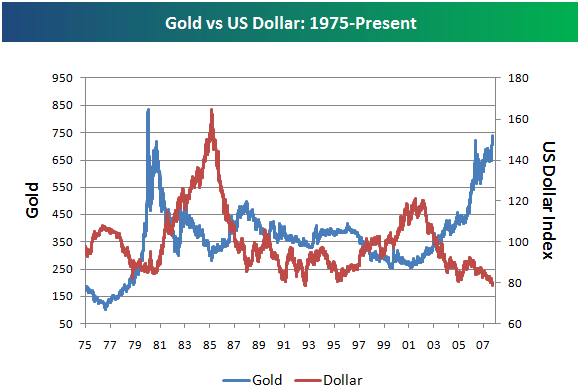

In March 2008, gold prices hit a record high of $1,033 an ounce as the gold bull market entered its seventh year of life. This was followed by a normal 18% correction, which drove gold prices back down to $850 an ounce.

Gold prices subsequently rebounded and were once again closing in on the $1,000 level in mid-July. At the same time, however, the fundamental and psychological effects of the slowing housing and credit markets were just beginning to devalue significantly the investment markets across the board.

As a result, many long gold positions had to be sold in order to cover losses from investments in other markets. Over the next several months, this forced selling pressure pushed gold prices down.

Gold prices were also held down during the second half of 2008 as the U.S. dollar enjoyed a +20% rally. Foreign governments, institutions, and banks began buying the U.S. dollar, which despite a legion of problems continues to be the world’s most important reserve currency, as a hedge against domestic economic turmoil.

These factors contributed to a significant drop in the price of gold, which officially bottomed out for the year at an intraday low of $683 an ounce in October 2008.

Gold prices have subsequently bounced off of the $700 level as major selling has dried up, and fresh buying has come into the market.

Despite three 20% corrections and serious deflation in the market, gold exited 2008 with a positive 5.4% gain for the year. Although subtle, this gain outperformed every major equity index and commodity in the world. Here are just a few examples…

Index/Commodity

|

Percent Change During 2008

|

Dow Jones

|

-34% |

NASDAQ

|

-41% |

S&P 500

|

-39% |

| TSX |

-35% |

| TSX Venture |

-74% |

Oil

|

-55% |

Silver

|

-23% |

Copper

|

-54% |

| |

|

Gold

|

+5%

|

This made gold one of the best investments of 2008.

And the 2009 gold outlook looks just as strong.

Gold’s 2009 Outlook

Despite a bit of downside in the immediate future, we expect gold to have a stellar year.

Global economic turmoil and deflation will undoubtedly continue to influence gold prices in the near-term. A short-term pullback in gold prices from current levels to $800—maybe even a bit lower—is not out of the question. However, we expect gold prices to break new records during 2009.

For our current perspective, we expect gold prices to reach as high as $1,300 during 2009, which would be a profit of over 50% from current levels.

Gold prices in 2009 will be supported more heavily by supply/demand fundamentals than in the previous years of this gold bull market.

As we’ve previously discussed, during the third quarter of 2008, world gold demand outstripped supply by 10.5 million ounces. This deficit was worth $8.5 billion and was the largest supply/demand deficit since the gold bull market of the 1970s.

Official 4Q 2008 world gold supply/demand figures will be calculated and reported later this month. Gold World will report them to you when the data is released.

In the meantime, though, all estimates suggest that there will be another very large deficit in world gold supplies from the fourth-quarter, with investment demand continuing to drive the market.

We expect that a continuing surge in investment demand could push gold prices as high as $1,300 at one point during 2009.

There will likely be a bit more volatility in the gold market in 2009 as more and more speculators come into the market. It is likely that the gold market will experience three or four price peaks (selling points) during 2009.

How to Invest in Gold for 2009

As we expect a near-term drop in gold prices as a result of continuing deflation, we are advising our readers to hold off on any physical gold buying for the immediate future. As previously mentioned, gold prices could dip back down to $800 before recovering again.

Nevertheless, we expect 2009 to be another great year for gold investors.

Good Investing,

Luke Burgess and the Gold World Research Team

www.GoldWorld.com

=================================================

Gold World Special Report – Gold Backed Banking

Special Report – Here’s How To Get Your Own Copy – Simply Subscribe

January, 2009

Gold Backed Banking

It’s a wonder Americans aren’t rioting in the streets.

Not including the $700 billion blank check issued to the banks and signed by the US taxpayer, the sum of liabilities assumed by the US government from the finance industry in the past 6 months alone exceeds 50% of the GDP.

Despite this unprecedented government intervention, the solvency of other every commercial and investment bank is still at stake!

Recognize this all-but-forgotten quote?

“The central bank is an institution of the most deadly hostility existing against the Principles and form of our Constitution. I am an Enemy to all banks discounting bills or notes for anything but Coin. If the American People allow private banks to control the issuance of their currency, first by inflation and then by deflation, the banks and corporations that will grow up around them will deprive the People of all their Property until their Children will wake up homeless on the continent their Fathers conquered.”

— Thomas Jefferson, Founding Father, Third President of the United States, and the principal author of the US Declaration of Independence

How bout a drink from the cup of truth…

The Bush administration’s $700 billion bailout plan may keep some banks afloat for the time being. But fundamental problems are still deeply rooted within the financial markets that threaten to bring down the whole system.

The hard truth is that there is no 100% safe place to keep your money.

Physical cash and gold are the safest places to hold your wealth right now. Anyone who tells you otherwise has either a motive or no clue.

Those with the means to do so should be holding at least some physical cash and gold.

Of course, people will debate why you should hold these assets…

Gold is the ultimate in hedging against financial turmoil. But as it stands today, it’s quite rare to find someone willing to trade a product or service for gold. In other words, it’s difficult to spend gold like money, which has been a criticism of owning physical gold for decades.

Today’s digital age allows consumers to move electronic fiat money around at speeds exponentially faster than ever before. This morning I paid my cable bill with my check card. The entire transaction was completed within 5 minutes. Had I paid by mailing a check, it could have taken up 1-2 days to reach the cable company and 3-5 days to clear my account.

So what if there was a way gold could be used as easily as electronic money?

The World’s Only “100% Backed-by-Gold Bank”

You might have a hard time believing this, but you can actually put yourself on a personal gold standard with a new kind of currency, and it’s rapidly growing among gold bugs.

Understand first, this new currency is not legal tender issued by any government. That means there’s no debt, inflation, geopolitical turmoil, or any other considerations normally associated with government-issued currency.

The currency comes in electronic form, but can be used like any other currency in the world today to pay for goods and services, and even settle debt. But there’s one major difference that sets this currency apart from every other in the world:

It’s 100% backed by gold.

In fact, in most cases you can instantly exchange this currency for physical gold at any time… a feature taken away from the US dollar decades ago.

This currency has a new system fully established, making it as easy to use as the current banking industry’s electronic money. Right now, in fact, there are already over 3,000 outfits—and climbing—in which you can pay online using this currency.

How the “Gold Bank” Works

Customers transfer funds from traditional bank accounts into these unique gold-backed bank accounts, and earn interest on their funds prior to placing an order.

Meanwhile, for customers already holding gold and silver in secured (and insured) vaults, their metals are insured and held in specialized bullion vaults. Their metals assets go through an annual audit, and are fully reported to customers.

Once customers’ funds are in the database, customers’ orders are made through its secure online system. Database servers record all transactions and store currency and metal balances.

The Advantages of Using this Currency?

Being backed by gold, the purchasing power of this currency fluctuates in relation to the price of gold.

This means that as the price of gold increases, the purchasing power of the account increases. On the flip side, however, if the price of gold falls, so does the value of the account. Nonetheless, the risk of significant price fluctuation in gold is small compared to the risk of value fluctuations among fiat currencies, especially the US dollar.

And despite a short-term correction, the price of gold has increased significantly over the past five years. So this factor has worked out to the advantage of anyone holding this currency over that period. And with +$2,000 gold on the horizon, holders of this currency should do quite well in the future.

Now you should know that I’m in no way affiliated with this service, nor do I receive any compensation from it. That said…

I Recently Put the Final Touches on my New Research Report…

This report shares all the details about the new gold-backed electronic currency, and it’s yours free after you take a risk-free trial of the Mining Speculator service.

It’s your chance to get in on the biggest and best buying opportunity in junior gold and silver stocks… ever.

That’s right. The junior gold market is about to blast off, after a brutal beat-down sparked by the financial crisis. Truth is, it’s pushed many gold and silver stocks to new lows…

… Which is why you don’t want to wait a minute longer to position yourself in the Mining Speculator’s mining and precious metals portfolio. Our team of analysts scour the earth for opportunities in gold, as protection against the financial uncertainties engulfing the U.S. and world markets.

It’s the ultimate opportunity in a period of great crisis.

You see, as our government continues to lose control of its ability to manage and prop up markets, gold and silver will undoubtedly make meteoric moves that will stun the populace.

And just in case you still harbor doubts about gold, consider this… reported last week in the Financial Times…

“… Investors in gold are demanding ‘unprecedented’ amounts of bullion bars and coins and moving them into their own vaults as fears about the health of the global financial system deepen.”

And since gold bullion is getting harder and harder to come by, more investors are looking for the next best alternative, and that’s…

Precious Metals Mining Stocks

Bottom line: Junior mining stocks will begin to make major moves to the upside, rewarding those who got in early and held on… and those who get in now at what are, frankly, bargain share prices.

You see, nothing can keep gold from doubling up and hitting $2,000 an ounce… causing shares in our mining exploration companies to skyrocket.

I’m talking about junior mining stocks with the potential to double, triple—even quadruple!

Of course, many people have trouble accepting gold as an investment—even now that they’ve witnessed a financial upheaval that’s shaken our country by the shoulders.

But I also know that those who have heard me out-and followed through with my research and recommendations-have made extraordinary, life-altering returns.

Which is why I maintain…

There’s never been a better time-a more crucial time-to protect your portfolio with gold and precious metals.

And for a brief time, we’re making it easy to do just that… for as little as $25.

To get immediate inside access to the junior mining companies poised for major run-ups – the ones I’ve visited firsthand and carefully selected after exhaustive research and quality controls – simply take a trial of my Mining Speculator advisory.

When you sign up for Mining Speculator, I will immediately send you the free report on the new gold-backed currency mentioned in this editorial.

So, for only $25 you’ll begin to receive my Mining Speculator junior stock advisory… one that held an average 212% gain over five years… plus you’ll get our new special report on “The World’s Only 100% Backed-by-Gold Bank.”

All you have to do is click here to get started.

Good investing,

Greg McCoach, Investment Director, Mining Speculator

Luke Burgess, Editor, Gold World

====================================================

My Note: I do not receive any renumeration or commissions for recommending either the Gold backed banking or the Mining Speculator. As Always be sure to do your own due diligence and read the prospectus before making any investments or deposits into financial institutions.-jschulmansr